Analyzing Cloud Competitors: IBM vs. Microsoft in 2025

International Business Machines Corporation (IBM) and Microsoft Corporation (MSFT) are two major entities in the cloud computing sector. IBM specializes in cloud and data solutions that support digital transformation for businesses. In addition to hybrid cloud services, IBM provides advanced IT solutions, computer systems, quantum computing, supercomputing, enterprise software, storage systems, and microelectronics.

Conversely, Microsoft’s Azure cloud platform features various hybrid solutions that facilitate the hosting of applications and workloads, alongside security and operational tools. Azure’s hybrid services include virtualized hardware for traditional IT applications and integrated platforms as a service for on-premises, edge, and multi-cloud environments.

Both companies focus on hybrid cloud and AI (artificial intelligence), positioning themselves to meet the evolving demands of enterprises. A deeper analysis of their competitive landscape will help identify which company is in a stronger position within the industry.

IBM’s Position in the Cloud Market

IBM appears well-equipped to leverage the healthy demand for hybrid cloud and AI, which boost its Software and Consulting divisions. Demand-driven growth in analytics, cloud computing, and security is likely to benefit IBM in the long term. Recently, IBM intensified its partnership with NVIDIA Corporation (NVDA) to enhance AI workloads and applications. Under this partnership, IBM plans to develop a content-aware storage (CAS) capability for its hybrid cloud system, called IBM Fusion, while expanding its watsonx integrations with NVIDIA and introducing new consulting solutions.

This CAS capability allows organizations to uncover insights from unstructured data, improving AI application capabilities without sacrificing security. Additionally, the integration of watsonx and NVIDIA Inference Microservices enables businesses to access high-end AI models across various cloud environments. The watsonx platform is set to be the backbone of IBM’s AI capabilities, optimizing productivity for enterprises.

Despite these positive aspects, IBM faces significant competition from Amazon Web Services and Microsoft Azure. Pressure from pricing competition is squeezing margins, and profitability has seen a downward trend, aside from occasional spikes. Transitioning its business model to cloud solutions remains a challenging endeavor, compounded by weaknesses in its traditional business and ongoing foreign exchange fluctuations.

Microsoft’s Growth Trajectory

Microsoft is capitalizing on cloud computing opportunities with Azure’s presence expanding to over 60 regions worldwide. This growth potentially strengthens Microsoft’s position in the cloud market. The adoption of Azure OpenAI and Copilots within Microsoft 365, Dynamics 365, and Power Platform is likely to be transformative. With Azure AI, Microsoft is constructing an application server to meet the rising demand for AI, offering diverse model selection tailored to customer needs. The number of Azure AI customers continues to grow, with over 60,000 reported, marking an increase of nearly 60% year over year.

Aggressive expansion of its cloud infrastructure is a priority for Microsoft, evident through operating data centers in more than 60 regions globally. New investments announced in Brazil, Italy, Mexico, and Sweden illustrate Microsoft’s commitment to responding to long-term demand. The ongoing partnership with OpenAI has yielded positive results, leading to a 67% increase in commercial bookings on Azure.

However, the heavy capital required for expanding AI infrastructure may put pressure on margins in the upcoming quarters. In the second quarter for fiscal 2025, Microsoft’s cloud gross margin percentage fell by 2 points to 71%, primarily due to costs associated with scaling AI infrastructure. Total capital expenditures, including finance leases, reached $20 billion, with roughly half allocated toward long-term assets supporting 15-year monetization. Despite Azure’s impressive expansion, capacity constraints within AI services pose potential limits on short-term growth.

Comparing Zacks Estimates for IBM and Microsoft

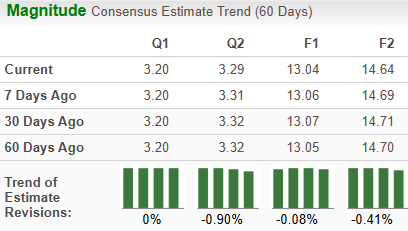

The Zacks Consensus Estimate anticipates IBM’s 2025 sales and EPS to reflect year-over-year increases of 3.1% and 3.9%, respectively. However, EPS estimates have been declining over the past two months.

Image Source: Zacks Investment Research

For Microsoft, the Zacks Consensus Estimate projects 2025 sales and EPS growth of 12.3% and 10.5%, respectively, with EPS estimates also trending downward recently.

Image Source: Zacks Investment Research

Performance and Valuation Comparisons for IBM and Microsoft

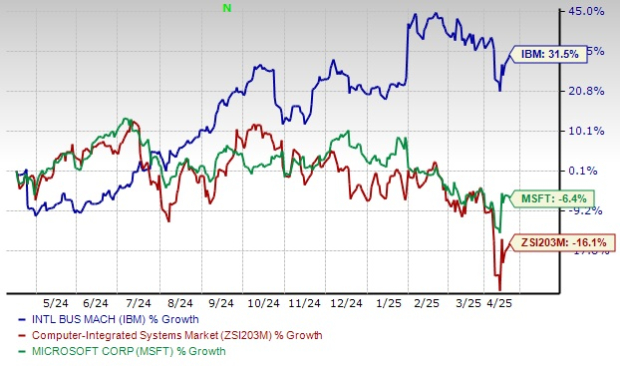

In the past year, IBM has risen by 31.5%, contrasting with the industry’s decline of 16.1%. In that same timeframe, Microsoft has seen a decrease of 6.4%.

Image Source: Zacks Investment Research

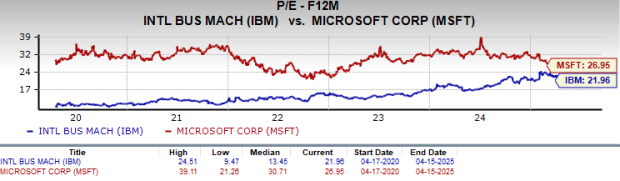

From a valuation perspective, IBM appears more appealing than Microsoft. IBM’s shares currently trade at a forward price/earnings ratio of 21.96, substantially lower than Microsoft’s rate of 26.95.

Image Source: Zacks Investment Research

IBM vs. Microsoft: Which is the Favorable Investment?

Both IBM and Microsoft hold a Zacks Rank of #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

As both firms anticipate growth in sales and profits for 2025, Microsoft has demonstrated consistent revenue and EPS growth over time, while IBM has faced challenges. Due to better performance and valuation metrics, IBM currently stands as a more favorable investment option, though both companies are rated similarly in terms of their Zacks Rank.

Zacks Names Top Semiconductor Stock

It’s only 1/9,000th the size of NVIDIA, which has skyrocketed over 800% since our recommendation. NVIDIA remains strong, but our new top chip stock has far more potential for growth.

With robust earnings growth and a growing customer base, it’s well-positioned to meet the soaring demand for Artificial Intelligence, Machine Learning, and the Internet of Things. The global semiconductor manufacturing market is expected to surge from $452 billion in 2021 to $803 billion by 2028.

see This Stock Now for Free >>

Want the latest recommendations from Zacks Investment Research? Download 7 Best Stocks for the Next 30 Days. Click to receive this free report.

Microsoft Corporation (MSFT): Free Stock Analysis report.

International Business Machines Corporation (IBM): Free Stock Analysis report.

NVIDIA Corporation (NVDA): Free Stock Analysis report.

This article originally published on Zacks Investment Research (zacks.com).

Zacks Investment Research

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Nasdaq, Inc.