Market Update: Becton, Dickinson and Company Faces Stock Decline Despite Strong Q4 Results

With a market cap of $64 billion, Becton, Dickinson and Company (BDX) stands as a key player in global medical technology. Headquartered in Franklin Lakes, New Jersey, the company operates through three main segments: BD Medical, BD Life Sciences, and BD Interventional. It provides various products, including advanced catheters, diagnostic assays, and surgical instruments.

Classified as a “large-cap” stock, Becton Dickinson has a strong emphasis on enhancing patient care and medical innovation. The company focuses on developing, manufacturing, and marketing medical devices, laboratory equipment, and diagnostic tools aimed at healthcare providers, researchers, and the public at large.

Recently, Becton, Dickinson and Company’s stock has slid 11.6% from its 52-week high of $249.89, reached at the start of the year. Over the past three months, the company’s shares declined by 5.4%, underperforming relative to the Dow Jones Industrials Average ($DOWI), which saw an 8% increase.

Looking further back, Becton, Dickinson and Company has faced a year-to-date decline of 9.4%, contrasting sharply with the DOWI’s 17.1% gain. In the past 52 weeks, BDX shares dipped by 5.3%, while the DOWI achieved a remarkable 21.3% return in the same timeframe.

Evidence of the company’s struggles is clear, as BDX has traded below its 50-day and 200-day moving averages since November, indicating a bearish price trend.

On a positive note, BDX reported strong Q4 results on November 7, revealing an adjusted EPS of $3.81 and revenue of $5.4 billion, both exceeding expectations. The BD Medical segment notably contributed to this growth, recording an 11.1% surge in sales driven by advancements in medication delivery, particularly the Alaris platform, while the Interventional segment grew by 4.7%. The company has also made strides through its acquisition of Edwards Lifesciences’ Critical Care business, valued at $4.2 billion. Looking ahead, BDX forecasts revenue between $21.9 billion and $22.1 billion for fiscal 2025, paired with adjusted EPS expectations of $14.25 to $14.60.

However, despite the upbeat quarterly performance, BDX shares fell 5.4% on the announcement day due to rising operating expenses. These include a significant 10.5% increase in selling and administrative costs as well as higher research and development expenditures, which are expected to squeeze profit margins. Additionally, BDX’s total debt rose to $20.1 billion, raising red flags for investors.

In comparison, Edwards Lifesciences Corporation (EW) has seen better fortune, with EW shares rising nearly 5% over the past year and a modest 3.2% drop year-to-date.

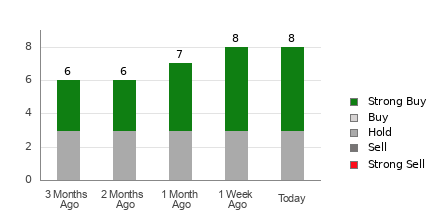

Even amidst BDX’s challenges, analysts remain optimistic about the company. A consensus “Strong Buy” rating has been assigned to the stock by 17 analysts, and it currently trades below the mean price target of $278.07.

On the date of publication, Sohini Mondal did not hold (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data provided herein are for informational purposes only. Please view the Barchart Disclosure Policy for more information. More news from Barchart

The opinions expressed here are solely those of the author and do not necessarily reflect the views of Nasdaq, Inc.