A meticulously compiled daily market digest from Nasdaq’s IR crew.

#marketseverywhere | Federal Reserve decision imminent with a mere 1% probability of a rate slash today, but sights set on a 55% likelihood for cuts in June. Critical focus narrows on dot plots and the Summary of Economic Projections.

The ominous shadow of inflation creeps upon us as Brent crude clinches above $87 per barrel for the first time since last October, while US1YR inflation swaps perceptibly ascend to 2.64%, marking its highest since last year.

“Central bankers find themselves in a tough spot, endeavoring to fine-tune policy amid prolonged and unpredictable policy lags aggravated by the recent inflation upheaval and conjoined post-Covid structural transformations.” -Insights from Jim Reid at Deutsche Bank

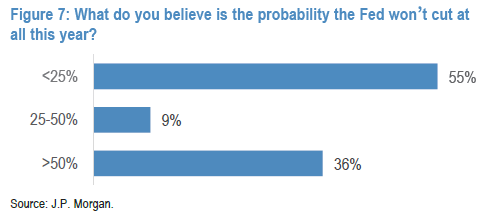

| Can it be fathomed that the Federal Reserve might abstain from snipping rates until 2024, as suggested by a JP Morgan investor poll?

The Ripple Effect of Easy Money Policies

Delving into the nitty-gritty, the BOJ’s prolonged era of ultracheap money introduces subtle tremors to the global financial landscape. The carry trade phenomenon, propelled by years of yen-fueled investments worldwide, paints a riveting picture of potential market reshaping as the BOJ navigates policy normalization ahead. Keeping a vigil eye, the US Treasury market emerges as a central player, beckoning wary attention due to its allure for Japanese capital.

This thought-provoking narrative stems from the Wall Street Journal Editorial Board’s sharp insights in “Japan Ends the Negative Rate Mistake.”

Global Fund Manager Survey Insights

As per BofA’s Global Fund Manager Survey:

Investors notably realign their positions, transitioning towards the Eurozone and Emerging Markets while diverting from US equities.

On an absolute scale:

Optimism reigns supreme over healthcare, tech, stocks, and Japan; conversely, skepticism looms over the UK, Utilities, REITs, and materials sector.

Market breadth displays a recent positive trend – the pivotal question arises: can this growth be perpetuated?

Meanwhile, a JPMorgan investor survey raises pertinent concerns about elevated valuations and escalating inflation risks as 82% of respondents brace for an impending market correction.

Goldman Sachs optimistically anticipates a downtrend in inflation by June, potentially paving the way for a rate cut – but will this prophecy hold true?

A Glance into Productivity Growth

The narrative shifts towards a contemplative stance, urging a return to #EconomicGrowth. Endeavoring to offer context, Deutsche Bank’s Jim Reid delves into the annals of post-WWII economic growth. A poignant reflection surfaces on the rolling 10-year average of annual productivity growth, oscillating around a meager 1.5% post-mid 2010s. Coupled with dwindling population growth, this trend underpins the comparatively feeble US economic growth trajectory since the aftermath of the GFC. Where does the trajectory of US productivity growth steer from here?

Investors’ clamor for corporates to shower cash upon shareholders spikes, marking its highest ascent since Feb’16.

Key Insights

Equities depict a mixed to lower trend, juxtaposed against a soaring Dollar and declining Oil, Treasury Yields, and Gold prices.

DJ -0.1%, S&P500 -0.1%, Nasdaq -0.1%, R2K -0.2%

Stoxx Europe 600 -0.0%, APAC stocks gain traction with the 10YR Treasury Yield standing at 4.295%

Midst this week’s prospects:

“The Fed, the BoJ, and the BoE headline the policy domain next week. Vital economic shifts are anticipated from global flash PMIs on Thursday, accompanied by inflation updates from Japan and the UK. China’s economic barometers are slated for release on Monday.” -Insights from Deutsche Bank

Market Musings and Financial Buzz

- Fed poised to unveil hints on interest-rate trajectory -BBG

- The Fed grapples with a plethora of conundrums regarding its balance sheet -BBG

- Speculations arise on a probable reduction in the frequency of rate cuts by the Fed due to continued economic expansion -CNBC

- Divisions among investors and economists persist on the likelihood of BOJ implementing subsequent rate hikes -BBG

- Post a significant policy pivot, BOJ trims the maximum JGB purchase limit -RTRS

- ECB’s Kazaks expresses contentment with market anticipations of three rate cuts this year -RTRS

- FTSE 100 Live: Subdued UK inflation sustains anticipation for summer BOE rate adjustments

The Dynamic Landscape of Financial Markets: A Deep Dive into the Latest Market Updates

Central Bankers Navigate ‘immaculate disinflation’

Central bankers worldwide are setting their sights on achieving what has been dubbed as ‘immaculate disinflation,’ a remarkable feat that may soon become a reality. Recent reports by reputable sources like FT and BBG suggest that UK inflation has cooled significantly, reaching its slowest pace since 2021. In the same vein, the US dollar bears may find themselves in an unexpected position – being ‘gloriously wrong’ in light of falling global rates. The financial world is on the cusp of witnessing a unique convergence of events that could reshape the economic landscape.

China’s Economic Ripples: Bonds Boom and Builders’ Challenges

Amid these global shifts, China stands out as a focal point of economic activity. With the country’s decision to leave benchmark lending rates unchanged, as reported by RTRS, investors are facing what can only be described as an ‘asset famine.’ Concurrently, China’s bonds market is experiencing a significant boom, reflecting a complex interplay of market forces. Furthermore, as China’s builders embark on restructuring efforts to navigate a new phase of crisis, the country’s economic resilience is being put to the test.

Political Maneuvers: From NATO to US-China Relations

In the realm of geopolitics and international relations, intriguing developments are underway. Former US President Donald Trump’s statement on NATO hints at a nuanced stance – he expresses his commitment to the organization on the condition that Europe fulfills its financial obligations. Meanwhile, the US is contemplating sanctioning Huawei’s secretive Chinese chip network, signaling potential tensions in US-China relations.

Corporate Strategies and Market Dynamics

Shifting the focus to the corporate world, companies like Bharti Hexacom are gearing up for potential IPOs, with a Rs 4,300-crore offering anticipated in the coming weeks. South African Airways is on the lookout for new investors and a possible relisting following a failed deal. On the technology front, Intel is poised to receive a multibillion-dollar grant to bolster chip production, indicative of the tech industry’s ongoing evolution.

Industry Insights: Aerospace, Telecommunications, and AI

In the aerospace sector, Boeing is under scrutiny to enhance quality standards before ramping up 737 production, as per the FAA’s directives. Additionally, telecommunications giant Rogers Communications plans to offload its data center, while cybersecurity firm Cato Networks is reportedly considering an IPO in 2025. The realm of artificial intelligence is abuzz with activity, with Microsoft appointing DeepMind co-founder Suleyman to lead consumer AI initiatives, and Saudi Arabia gearing up for a massive $40 billion investment in AI technologies.

The Ebb and Flow of Markets: From Retail to Energy

Retail behemoth Gucci braces for a sales dip in the first quarter, attributing it to an Asia-related slowdown. On the energy front, Russia’s crude flows are witnessing disruptions, while projections indicate that US oil output may surpass 14 million bpd before stabilizing. Additionally, the Trans Mountain Pipeline expansion is slated for completion by the end of May, promising to reshape Canada’s energy landscape.

In conclusion, the financial markets are a tapestry of interconnected events and developments, each painting a unique picture of the global economy’s evolution. As investors navigate these turbulent waters, staying informed and attuned to the nuances of market dynamics is paramount. The convergence of economic, political, and corporate forces sets the stage for a compelling narrative of growth, change, and resilience in the financial world.