The recent resurgence in Treasury yield is impacting both AT&T Inc. (NYSE:T) and Verizon Communications Inc.’s (NYSE:VZ) market performance. The fluctuations in both telco stocks are closely linked to movements in Treasury bonds due to their consistent long-term average yield differential. Despite recent declines, the intact fundamental prospects of both companies post a robust Q4 suggest an attractive setup for investing in quality dividend yield alongside potential upside appreciation.

As we approach 2024, Verizon’s recovery appears particularly promising, while AT&T is anticipated to display resilience. Verizon, often considered the “underdog” among the big three national cellular carriers, is expected to make significant strides this year. Following two consecutive quarters of reacceleration in consumer postpaid phone net adds, Verizon is poised to outshine its peers amidst emerging exhaustion in mobility subscriptions. These advancements align with new consumer division chief Sowmyanaraya Sampath’s projections of securing 1 million new customers for the segment in 2024, complementing Verizon’s improving average revenue per account and strong myPlan uptake, as well as its solid foothold in the 5G fixed wireless access (“FWA”) business.

Conversely, AT&T is encountering challenges in its postpaid phone net adds and broadband business, which prioritizes fiber internet sales. Despite these headwinds, both companies are expected to experience favorable cash flow expansion in 2024, given the conclusion of the peak capex spend on 5G investments. However, Verizon’s stronger free cash flow trajectory, historical yield differential to Treasury, and relatively better operating performance prospects position it favorably compared to AT&T.

High-Speed Connectivity Battle: Fiber vs. FWA

The traditional focus on wireless mobility has been joined by momentum in broadband, driven by the increasing demand for high performance, low latency connectivity. Both AT&T and Verizon have reaped the benefits of this trend, displaying fundamental resilience despite the challenging macro environment for consumer end-markets.

AT&T’s Struggles

AT&T’s delayed expansion into the 5G FWA market, reflecting constraints from its C-band coverage relative to Verizon and T-Mobile, has impacted its broadband business. The company’s core fiber deployments, which previously showed acceleration, have also exhibited signs of exhaustion in recent quarters. In addition, increasing FWA adoption threatens the prospects of fiber, with over 80% of new broadband subscriptions being FWA deployments in the U.S. AT&T’s broadband offerings are not as competitively priced as current FWA offerings in the marketplace, indicating a potential normalization in the pace of broadband growth at AT&T going forward.

Verizon’s Success

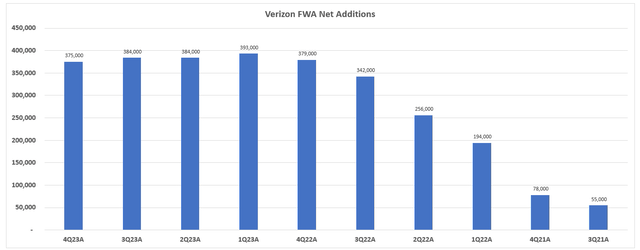

In contrast, Verizon has strategically pursued FWA opportunities since deploying 5G coverage during the pandemic, compensating for market share loss in wireless mobility. Despite trailing T-Mobile in FWA market share, Verizon commands close to 40% of related broadband subscriptions in the U.S. Its quarterly FWA net adds have consistently surpassed 300,000 for six consecutive quarters, underscoring the company’s resilience and strategic position in the market.

Verizon’s Rural Dominance and AT&T’s Mobility Woes

Amidst the ever-accelerating shift in consumer preferences toward Fixed Wireless Access (FWA) technology, Verizon has emerged as a stalwart share gainer, especially in rural areas where connectivity options are often scant. This shift has seen FWA becoming a fierce competitor to traditional broadband, with Verizon seizing the opportunity to beef up its market presence and fortify its FWA business.

FWA Value Proposition

In an era epitomized by the shadow of “digital deserts,” Verizon’s FWA has proven to be a game-changer, flexing its might as a high-performance alternative in these connectivity-starved regions. The recent data unveils Verizon’s successful capture of over 10% churn from T-Mobile, signifying its robust foothold in these remote areas.

As Verizon gears up for a full-fledged deployment of its licensed C-band spectrum across the United States markets in the latter half of 2023, its competitive edge is poised to burgeon further. Notably, the preliminary outcomes have already spotlighted enhanced performance in C-Band deployed territories, with 80% of gross consumer additions stemming from the initial 76 C-Band markets. This foresight lays the groundwork for coverage in 158 predominantly rural regions, potentially reaching over 40 million Americans, solidifying Verizon’s potential for expanding its market share.

Wireless Mobility

AT&T

Contrary to Verizon’s thriving trajectory, AT&T is grappling with a disquieting trend in its wireless mobility business. The postpaid phone net additions, previously a potent weapon in wresting market share from Verizon, witnessed erratic performance in recent quarters. This lackluster display has coincided with a tepid expansion in AT&T’s postpaid phone ARPU, hinting at the challenges it faces in harmonizing pricing strategies amidst fervent competition.

AT&T’s once-potent competitive advantage, revolving around a balanced promotional pricing strategy, is showing signs of waning allure among price-sensitive consumers. The escalating preference for T-Mobile’s Magenta unlimited data plan and its superior 5G coverage has further compounded AT&T’s predicament, intensifying the battle for market supremacy.

Verizon

Meanwhile, Verizon has adeptly sustained a stable Average Revenue Per Account (ARPA), underscoring its resilience amidst escalating competition. The introduction of value-driven subscription bundles has bolstered its wireless mobility propositions, attracting cost-conscious households seeking to streamline expenses amid prevailing economic uncertainties. This strategic move has translated into a robust performance, with total “myPlan” bundle subscribers reaching an impressive 13 million in the fourth quarter.

Amid the prevailing economic headwinds and diminishing household savings, Verizon’s offer of bundle savings on indispensable daily services has emerged as a compelling value proposition. The concurrent uptick in ARPA is anticipated to catalyze further subscription share gains, auguring well for Verizon’s top-line growth in 2024. While the recovery remains in its nascent stages, the consecutive upturn in wireless postpaid

Verizon vs AT&T: A 2024 Outlook Comparison

Assessment of Cash Flow Positions

Verizon’s recent performance has delivered reinforcing signals, fortifying its standing in the market. In stark contrast, AT&T faces a shifting landscape threatened by market share erosion due to impending contract renewals and heightened competition.

Verizon’s Free Cash Flow Growth

Verizon ended 2023 with $18.7 billion in Free Cash Flow (FCF), marking a substantial 33% increase from the prior year. This surge is a testament to Verizon’s enduring business acumen and strategic agility in response to market dynamics. The company’s optimism for sustained strong FCF generation going forward further cements its robust position in the industry.

Moreover, Verizon’s commitment to reducing capital intensity and its expected ARPA expansion are set to further bolster its FCF, providing a solid foundation for continued dividend growth and overall financial health. With a history of consistently increasing dividends for 17 years and a FCF to dividend payout ratio of 59% in 2023, Verizon’s momentum is evident, instilling investor confidence.

AT&T’s Free Cash Flow Performance

In comparison, AT&T’s achievement of $16.8 billion in full-year 2023 FCF may seem commendable at first glance. However, the company’s future outlook is clouded with uncertainties. While AT&T guides full-year 2024 FCF in the range of $17-$18 billion, questions linger about the sustainability of its near-term cash flow prospects.

The constrained margin for error in protecting dividends crucial to AT&T’s income-focused investor base adds a layer of caution to the company’s anticipated performance. This cautious outlook contrasts starkly with Verizon’s robust and optimistic trajectory, further emphasizing the divergence between the two telecom giants.

Valuation and Dividend Yield Analysis

Verizon’s stock is positioned at a slight discount compared to its telecom carrier peer group average, reflecting its historical underperformance. Despite this, the company’s sustainably growing dividend yield stands at 6.3%, further fortified by its consistent cash flow trajectory.

Conversely, while AT&T presents a similar 6.5% dividend yield, concerns loom over the durability of its cash flow prospects. The historical yield differentials to U.S. Treasury also favor Verizon, reinforcing its superior standing in comparison to AT&T.

The Better Dividend Stock: Verizon or AT&T?

In light of the comparative assessment, Verizon emerges as the more resilient and appealing dividend stock for 2024. The company’s restoration of its historical yield differential from 10-year U.S. Treasury and its favorable discount to peers highlight its strong position for dividend income and potential value appreciation.