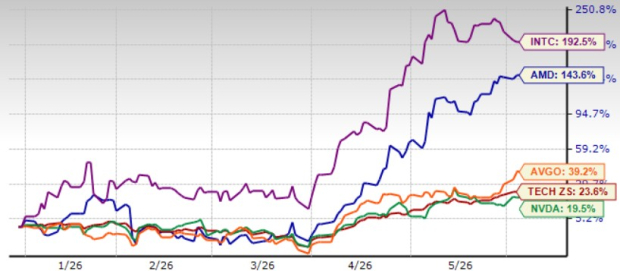

Advanced Micro Devices (AMD) reported a strong start to 2026, with shares closing at $521.54 on June 2, near a 52-week high of $527.20. Year-to-date, AMD shares have surged 143.6%, significantly outpacing the broader Zacks Computer and Technology sector’s 23.6% growth. The company’s revenue from its Data Center segment reached $5.8 billion in Q1, a 57% year-over-year increase, primarily driven by demand for data center EPYC CPUs and Instinct GPUs.

Looking ahead, AMD projects Q2 Data Center revenues to be approximately $11.2 billion, up 46% year-over-year, with server CPU revenue growth exceeding 70%. AMD’s total addressable market for server CPUs is now estimated at over $120 billion by 2030. Despite these promising figures, AMD faces intense competition from NVIDIA, Broadcom, and Intel, all of which have shown strong stock performance this year. AMD’s earnings estimate for Q2 is $1.60 per share, marking an 11.1% increase over the previous month.

However, challenges loom as AMD anticipates downward pressure on gross margins due to the expected inclusion of lower-margin AI accelerators in their offerings. Supply constraints and higher costs for components could also affect profitability and future growth. Currently, AMD holds a Zacks Rank of #3 (Hold), indicating that potential investors should consider waiting for a better entry point before buying into the stock.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.