Alibaba is facing significant profitability pressure due to rising costs. In the third quarter of fiscal 2026, sales and marketing expenses rose to 25.3% of revenues, while the cost of revenues hit 59.5%, largely driven by logistics and infrastructure spending. As a result, Alibaba’s adjusted EBITA fell 57% year-over-year, and operating income dropped 74%, with free cash flow decreasing by 71%, indicating that its expansion efforts are becoming increasingly capital-intensive.

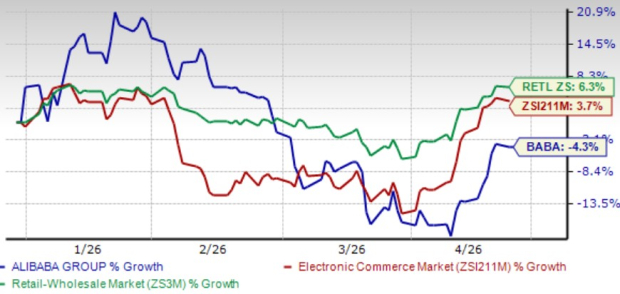

As of now, Alibaba shares have declined 4.3% year-to-date, underperforming the wider Zacks Internet – Commerce and Retail-Wholesale sectors that have seen gains of 3.7% and 6.3%, respectively. The Zacks Consensus Estimate for fiscal 2026 earnings has been revised down to $5.08 per share, reflecting a 43.62% year-over-year decline.

Competitors like JD.com and PDD Holdings are also experiencing margin pressures, with JD focusing on supply chain efficiency while facing high investments and PDD dealing with ecosystem investments and regulatory challenges affecting profit margins.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.