Federal Reserve’s Interest Rate Decisions Under Scrutiny Amid Latest Economic Data

The Federal Reserve appears to be confronting a “boogeyman” that may not exist. Fed Chairman Jerome Powell emphasized the need for “greater confidence” regarding the cooling of inflation. The focus is not only on overall numbers, but specifically on core services and housing, which have shown persistent inflationary pressures.

Last week, the Fed opted to maintain key interest rates, which was expected. Currently, they remain in a “wait-and-see” phase. However, I believe this strategy may be misguided, as I discussed in a previous Market 360 article. The influence of tariffs on prices seems exaggerated to me. Much of the impact from the baseline 10% tariffs is likely to be offset by a stronger dollar. With many countries now engaging in negotiations, the outcome could favor not only free trade but also a fairer trading environment for the U.S.

Nonetheless, it’s important to note that adjustments will take time. This week’s economic data is critical for understanding whether inflation is indeed easing and if tariffs are affecting prices as many have suggested.

The upcoming April Consumer Price Index (CPI) and Producer Price Index (PPI) reports will provide new insights. Additionally, the April retail sales report will reveal if American consumers continue to spend or are starting to contract their spending due to rising interest rates.

The implications of these data points could significantly influence the Fed’s future decisions. Should inflation show clear signs of deceleration, coupled with a cooling in consumer demand, the possibility of rate cuts later this year remains viable.

In today’s Market 360, I aim to analyze these three critical reports in detail.

It’s vital for the Fed to reconsider its stance and initiate rate cuts sooner rather than later. A global decline in interest rates is happening, and our central bank may soon need to catch up. A proactive approach could be beneficial, especially given more significant threats looming on the horizon—threats that are easily overlooked amidst the current tariff and interest rate discussions.

Consumer Price Index

Tuesday’s CPI report confirmed my belief: inflation is moderating, indicating that the Federal Reserve should reduce key interest rates promptly.

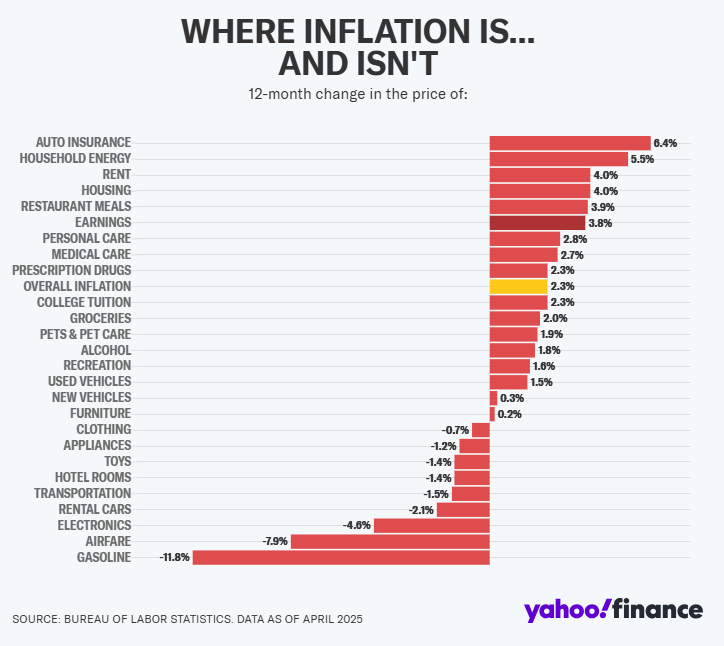

In April, consumer prices increased by just 2.3% year-over-year, down from 2.4% in March and below the anticipated 2.4%. This is the slowest rise since February 2021. Month-over-month, prices climbed only 0.2%, falling short of economists’ expectations of 0.3%.

Core CPI, which excludes food and energy, rose 0.2% in April and gained 2.8% year-over-year, aligning with the predicted 2.8% increase but slightly exceeding expectations for a 0.1% monthly rise.

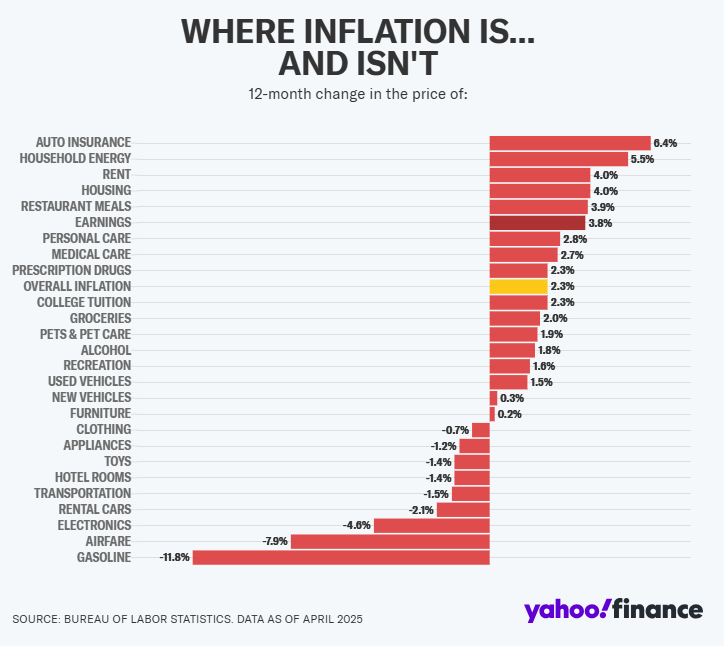

Diving deeper, the energy index increased by 0.7%, propelled by gains in natural gas (up 3.7%) and electricity (up 0.8%). In contrast, food prices fell by 0.1%, with food at home costs declining by 0.4%. Notably, five of six major grocery categories reported decreases in April, including a significant 12.7% drop in egg prices after surging costs in recent months.

The accompanying chart illustrates areas experiencing high versus low inflation effectively.

Shelter costs remain a focal point for the Fed, having increased by 0.3% in April—accounting for more than half of the total monthly increase.

Producer Price Index

The latest PPI report revealed an unexpected decrease. April saw a 0.5% drop in the PPI, contrary to expectations of a 0.3% increase. This marks the largest monthly drop in wholesale prices in over five years, tracing back to the pandemic.

Excluding food, energy, and trade, the “core” PPI dropped 0.1%, translating to a 2.9% decrease year-over-year. Economists had anticipated a 0.3% rise.

The most significant surprise was a 0.7% plunge in wholesale service costs, marking the steepest drop since 2009.

Upon further review, wholesale goods prices edged up by 0.2%, while food prices declined by 1% and wholesale energy prices fell by 0.4%. Overall, the PPI illustrates that, despite trade-related chaos, wholesale prices are dropping due to tepid economic activity and an influx of surplus goods into the U.S. ahead of the tariffs.

Retail Sales

The final report focused on April retail sales, which only increased by 0.1%. However, March figures were revised upward to 1.7% from the initially reported 1.4%.

Examining the specifics of this report, here are some noteworthy highlights:

- Sales at bars and restaurants rose by 1.2%.

- Building material and garden sales climbed by 0.8% in April, likely influenced by favorable weather.

- Sales at gas stations dipped by 0.5%, attributed to decreased pump prices.

A surprising element was the 0.1% decline in vehicle sales for April. Previous reports suggested consumers were purchasing vehicles pre-emptively to evade tariffs, but this has yet to materialize as a significant trend.

Recent Retail Sales Report Highlights Consumer Trends and Economic Pressures

The latest retail sales report reveals a mixed bag of results for April. Online sales increased by only 0.2%, while department stores and sporting goods stores experienced significant declines. These numbers indicate a volatile consumer market; however, increased spending at bars and restaurants suggests some optimism.

Sector Performance Review

Out of the 13 sectors surveyed by the Commerce Department, only five showed an increase. Given these results, many analysts are questioning the validity of the April retail sales report and considering it an anomaly.

Economic Insights and Trends

Economic analysts seem to be struggling to interpret current trends accurately. Attention has largely been focused on tariffs, obscuring signs of a weakening economy and a shifting consumer landscape, coupled with a notable decline in global interest rates.

Next month, the European Central Bank plans to cut rates again, adding to the seven rate cuts made over the past year. Meanwhile, China’s rates are at a historic low, driving concerns over deflation and potential currency devaluation.

The Federal Reserve appears hesitant to adjust rates despite mounting economic pressures. Observers hope that the global downturn in interest rates will compel the Fed to take action, especially considering high rates are a burden on consumers.

Understanding the Economic Singularity

Current economic conditions represent a significant shift, referred to as the “Economic Singularity.” This phenomenon marks a fundamental change in how wealth is generated and how labor is valued. Importantly, inflation rates do not influence this transition, whether the Fed chooses to lower rates or not.

The ramifications of these changes may profoundly impact investors, either leading to substantial losses or new wealth opportunities. Being informed and prepared is essential as these transformations accelerate across the economy.

In summary, those who grasp these unfolding dynamics will be in a better position to navigate the challenges and opportunities ahead.

Sincerely,

Louis Navellier

Editor, Market 360