Microsoft’s Q3 Results Highlight Azure and AI as Growth Leaders

Microsoft (MSFT) showcased impressive results in its third quarter of fiscal 2025, with Azure and AI initiatives driving the company’s growth narrative. The tech giant’s investments in artificial intelligence are producing notable returns, establishing the stock as an attractive opportunity for investors interested in the transformative potential of AI technology.

The Zacks Consensus Estimate for Microsoft’s fiscal 2025 revenues stands at $278.62 billion, reflecting a year-over-year growth rate of 13.67%. Analysts project earnings of $13.3 per share for the same period, a 1.8% rise compared to last year.

Image Source: Zacks Investment Research

Azure’s Growth Fuels Microsoft’s Expansion

Microsoft’s Intelligent Cloud segment has become the core growth engine, with Azure and cloud service revenues rising 33% (35% in constant currency), including 16 percentage points attributed to AI services. This performance highlights Microsoft’s effective implementation of its AI-focused cloud strategy and increased enterprise adoption of its comprehensive AI services.

In the last quarter alone, Microsoft processed over 100 trillion tokens, marking a fivefold increase year over year, including a record 50 trillion tokens in March. This rapid expansion in AI workloads underscores a growing demand for Microsoft’s AI infrastructure and services.

The Azure AI Foundry platform has been adopted by over 70,000 enterprises, with developers utilizing new AI models from industry leaders including OpenAI, Cohere, DeepSeek, Meta, Mistral, and Stability, enriching its AI model catalog for enterprise clients.

Navigating Competitive Pressures

Microsoft is confronting fierce competition in AI from major players like Alphabet (GOOGL) Google, Nvidia (NVDA), and Amazon (AMZN). For instance, Google’s Isomorphic Labs secured $600 million for AI-driven drug discovery using its AlphaFold technology. Nvidia is prominent in industrial AI solutions with its Omniverse Blueprint, while Amazon’s Nova Act AI agent reportedly outperforms OpenAI on internal benchmarks.

Nevertheless, Microsoft retains competitive advantages through its well-rounded cloud-AI ecosystem and cross-platform strategy. The seamless integration of productivity tools and enterprise applications creates significant value for customers, positioning Microsoft strongly in the enterprise AI market. Partnerships with industry leaders further bolster its standing. Recent collaborations with NVIDIA, including the integration of NVIDIA NIM microservices and the AgentIQ toolkit into Azure AI Foundry, enhance efficiency for AI workloads.

Moreover, Microsoft announced the general availability of its Azure ND GB200 V6 virtual machines, powered by NVIDIA’s Blackwell platform, which significantly enhances AI computing capabilities. Additionally, Microsoft and SAP have initiated the RISE with SAP on the Microsoft Azure Global Acceleration Program to streamline cloud transitions for enterprises.

Valuation and Market Trends

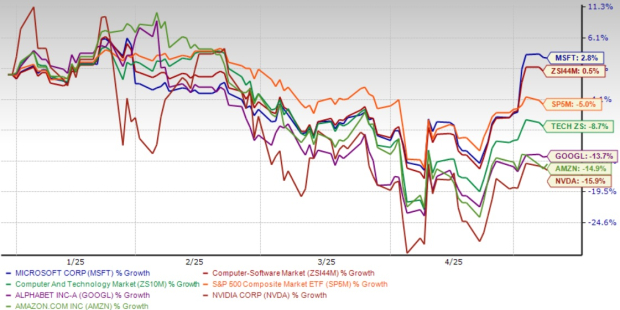

Year-to-date, Microsoft outperformed the Zacks Computer & Technology sector, achieving a 2.8% growth. In contrast, shares of Alphabet, Nvidia, and Amazon have seen declines of 13.7%, 15.9%, and 14.9%, respectively.

Strong Performance Against Peers

Image Source: Zacks Investment Research

Currently, Microsoft’s valuation stands at 10.49 times forward sales, which surpasses the Zacks Computer – Software industry average of 8.78 times. However, the solid third-quarter results indicate that Microsoft’s AI investments are starting to yield financial returns, suggesting room for future valuation growth as these initiatives develop. The company’s ability to monetize AI across various segments provides multiple avenues for stock appreciation.

AI-Driven Financial Success

Microsoft’s recent financial results narrate a robust story of AI-led growth. Total revenues hit $70.1 billion, climbing 13% (15% in constant currency) compared to the previous year. Operating income increased by 16% to $32 billion, while diluted earnings per share rose 18% to $3.46, surpassing analysts’ expectations.

The Microsoft Cloud segment alone generated $42.4 billion in revenues, a 21% increase (22% in constant currency), underscoring the company’s dominance in the cloud market. Commercial bookings rose by 18% (17% in constant currency), driven by strong executions in core sales and Azure commitments from key partners like OpenAI.

Investment Outlook: Azure’s AI Leadership

With outstanding Q3 results and ongoing investments in AI, Microsoft is emerging as a leader in the AI landscape. Azure’s AI services significantly contribute to growth, and the company is well-positioned to harness the rising trend of enterprise AI adoption. Its effective execution across the AI portfolio and solid financial returns suggest that Microsoft is a compelling investment opportunity in this evolving market.

# Microsoft’s Q3 Results Highlight AI Growth Potential and Stability

Microsoft has unveiled its third-quarter results, showcasing a robust performance and a clear strategic vision. For investors interested in transformative AI technology while preferring a reliable industry leader, these results indicate that Azure’s AI initiatives are set to significantly enhance long-term shareholder value. Currently, Microsoft holds a Zacks Rank of #2 (Buy).

High-Potential Stocks for 2024

Five stocks have been identified by Zacks experts as top picks likely to double in value in 2024. While past recommendations may have mixed results, previous selections have gained as much as +673.0%.

Many stocks in this report are under the radar of Wall Street, presenting an excellent opportunity for early investment.

For an in-depth look at these five potential opportunities, investors are encouraged to explore further.

Interested in the latest recommendations from Zacks Investment Research? Consider downloading the report on the “7 Best Stocks for the Next 30 Days.”

Key companies analyzed include:

- Amazon.com, Inc. (AMZN)

- Microsoft Corporation (MSFT)

- NVIDIA Corporation (NVDA)

- Alphabet Inc. (GOOGL)

This information was originally published on Zacks Investment Research.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Nasdaq, Inc.