Domino’s Set to Announce Q1 Earnings Amid Mixed Analyst Sentiment

With a market capitalization of nearly $15.9 billion, Domino’s Pizza, Inc. (DPZ) specializes in pizza delivery and carryout under its brand name through both company-owned and franchised locations. Based in Ann Arbor, Michigan, the company also offers a variety of menu items, including bread products, wings, boneless chicken, pastas, sandwiches, dips, beverages, and desserts. Investors are anticipating the announcement of its fiscal Q1 earnings for 2025, slated for Monday, April 28, before market opening.

Analyst Expectations for Earnings

As the earnings release approaches, analysts expect the pizza giant to report earnings of $4.08 per share, reflecting a 14% increase from $3.58 per share in the same quarter last year. Over the past year, Domino’s has met or exceeded Wall Street’s earnings expectations in three out of four previous quarters, although it fell short on one occasion. Last quarter, the company posted earnings of $4.89 per share, which slightly missed consensus estimates.

Financial Projections for the Year

For the entire fiscal year, analysts project that DPZ will report an annual earnings per share (EPS) of $17.53, which is a 5% increase from $16.69 in fiscal 2024. Furthermore, EPS is anticipated to rise by 11.1% year-over-year, reaching $19.47 in fiscal 2026.

Stock Performance and Market Comparison

Over the past 52 weeks, DPZ shares have decreased by 3.9%, underperforming the S&P 500 Index’s ($SPX) gain of 5.5% and the Consumer Discretionary Select Sector SPDR Fund’s (XLY) increase of 7.4% during the same timeframe.

Recent Earnings Report and Market Challenges

On February 24, DPZ shares fell 1.5% following the release of weaker-than-anticipated Q4 earnings. The company reported year-over-year revenue growth of 2.9%, totaling $1.4 billion, while earnings grew by 9.2% to $4.89 per share. However, both figures fell short of analysts’ expectations. Notably, the international segment achieved its 31st consecutive year of same-store sales growth, despite a challenging global economic landscape. Meanwhile, operating income rose 6.4% year-over-year to $273.7 million.

Despite these achievements, DPZ faced challenges related to consumer spending, the transition of its equipment and supplies business to third-party suppliers, and an increase in the provision for income taxes, which hindered its overall performance.

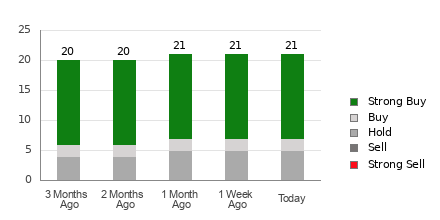

Analysts’ Ratings and Price Target

Wall Street analysts express a moderately optimistic outlook for DPZ’s stock, assigning a “Moderate Buy” rating overall. Out of 29 analysts covering the stock, 16 recommend a “Strong Buy”, two suggest a “Moderate Buy,” 10 indicate “Hold,” and one rates it as a “Strong Sell.” The average price target for DPZ stands at $489.96, reflecting a potential upside of 3% from current levels.

On the date of publication, Neharika Jain did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article are solely for informational purposes. For more information, please view the Barchart Disclosure Policy here.

More news from Barchart

The views and opinions expressed herein are those of the author and do not necessarily reflect those of Nasdaq, Inc.