Adobe Shares at Premium, Faces Competitive Challenges

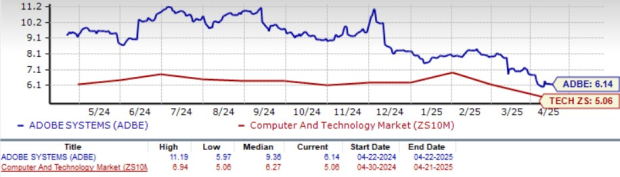

Adobe (ADBE) shares are currently trading at a premium, indicated by a Value Score of D. The stock has a forward 12-month price/sales ratio of 6.14X, higher than the Zacks Computer and Technology sector’s average of 5.06X. This premium pricing places Adobe ahead of its key competitors, such as digital marketing cloud provider Salesforce (CRM) and document services and e-signature provider DocuSign (DOCU), which trade at price/sales ratios of 5.62X and 4.73X, respectively.

Price/Sales Ratio (F12M)

Image Source: Zacks Investment Research

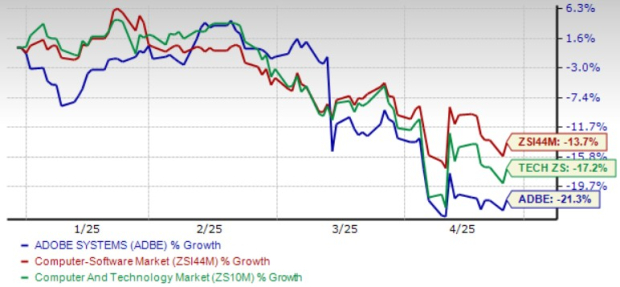

Adobe’s shares have declined 21.3% year to date (YTD), reflecting headwinds from tariffs and challenges from fierce competition in the AI and Generative AI (GenAI) sectors, particularly from Microsoft (MSFT)-backed OpenAI. Additionally, Adobe has struggled to monetize its AI solutions effectively. Over the same period, Adobe’s stock performance trailed behind Microsoft and DocuSign, but outperformed Salesforce, which saw drops of 12.9%, 17.5%, and 27.2%, respectively.

ADBE Stock’s Performance

Image Source: Zacks Investment Research

The question arises: are Adobe shares worth buying at this price? Let’s analyze the current situation.

Adobe’s Competition and Monetization Challenges

Adobe’s AI business remains relatively small compared to giants like Microsoft and Alphabet. Microsoft benefits from growth in Azure AI services and its AI Copilot initiative, while Alphabet’s Google Cloud sees accelerating growth in AI infrastructure and enterprise AI platform Vertex.

Despite these challenges, Adobe has expanded its AI portfolio with new products such as Adobe GenStudio and Firefly Services, designed to help brands collaborate on marketing. In Premiere Pro, Adobe introduced a Firefly Video Model feature that leverages AI for generating and extending video and audio clips. The company also launched an upgraded version of After Effects with advanced 3D motion design tools.

To improve monetization, Adobe is set to introduce standalone Firefly subscriptions within the Creative Cloud offerings and invest in its sales force to enhance its services across various sectors including business, education, and government. The integration of AI Assistant in products like Acrobat and Reader is expected to support Adobe’s growth trajectory. Currently, Adobe’s AI business has over $125 million, which constitutes a low single-digit percentage of its total revenues ($4.23 billion in Q1 FY25). The company anticipates this AI segment will double by the end of fiscal 2025.

Positive Guidance for Fiscal Year 2025

For fiscal 2025, Adobe expects Digital Media Annual Recurring Revenue to grow by approximately 11%. Revenues from the Digital Media segment are projected to be between $17.25 billion and $17.40 billion, while the Digital Experience segment is estimated at $5.8 billion to $5.9 billion, with subscription revenues between $5.375 billion and $5.425 billion.

In line with this, Adobe has reaffirmed its total revenue guidance of $23.30 billion to $23.55 billion for fiscal 2025, up from $21.51 billion in fiscal 2024. Non-GAAP earnings are projected to range from $20.20 to $20.50, compared to $18.42 per share in fiscal 2024.

ADBE 2025 Estimate Revision Trends

The Zacks Consensus Estimate for Adobe’s fiscal 2025 earnings is currently at $20.36 per share, reflecting a slight decline of five cents over the past 30 days, yet indicating a 10.53% growth compared to fiscal 2024.

Adobe Inc. Price and Consensus

Adobe Inc. price-consensus-chart | Adobe Inc. Quote

The Zacks Consensus Estimate for second-quarter fiscal 2025 earnings stands at $4.96 per share, down by one cent over the past 30 days. This figure indicates a 10.71% increase from the same quarter last year. Adobe has exceeded the Zacks Consensus Estimate for earnings in the last four quarters, with an average surprise of 2.53%.

Conclusion: ADBE Stock as a Hold

Adobe’s increasing focus on GenAI and its innovative product offerings are potential growth catalysts. Current shareholders might see long-term rewards from this growth trajectory.

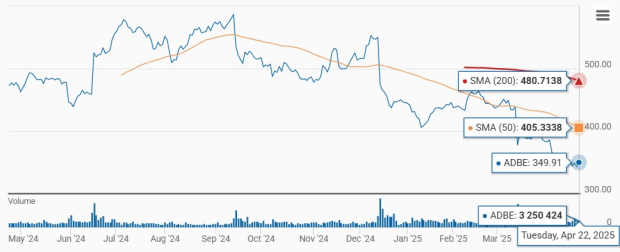

However, the stock’s current valuation may deter value-oriented investors. Presently, ADBE trades below both the 50-day and 200-day moving averages, which indicates a bearish trend.

ADBE Stock Trends Below Moving Averages

Image Source: Zacks Investment Research

ADBE holds a Zacks Rank of #3 (Hold), suggesting that investors should wait for a more favorable market opportunity to acquire the stock.