Alibaba’s Current Status

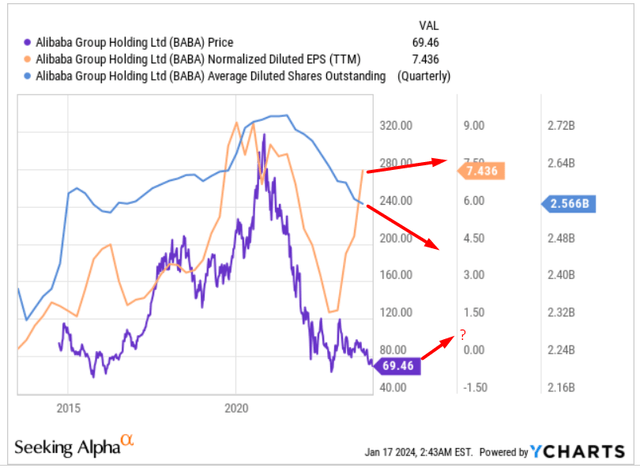

Alibaba Group (NYSE:BABA), once the favored gem of the e-commerce world, now faces a slew of challenges, including intensifying competition, geopolitical tensions, and broader economic weaknesses. The company’s stock has plummeted more than 78% from its 2020 peak:

The company, despite these challenges, presents itself as a classic contrarian ‘Buy’ opportunity due to its substantial margin of safety and the potential for growth from its ongoing ventures. Yet, this assertion comes with a bittersweet tinge of risk.

The Rational Case

Before delving deeper into Alibaba’s prospects, let’s first dissect its recent financials.

During the fiscal 2Q of FY2024, the company recorded a 9% year-over-year rise in revenue to RMB 224.7 billion, equivalent to approximately $30.8 billion, a 6% increase compared to the previous year. While this marked a positive uptick, the figures fell short of the anticipated $31.05 billion. Notably, the company’s non-GAAP earnings per ADS amounted to $2.14, surpassing the market consensus of $2.09. Despite the earnings beat, the company took investors by surprise when it announced the cancellation of its cloud business spin-off. This decision was primarily due to the constraints imposed by recent expansions in US export controls.

However, beyond the immediate disappointment of the halted cloud spin-off, Alibaba’s divisional performance in the second quarter merits a closer inspection.

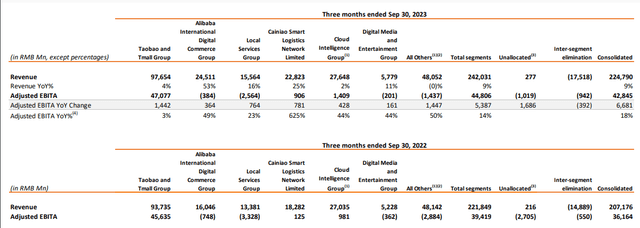

Previously, Alibaba operated in four segments: Core Commerce, Cloud Computing, Digital Media & Entertainment, and Innovation Initiatives. The company now reports its results separately for six units:

During Q2 of FY2024, the Taobao & Tmall Group (Core Commerce) displayed resilience with a 3% year-over-year growth in Customer Management Revenue (CMR), outpacing the minor decline in Gross Merchandise Volume (GMV). The group’s strategic focus on advertising investments, coupled with an upgraded ad-tech infrastructure, resulted in improved merchant ROI and increased customer engagement. Despite the positive CMR growth, the group’s EBITA inched up by 3% to RMB 47.1 billion, leading to a slight EBITA margin decrease to 48.2% from 48.7% a year ago. The management attributed this decline to ongoing investments in content and a pricing strategy emphasizing competitiveness.

Alibaba’s Cloud segment grappled with challenges, recording a modest 2.3% year-over-year revenue growth. However, a strategic shift away from lower-margin project-based contract revenue streams contributed to a healthier margin, elevating the EBITA margin to 5.1% from 1.6% in the corresponding quarter of the previous year. Notably, the termination of the full spin-off of Alibaba Cloud underscores its enduring importance in the company’s strategy, pivoting towards higher-margin public cloud revenue growth with a focus on AI cloud computing.

The Alibaba International Digital Commerce Group witnessed robust growth, marked by a remarkable 53% year-over-year revenue surge to RMB 24.5 billion. This expansion was underpinned by a blend of retail order growth (28% year-over-year) and solid performance across platforms such as Lazada, AliExpress, and Trendyol. Enhanced monetization efforts culminated in an adjusted EBITA of RMB -384 million, a stark improvement from RMB -748 million during the comparable quarter of the prior year.

The Local Services Group exhibited positive momentum, recording a 16% year-over-year revenue growth to RMB 15.6 billion. Additionally, the group managed to reduce its adjusted EBITA loss year-over-year to RMB -2.6 billion, propelled by nearly 20% year-over-year growth in order volume and an expansion in active customers. The upbeat performance of Ele.me and Amap contributed to the Local Services Group’s advancement.

After scrutinizing the latest quarterly results across Alibaba’s divisions, there are no glaring negative aspects. While the absence of the cloud spin-off disappointed investors, management’s strategic decisions indicate evolving priorities. The termination of the spin-off is unlikely to diminish its strategic significance for Alibaba. The pivot is towards higher-margin public cloud revenue growth, focusing on AI cloud computing. Goldman Sachs [November 2023, proprietary source] anticipates Alibaba Cloud revenue growth of 2-4% for the 3rd and 4th quarters of FY2024, accompanied by a reduction in revenue from project-based contracts. Analysts opine that the launch of “Wanxiangtai Unbounded” and the “return to Taobao” strategy could fuel further growth.

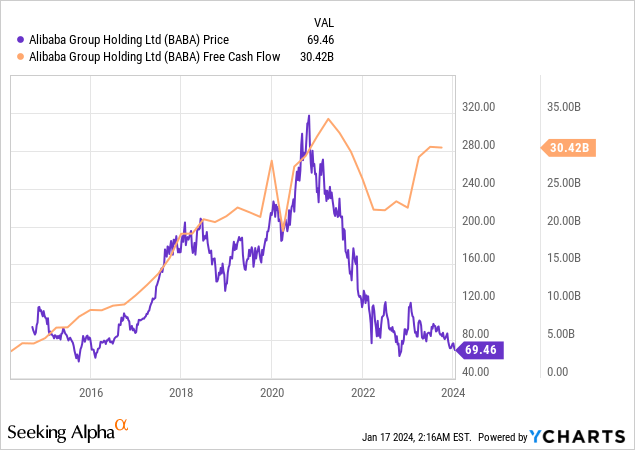

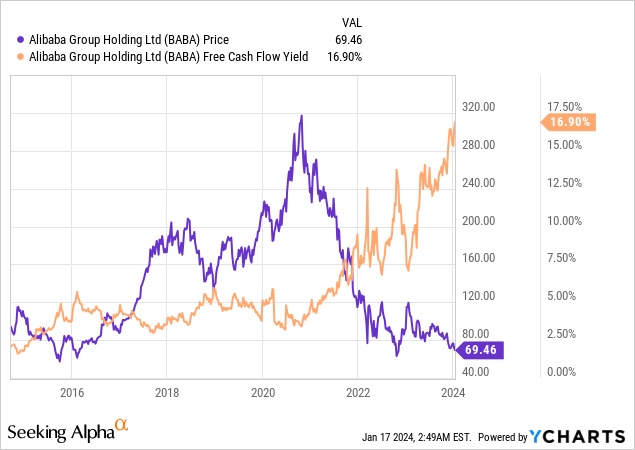

Although Alibaba’s initiatives to steer its operational growth towards higher-margin ventures are in their nascent phase, the company is already on course to restore its free cash flow to pre-COVID levels.

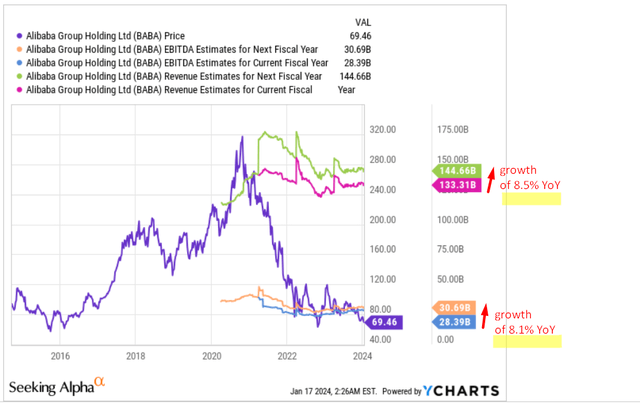

Given the recent positive developments within Alibaba’s still loss-making International Digital Commerce Group, I envision BABA achieving margin expansion in the calendar 2024 year, despite the challenges and skepticism from many market participants. According to YCharts, Alibaba’s revenue growth rate next year is projected to surpass its EBITDA growth rate over the same period. This implies an expected decline in margin, despite management’s visible efforts to achieve the contrary.

On the whole, a conspicuous gulf exists in market expectations. Wall Street consensus estimates foreshadow earnings per share growth over the next six years at a CAGR

Alibaba’s Future Viability and Market Resilience

Alibaba Group Holding Limited, a global e-commerce and technology conglomerate, has experienced formidable challenges alongside noteworthy advancements in recent years. Amidst fluctuations in Earnings Per Share (EPS) and the ascent of high-growth undertakings, including ventures like Lazard, the company is fiercely grappling with the complexities of market dynamics. Despite the nascent breaking even in the past few quarters, the trajectory of the organization’s international business appears buoyant, poised to elevate the operating profit, thereby dispelling the headwind of EBITA growth.

In the face of a glaring disjunction between the stock’s performance and the company’s business aptitude, Alibaba’s stock presents an unprecedented opportunity for investors. The Free Cash Flow (FCF) yield and various valuation metrics collectively unveil an unparalleled value proposition. The prevailing fear surrounding the investability of Chinese stocks reverberates within the market, a caution that necessitates meticulous contemplation. As the scales tip, there arises a poetic call-to-action, resonating the essence of a famous aphorism, interwoven in the crux of this narrative.

Navigating Risks

While considering an investment in Alibaba, it is imperative to acknowledge the latent risks that elusive investment propositions inherently encompass. The potential variations in Gross Merchandise Volume (GMV) growth, contingent upon macroeconomic vicissitudes or augmented competition, cast a looming shadow of uncertainty. The intricate interplay between the retail marketplace in China and the company’s monetization endeavors poses a convoluted blend of hazards, particularly if the monetization in China’s retail sphere fails to meet expectations.

The ongoing metamorphosis within the organization, holding latent promises of ameliorating the execution of disparate businesses, is counterbalanced by the lurking risks of divergence and tribulations. The sheer magnitude of Alibaba breeds concerns that the restructuring process might inadvertently proffer an opening for more focused contenders to seize market share. The departure of Jack Ma, an indomitable figure synonymous with the company, coupled with the transition away from his integrated approach to commerce, unfurls an enigma of uncertainty.

Moreover, flourishing within the confined contours of the People’s Republic of China’s regulated economy tether Alibaba to a web of regulatory perplexities. The capricious undercurrents of regulatory developments, especially against the backdrop of ongoing global trade tensions, have the potential to reverberate through the company’s operational landscape and growth trajectory. Hence, all prospective investors must meticulously scrutinize these perils before treading the path of Alibaba’s investment terrain.

Key Takeaways

While the landscape of Alibaba’s stock charts unveils a facade of despondency to the keen-eyed prospector, a deep dive into fundamental bedrocks reveals a contrasting narrative. The resilience demonstrated within the various divisions of the company in the preceding quarter, intertwined with their potential to augment the consolidated EBITA margin, reflects a narrative diametrically opposed to the consensus. Even with the current margin, Alibaba reaps a bountiful harvest, accumulating over 16% of the market capitalization in FCF. A.J. Button’s astute calculations infer that amalgamating FCF and the cash balance renders Alibaba capable of repurchasing its entire stock within a mere four-year window, an endeavor of Herculean proportions. Ergo, Alibaba radiates an alluring hue of undervaluation in the market’s kaleidoscope, a truth conspicuously acknowledged by all stakeholders. However, the catalyst that could pivot the stock lies ensconced in the expansion of margins. Hence, it beckons the discerning investor to embrace a spirit of acquisitiveness in this juncture.

Good luck with your investments!

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.