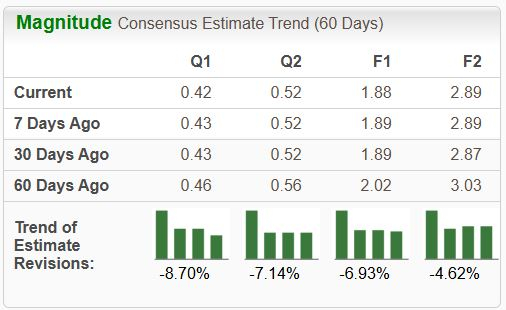

After months of waiting, investors finally learned the identity of the mystery stock Berkshire Hathaway has been scooping up over the past few quarters. The conglomerate added nearly 26 million shares of Chubb (NYSE: CB), the largest publicly traded property and casualty insurance company.

Although investors may have been hoping for something more exciting, Chubb is a prototypical Warren Buffett stock. Buffett has a special affinity for the insurance business and the cash flows they generate, and Chubb is one of the largest, most diversified insurance companies out there. Here’s why it was an ideal stock for Buffett and his team at Berkshire.

Image source: The Motley Fool.

Warren Buffett has a special place in his heart for insurance companies

Buffett has an affinity for insurance companies that dates back to his time as a student of Benjamin Graham at Columbia Business School. In 1950, Buffett bought $10,000 shares of GEICO, which he sold a couple of years later for $15,000. Buffett also credits Berkshire Hathaway’s acquisition of National Indemnity Insurance in 1967 as a pivotal turning point for the company.

The insurance business isn’t easy. Companies need to consistently weigh risks on policies and price them so they have enough room to pay for losses and squeeze out a small profit.

Because there is a period of time between collecting premiums and paying out claims, insurance companies essentially have an interest-free loan. This cash, also known as float, is “money we hold and can invest but that does not belong to us,” in the words of Warren Buffett.

As old policies lapse and new ones begin, insurers can consistently grow their cash pile and invest it in short-term assets like Treasury bills or longer-term investments like bonds and stocks. This cash generation is a big reason Buffett loves investing in the industry.

Berkshire Hathaway has invested in numerous insurance companies over the years. In 2022, the conglomerate acquired Alleghany for $11.6 billion, adding it to GEICO, Berkshire Hathaway Reinsurance Group, and National Indemnity. It also held a few insurance-focused companies in its portfolio but recently eliminated its holdings in Marsh & McLennan, Globe Life, and Markel — perhaps to clear space for Chubb.

Chubb is one of the best at pricing risk

Over time, insurance is an excellent business for those who can consistently balance the risks and rewards and underwrite profitable policies.

When evaluating an insurer’s underwriting ability, the combined ratio can be an excellent starting point. This ratio shows the claims costs plus expenses that go into selling and underwriting policies divided by the premiums collected.

The industry average combined ratio is around 100%, meaning insurers, on average, collect just enough premiums to cover their expenses and claims. When a company consistently beats its industry peers, you have a good candidate for a long-term investment.

Chubb is a diversified insurer that writes policies covering commercial property and casualty, personal lines like automotive or homeowners insurance, accident and health, agriculture, and reinsurance. The diversified insurance company has displayed a stellar history of underwriting profitable policies, with its combined ratio averaging 91% over the past two decades while consistently beating industry peers.

Chart by author.

Insurance companies can be a source of stability

Well-run insurance companies can make excellent investments because their products are always in demand. People and businesses protect against losses, and regulations often require people to have insurance, whether for auto, homeowners, or other insurance. For this reason, insurers grow along with the U.S. economy.

Insurers can also grow when inflation increases and interest rates rise. That’s because insurers see claims costs in real time and can adjust their rates when new policies begin. Since 2021, inflationary pressures have impacted insurers, causing repair and replacement costs to skyrocket. Last year, insurers saw their largest first-quarter underwriting loss in a decade and have raised their premiums in response. Over the past three years, Chubb’s net written premiums have grown 40%.

In addition, these companies have a cash pile (float) that can generate higher interest income when interest rates rise, providing them with another lever of growth in this particular environment. Last year, Chubb earned $4.9 billion in net investment income, a growth of 32% from the prior year.

Should you follow Buffett’s lead?

Berkshire’s purchase of Chubb is a solid choice that makes sense given Buffett’s prior history with insurance. Although I thought Berkshire would buy Progressive, Chubb may be a better fit. Berkshire already owns GEICO, so it may not want to invest in a direct competitor and add more exposure to auto insurance. Instead, Chubb casts a wide net, providing Berkshire with broad exposure to the industry.

The insurance business isn’t exciting, but those who do it well produce stellar cash flows — which is why investors would be smart to follow Buffett and invest in some high-quality insurance companies today.

Should you invest $1,000 in Chubb right now?

Before you buy stock in Chubb, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Chubb wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $566,624!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

See the 10 stocks »

*Stock Advisor returns as of May 13, 2024

Courtney Carlsen has positions in Progressive. The Motley Fool has positions in and recommends Berkshire Hathaway and Markel Group. The Motley Fool recommends Progressive. The Motley Fool has a disclosure policy.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.