![]()

![]()

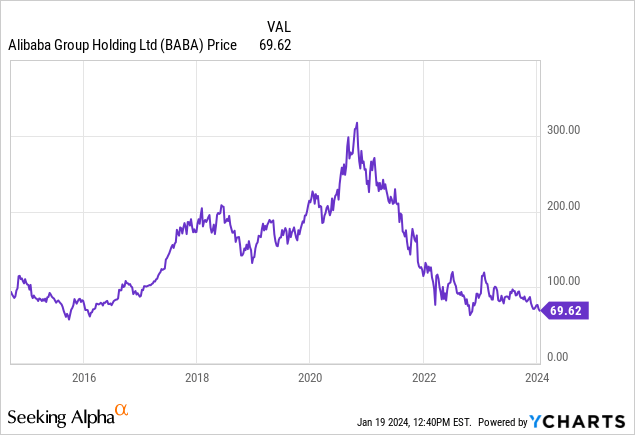

I vacillated from skepticism regarding its overvaluation in the early years post the 2014 Alibaba Group Holding ADR (NYSE:BABA) IPO to outright bearishness in recent years due to a slowdown in company growth and Chinese government intervention in operations. However, circumstances have shifted. While I wouldn’t label myself a fervent bull on the stock, if you’re keen on participating in China’s economy, diversifying away from a Western-market focus, the case for owning Alibaba has significantly strengthened compared to 6-12 months ago.

Undoubtedly, numerous obstacles, including a Chinese economy teetering on the edge of recession, the emergence of new government regulations on AI development, concerns about accounting disparities versus GAAP U.S. results, and the continued tight reins on capital outflows from the world’s second-largest economy, will pose challenges for both company growth and the stock price moving forward. BABA has been the quintessential example of how an inexpensive stock can become even cheaper when a slew of negative news compounds already bearish investor sentiment.

One positive development that has swayed me to elevate my rating on Alibaba is the capital return initiative. In November, the company obtained approval to distribute dividends to U.S. and other foreign shareholders. I’ve bemoaned that a $1 annual payout isn’t substantial enough to attract the income-oriented investor cohort, but one has to start somewhere (yielding 1.5% in cash as of yesterday). Additionally, share buybacks have marginally decreased the outstanding counts for several years now.

Ultimately, if Sino-U.S. tensions ease and this typically insular nation loosens its capital flows and market access to foster greater competition, Alibaba could rapidly transform into a formidable wealth generator. I understand it won’t materialize overnight, but institutional-sized value investors like the late Charlie Munger have been acquiring shares since 2021. Presently, the value proposition is quite compelling, particularly when benchmarked against the closest U.S. E-commerce and Big Tech peer, Amazon (AMZN).

For investors contemplating diversification beyond exclusive U.S.-based asset allocations into Asia, initiating a modest position in Alibaba could be the appropriate starting point. I am upgrading my 12-month outlook from Hold in September to a marginal Buy stance. This marks my first bullish rating ever for the stock (I have been contributing to Seeking Alpha since 2013).

Certainly, if China were to annex Taiwan in 2024, owning shares would be arduous, both practically and emotionally. Heck, the company might even face delisting in New York. This additional risk shouldn’t be casually dismissed.

The Valuation Story

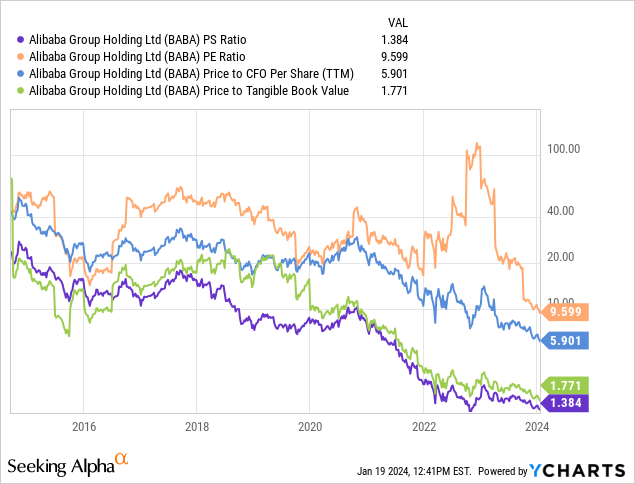

The overall fundamental valuation setup is presently at record lows in January 2024, dating back to the company’s U.S. listing nearly a decade ago. Price to trailing sales (1.38x), earnings (9.6x), cash flow (5.9x), and tangible book value (1.77x) ratios are depicted below.

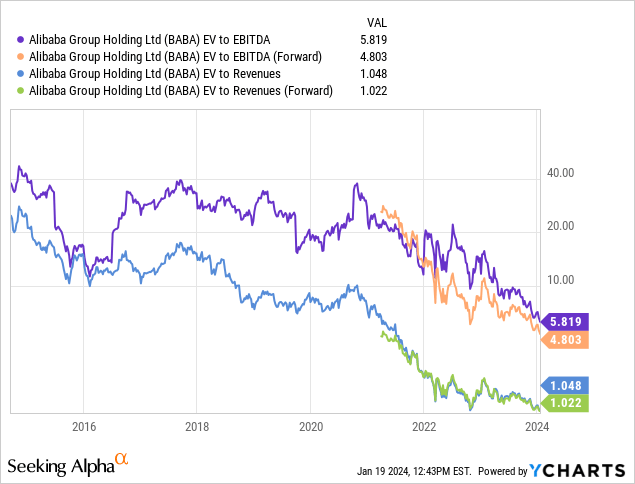

What’s even more compelling to me is the enterprise value scenario. When we account for the fact that debts ($27 billion in debt and lease obligations as of September) are vastly inferior to cash holdings ($78 billion), EV to EBITDA and sales multiples are entering the realm of “deep value” for investors. For instance, both figures are approximately 85% to 90% lower than their peaks in 2021.

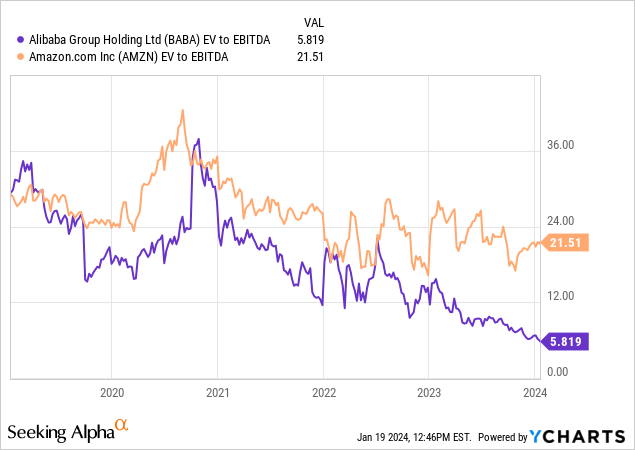

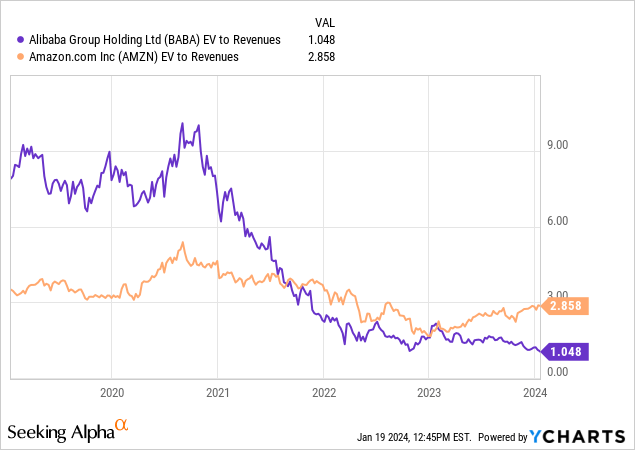

Comparisons to Amazon

Although they operate similar business models focused on fulfilling consumer/business demand and sales through the internet, with a suite of related operations from finance to online-sold cloud-based products, Amazon may be considered Alibaba’s U.S. counterpart for stock comparison purposes by investors.

For this piece, I will spotlight 5-year charts of EV to core cash EBITDA generation and total sales. You will observe that the valuation trajectories mirrored each other until 2023. At present, the disparity in investor pricing for both entities is quite astounding. In terms of EBITDA, Alibaba is priced at a 70% discount to Amazon, while sales are 65% lower. In late 2020, Alibaba traded at a premium!

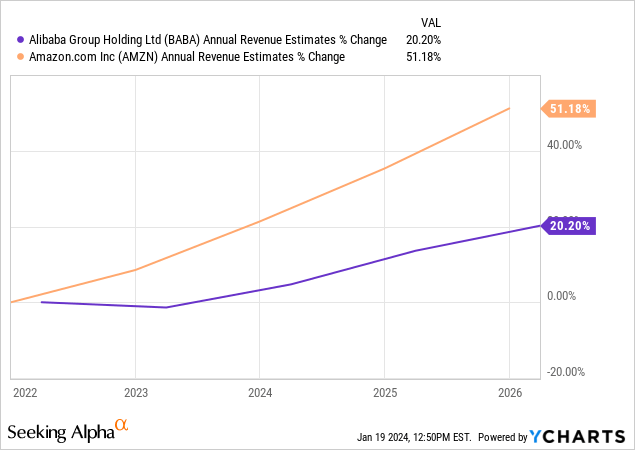

One justification for Alibaba’s discount is that sales and earnings growth are anticipated to lag behind Amazon’s until 2026 (although Amazon is also grappling with noticeably slower growth compared to 5 or 10 years ago). Both businesses are reaching sizable proportions, and the competition for online-oriented sales is cutthroat across the board. At this juncture, I would assert that both entities are in the mature stage of growth.

Below is a graph depicting Wall Street analyst estimates for sales growth for each. Visually, you can discern that Amazon is expanding at a faster clip. Hence, it probably merits higher valuation metrics than Alibaba. The question is, to what extent should this variance exist?

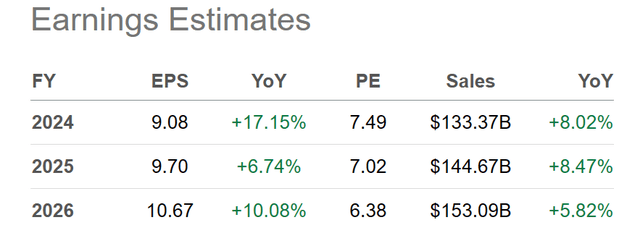

The jaw-dropping disparity in data points is that Alibaba shareholders are forecasted to have access to an earnings yield approaching 14% annually at the current sub-$70 ADR price. In contrast, Amazon is projected to yield a meager 3.1% for 2024-25 estimates. Amazon even fails to deliver an earnings yield close to the risk-free 1-year Treasury rate of just under 5%, whereas Alibaba is generating a figure nearly three times that of short-term Treasuries for investors!

Alibaba’s Future Outlook: A Bullish Perspective

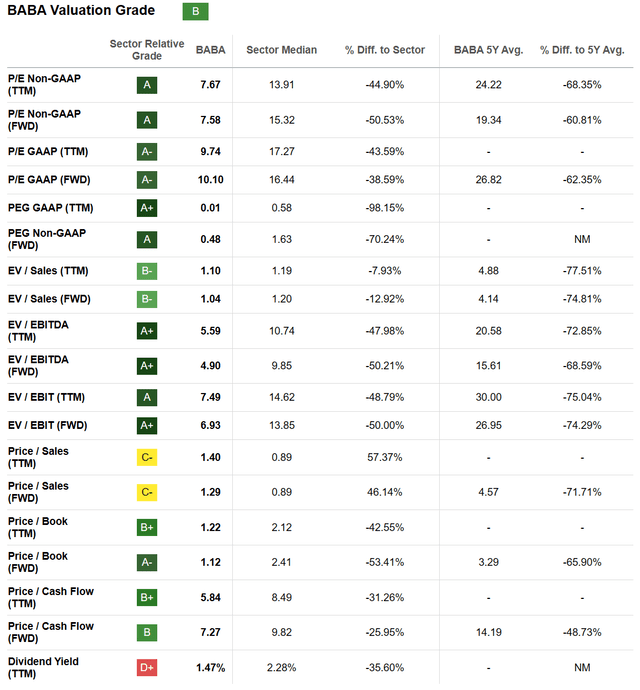

Seeking Alpha’s assessment of Alibaba reflects a “B” Quant Valuation Grade, perceived pessimistically by some. However, an alternative view holds that the stock deserves an “A” grade. The reasons for this optimism are diverse and compelling.

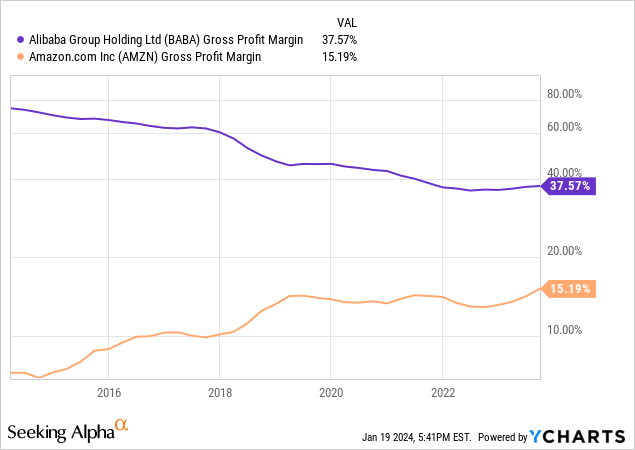

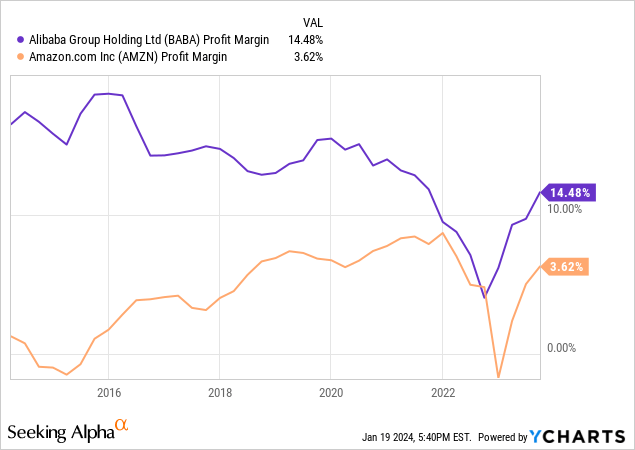

Alibaba’s high price-to-sales ratio may appear underwhelming compared to its peers. However, this metric is influenced by robust profit margins, presenting a favorable scenario for shareholders. In fact, Alibaba’s gross and final profit margins surpass those of Amazon by a substantial margin, signaling underlying strength in the company’s fundamentals.

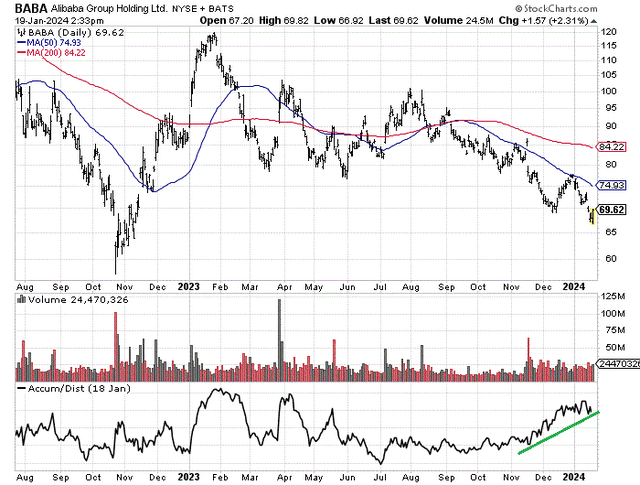

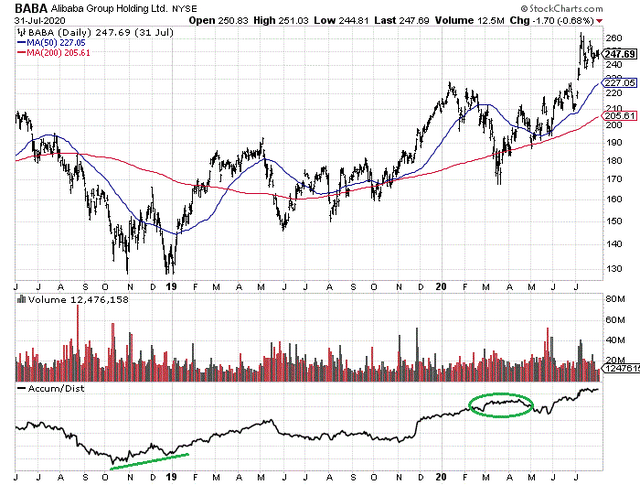

Unusual Accumulation/Distribution Line Strength

An intriguing aspect of Alibaba’s current standing is the rare uptick in the Accumulation/Distribution Line amidst a phase of declining prices. Historical data reveals only three similar instances of positive momentum in the ADL since 2014 during a price downturn. Such occurrences have historically signaled a bullish market outlook for intermediate-term buyers, often precipitating significant upswings in the stock price over the subsequent three to 18 months.

Examining the 18-month chart depicting daily price and volume fluctuations for Alibaba, a notable discord is observed between the ADL indicator and the share price movement. Unlike typical patterns, the recent price decline since November has not been corroborated by a corresponding decrease in the ADL. On the contrary, the ADL has displayed a positive trajectory, marked by a notable upturn indicated by a green line.

In the past, instances of price declines unaccompanied by a corresponding decrease in the ADL have heralded favorable market conditions. During the 2020 pandemic-induced slump, this trend preceded a resurgence in Alibaba’s stock price, resulting in a significant uptick of around 50% over the subsequent four months. Similar episodes in 2018 and 2016 have also been followed by notable upswings, cementing the significance of the current divergence between the ADL and the stock price.

The recurrent pattern of positive ADL divergences has consistently culminated in a bottoming out of stock prices between January and March, mirroring the current market dynamics.

Despite the absence of any overtly bullish signals on the momentum chart, the historical precedence of reversal patterns in Alibaba’s stock performance warrants careful consideration. The company has exhibited a propensity for sudden reversals, both upward and downward, devoid of explicit precursory signals.

Concluding Remarks

While I haven’t personally invested in Alibaba shares yet, the rationale for doing so is becoming increasingly compelling. For investors seeking exposure to the Chinese market, Alibaba emerges as a promising starting point. The possibility of a substantial surge in the stock price, contingent on a more favorable stance from the Chinese government toward Jack Ma and corporate leaders, is a tantalizing prospect that may materialize in the coming years. If such a scenario unfolds, the stock valuation could easily justify a twofold or threefold increase within the next 2-3 years, potentially reverting to the price levels witnessed in 2020-21, underpinned by stronger underlying value.

Furthermore, the recent initiatives to return capital to shareholders through stock buybacks and the introduction of dividends signify a positive shift in the company’s strategic direction, particularly for U.S.-based investors.

Balancing the sobering risk of a complete loss in the event of heightened geopolitical tensions between China and the U.S., an equally plausible outcome entails a substantial appreciation of 100% or 200%, premised on a favorable environment characterized by reduced government regulations and a robust Asian economy. This juxtaposition highlights the compelling risk/reward dynamic, deserving of earnest consideration. It is important to note that despite the potential risks associated with Alibaba shares, maintaining a cautious approach, such as implementing risk mitigation strategies like selling covered calls or setting tight stop-sell orders, is advisable to limit potential losses.

In conclusion, while my characterization of Alibaba as a “Buy” applies within the constraints of prudent investment practices, I encourage readers to view this article as the first step in a comprehensive due diligence process. Seeking guidance from a seasoned investment advisor before making any investment decision is strongly recommended.

Editor’s Note: This article discusses securities that are not traded on a major U.S. exchange. Hence, readers are urged to acknowledge the associated risks before considering investment in these stocks.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.