Bank Stocks in Focus Amid Tariff-Induced Market Turbulence

Understanding how banks operate reveals their business isn’t as affected by tariffs as one might think. However, the current performance of bank stocks suggests market participants are concerned about broader economic conditions amid ongoing tariff-related uncertainty.

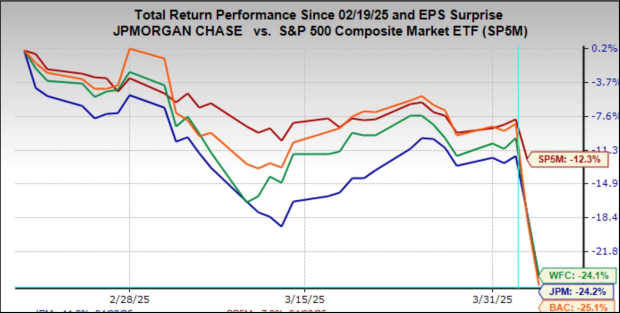

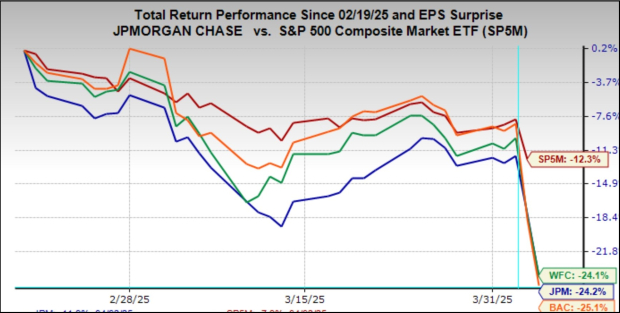

The following chart illustrates the performance of JPMorgan (JPM), Wells Fargo (WFC), Bank of America (BAC), and Morgan Stanley (MS) relative to the S&P 500 index since February 19th. Notably, two of these banks will kick off the Q1 2025 reporting cycle for the Finance sector on Friday, April 11th, before the market opens.

Image Source: Zacks Investment Research

While banking is not directly impacted by tariffs, these institutions are cyclical operators whose fortunes are closely tied to economic trends. The ongoing uncertainty surrounding tariffs has raised concerns about economic stability, prompting many economists to increase recession probabilities and reduce GDP growth forecasts.

The trends in the provided chart decisively indicate market sentiment is growing cautious about bank profitability. As economic conditions soften, credit demand typically declines, and asset quality can suffer. This is particularly true as some borrowers face difficulties in repaying loans.

Recent data from the Federal Reserve indicates a slight uptick in loan demand during the first quarter, particularly in commercial and industrial (C&I) loans and home-equity loans. Nevertheless, investors remain skeptical about whether these trends can continue under a challenging macroeconomic backdrop, as reflected in the stock performance of these banks.

Credit quality issues are particularly pronounced in the commercial real estate (CRE) market, which is already well accounted for at major banks. While aggregate bankruptcies in the U.S. have significantly increased since the low point during the Covid pandemic, the growth rate has stabilized in recent months. Early-stage credit card delinquencies also show a flat year-over-year growth rate, suggesting some stabilization in net charge-off levels this year.

Looking forward, expectations surrounding credit quality hinge on future economic conditions, as growth shows signs of moderation, if not a recession. Investment banking appears to be significantly impacted by declining market sentiment. Despite management teams signaling an increase in deal pipelines in recent quarters, hopes of a rebound in Q1 results have dimmed, especially with tariffs still dominating market discussions.

Anticipated Earnings for JPMorgan, Wells Fargo, & Morgan Stanley

JPMorgan is anticipated to report earnings of $4.60 per share, a decrease of 0.7% year-over-year, alongside revenues of $43.01 billion, marking a 2.6% increase from the previous year. Following its last earnings release on January 15th, the stock performed well, reflecting positive outlook commentary. The estimate has risen from $4.54 one month ago and $4.25 three months back.

Wells Fargo is expected to post earnings of $1.23 per share, down 2.4% year-over-year, with revenues estimated at $20.8 billion, a decline of 0.3% YOY. Earnings estimates for Q1 have remained relatively stable, with the current estimate slightly down from $1.24 a month prior but up from $1.19 three months ago. The stock rose following the last quarterly release on January 15th.

For Morgan Stanley, expectations are set for earnings of $2.32 per share, which represents a 14.9% increase YOY, with projected revenues of $16.8 billion, up 11.2%. Analysts have been increasingly optimistic, adjusting their estimates upward since the quarter began. Shares also rose following the last quarterly release for this bank.

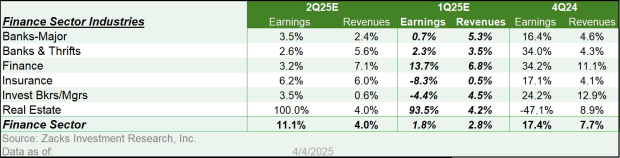

The Zacks Major Banks industry, which includes JPMorgan and Wells Fargo, is poised to see a 0.7% increase in Q1 earnings, along with a 5.3% rise in revenues. This sector contributed nearly 50% of the Zacks Finance sector’s total earnings over the previous four quarters.

Image Source: Zacks Investment Research

Overall, Q1 earnings for the Zacks Finance sector are projected to increase by 1.8% compared to the same period last year, alongside a 2.8% growth in revenues.

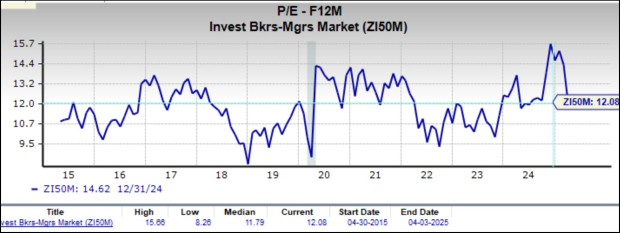

Despite outperforming the S&P 500 over the past year, large bank stocks generally remain undervalued based on traditional valuation metrics. The following chart shows the 10-year price-to-earnings (P/E) history for the Zacks Major Banks industry against a forward 12-month P/E ratio.

Image Source: Zacks Investment Research

Currently, the Zacks Major Banks industry is trading at 61% of the S&P 500’s forward 12-month P/E ratio. Historically, this industry has traded between 52% and 78% relative to the index over the last decade, with a median of 62%.

Image Source: Zacks Investment Research

Initial Q1 Earnings Overview

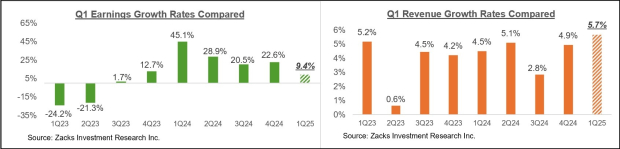

The Q1 reporting cycle is set to accelerate with the pending announcements from major banks. Recently, several companies with fiscal quarters ending in February have been releasing their results. Thus far, 19 S&P 500 members have reported February-quarter results, contributing to the overall March-quarter data.

Collectively, these 19 companies have experienced an earnings increase of 9.4% from the same year-ago timeframe on revenue growth of 5.7%. Notably, 57.9% of these companies surpassed EPS estimates, while 68.4% exceeded revenue expectations.

The comparison charts below contextualize these Q1 earnings and revenue growth rates historically.

Image Source: Zacks Investment Research

Additional comparison charts illustrate the Q1 EPS and revenue beat percentages within a historical context.

Q1 Earnings Estimates Show Weakness Amid Growing Economic Concerns

As illustrated in recent analyses, early earnings reports from various companies highlight challenges in meeting consensus estimates. This year’s EPS beat percentage is the lowest recorded in the last 20 quarters. While these preliminary results are concerning, caution is advised against overinterpreting them due to the small sample size.

Current Trends in Q1 Earnings Estimates

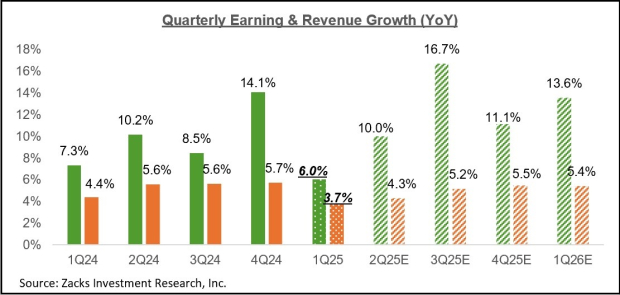

For the upcoming quarter, expectations indicate a 6% increase in earnings compared to the same period last year, alongside a revenue rise of 3.7%. This projected growth comes on the heels of a stronger prior quarter, which saw earnings increase by 14.1% and revenues by 5.7%.

The chart below depicts the current forecasts for earnings and revenue growth for Q1 2025, setting these expectations against trends observed over the previous four quarters and what is anticipated for the next four quarters.

Image Source: Zacks Investment Research

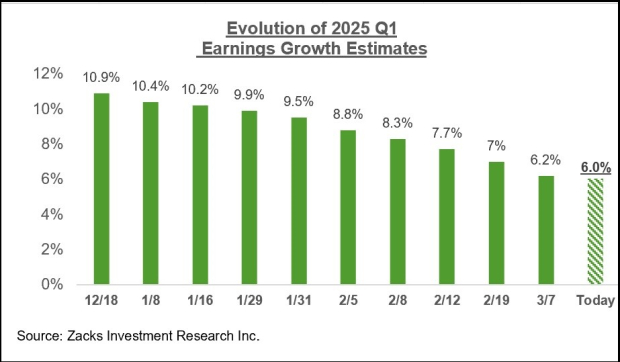

Significantly, the market has been experiencing an uptick in negative revisions to Q1 estimates, with few companies providing positive guidance, exacerbating concerns. The chart below tracks how earnings growth expectations for Q1 have shifted since January.

Image Source: Zacks Investment Research

Compared to earlier quarters, negative revisions since January have been more pronounced in both magnitude and scope. So far, estimates have declined for 13 out of the 16 Zacks sectors, with the most significant drops in Conglomerates, Autos, Basic Materials, Aerospace, and Consumer Discretionary.

Conversely, only Medical, Utilities, and Construction sectors have seen upward revisions for Q1 estimates.

Even the Technology sector, which has maintained positive outlooks over the past year, is facing downward adjustments to its Q1 projections. Recent market sentiment has soured, particularly after China’s DeepSeek announcement, dampening optimism around the AI investment sector. Challenges posed by tariffs are also heightening concerns, as much of the tech hardware originates from Asia.

Despite these challenges, the Tech sector is still projected to be a critical growth driver. Earnings for Q1 2025 in this sector are anticipated to rise by 12.6% with a revenue increase of 10.2%. The future of earnings expectations in Tech will significantly impact overall market performance, as this sector has been pivotal in driving growth over the last two years.

The current trend of disappointing guidance coincides with increasing worries regarding macroeconomic conditions. Market participants are becoming increasingly concerned about the U.S. economy’s growth prospects. Uncertainty surrounding the Trump administration’s tariff policies is reflected in declining business and consumer confidence metrics. There are fears that job cuts in the public sector may spread to the private sector.

The evolving tariff environment will likely necessitate further adjustments to earnings forecasts, mirroring current market weaknesses that stem from reduced expectations.

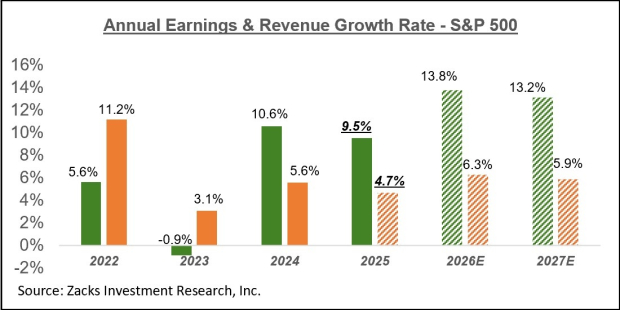

The chart below presents the broader earnings outlook on a calendar-year basis, illustrating anticipated strong growth momentum extending through 2027.

Image Source: Zacks Investment Research

For a comprehensive analysis of the evolving earnings landscape, check out our weekly Earnings Trends report here.

Upcoming Stock Recommendations

Recently, experts have identified seven stocks from a pool of 220 Zacks Rank #1 Strong Buys, which they believe are poised for early price increases.

Historically, this selection has outperformed the market by more than double since 1988, averaging annual gains of 23.9%. Investors are encouraged to take immediate notice of these curated stocks.

Bank of America Corporation (BAC): Free Stock Analysis Report

Wells Fargo & Company (WFC): Free Stock Analysis Report

JPMorgan Chase & Co. (JPM): Free Stock Analysis Report

Morgan Stanley (MS): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.