Co-produced by Austin Rogers.

The Fed’s Shifting Narratives

Investors once bought into the Federal Reserve’s “higher for longer” interest rates narrative, regurgitating it ad nauseam on financial shows, inadvertently aiding the Fed’s market-manipulation dance.

However, dissenting voices alerted to the unfeasibility of the Fed’s hawkish tune. Forward guidance, a Fed tactic to mold market expectations, was laid bare as a smoke-and-mirrors act.

We invoked former Fed chair Ben Bernanke’s 2015 testimony – “monetary policy is 98 percent talk and only two percent action” – to illustrate the veracity behind the facade.

Ackman’s Warning and the Real Economy

Billionaire investor Bill Ackman lately echoed our sentiments, cautioning that the Fed will pivot towards rate cuts much sooner than anticipated. His vivid prediction carries two grave points: an ailing economy and a looming debt repricing debacle for highly leveraged entities.

Ackman insinuates that the non-partisan Fed will act due to economic exigencies rather than political machinations, aligning with historical precedents that peg the first rate cut in March, heralding a recession a few months hence.

Even as forecast seems overly sanguine, it accords with historical patterns, charting a similar course as past market cycles, with the stock market expected to plummet around Fall 2024 and earnings bottoming out in late 2025.

Assessing Recession Impact on REITs

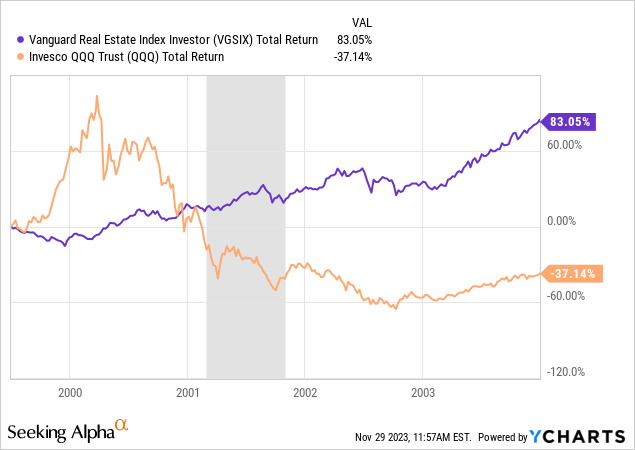

Market history confers that not all stocks suffer equally in a downturn. The impending recession could resemble the early 2000s post-Dot Com bubble burst, a notion buttressed by the performance of real estate stocks during that time.

In the wake of the 9/11 attack, REITs experienced only a tepid sell-off and swiftly rebounded, flagging their resilience even in tumultuous market conditions.

Our assessment envisions a tepid to moderate recession, unlike the cataclysmic 2008-2009 crash, offering a forecast that girds new opportunities within the REIT sector amidst broader market upheaval.

Investing in REITs: The 2024 Opportunity

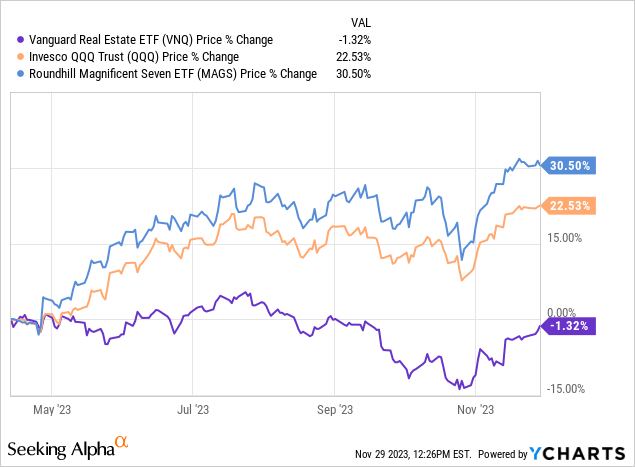

The tumultuous tango of the market often spawns unexpected opportunities, and the world of Real Estate Investment Trusts (REITs) has not been exempt from this performance pendulum. Even in the looming shadow of an impending recession, the trajectory of REITs has manifested a surprising ascendancy, confounding the naysayers and stirring the dust of a speculative whirlwind in the financial cosmos. Delving into the annals of history provides an enlightening vantage point, where the saga of 1999’s REITs selloff due to surging interest rates echoes like the ghost of financial past. Now, in the contemporary arena, akin to the turn of the millennium, a similar narrative is gradually unravelling, with interest rates likely having reached their zenith and REITs commencing their upward spiral. As the stage is set for this dichotomous dance between REITs and tech stocks, wherein the former burgeons while the latter lingers at their zenith, investors find themselves at a pivotal crossroads.

The Vanguard Real Estate ETF (VNQ) stands as a testament to this financial rumination, still shadowed by its precedent highs, while the QQQ and Magnificent 7 (MAGS) tech stocks prepare to etch new pinnacles, or perhaps have already achieved that lofty feat. This shifting landscape, reminiscent of bygone years, alludes to the possibility of 2024 “rhyming” with the early 2000s recession, wherein a paradigm shift in performance could witness REITs eclipsing tech stocks in total returns over a period of one or two years. Yet, as the crystal ball remains obfuscated, the future of the economy looms precariously over economic forecasts, reminiscent of the unpredictability of weather forecasts.

Embarking on the journey of uncovering the pearls amidst this tempestuous sea of REITs, a trove of enticing opportunities beckon, each radiating with their unique allure. Among these gems, three distinctive names emerge as the vanguard of this narrative, poised to soar into the realm of 2024 with unwavering resilience.

Exploring the REIT Opportunities

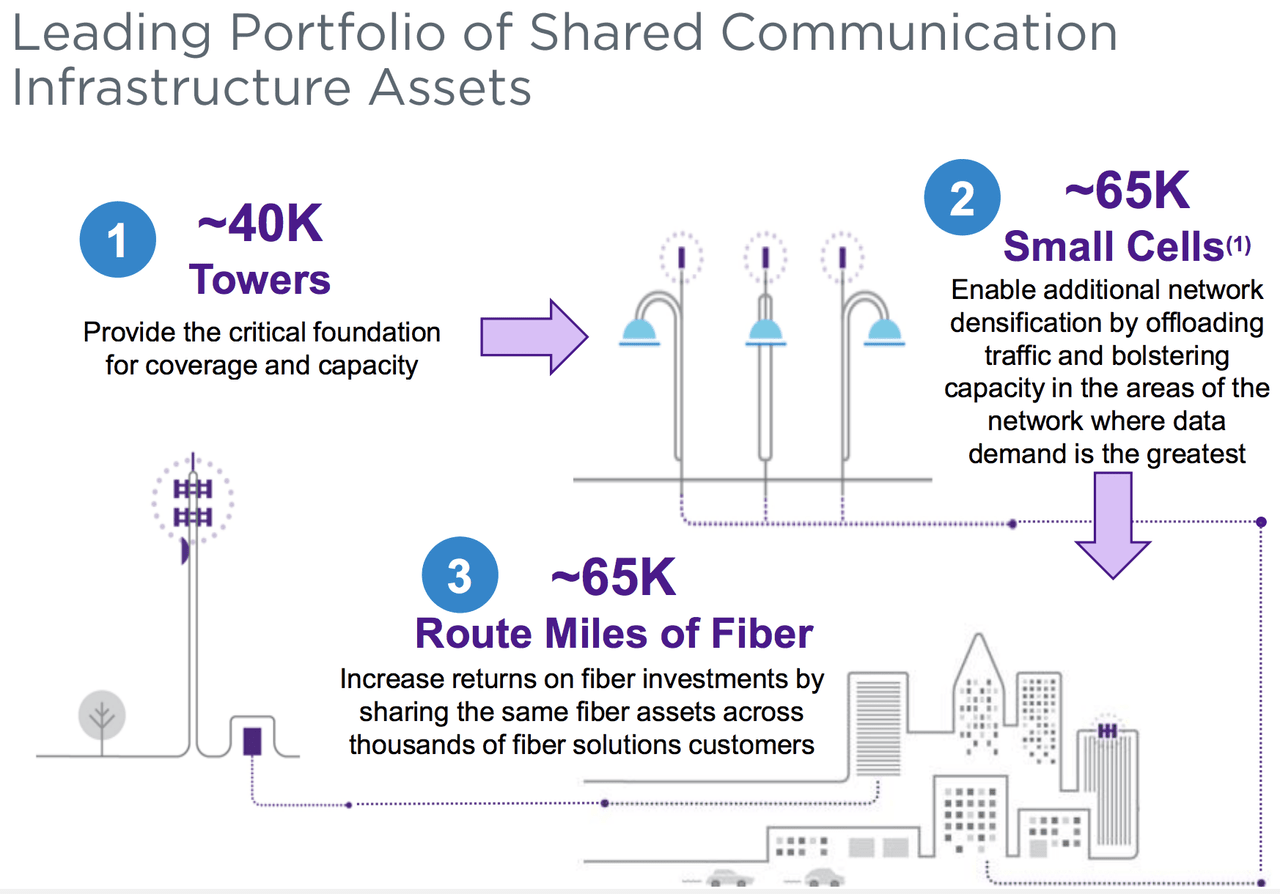

One standout amidst the myriad of REITs ensconces Crown Castle Inc. (CCI), a moniker oft-repeated in the halls of financial wisdom, owing to its unequivocal simplicity in reaping the unheralded tides of value. With an expansive U.S. telecommunications infrastructure boasting over 40,000 towers, ~120,000 small cells, and ~85,000 route miles of fiber, CCI shimmers as an archetype of latent potential, tarnished by the rise in debt costs amidst soaring interest rates. However, amidst this labyrinth of market sentiment, the entrance of activist investor Elliott Management, brandishing a stake exceeding $2 billion, poses an enigmatic proposition with the contemplation of a sale of CCI’s fiber segment, speculated to harbor a value of $11-15 billion. This tantalizing conjecture, shrouded in uncertainty, whets the appetite for prospective shareholder value, regardless of the outcome of this audacious exploration.

Entering the stage alongside CCI, Alexandria Real Estate Equities, Inc. (ARE) graces the spotlight, a testament to the egregious underestimation of value nestled within its Class A life science portfolio. An erroneous market opines the impending peril within ARE’s domain, fearing the brunt of a hybrid work arrangement slated to curtail tenant demand for life science properties, or incite a profusion of office conversions into the realm of life science. Yet, amidst this tumult, the eternal verity of physical experiments, necessitating a solace within commercial life science space, remains unscathed. Moreover, the specter of office-to-life science conversions is tethered to the eternal axiom of real estate value, entrenched within prime locations adjacent to the nerve centers of innovation and premier research universities, a sanctuary coveted by the elite echelons of the biotech fraternity. This indomitable allure of location sewn into the fabric of ARE’s edifices is impervious to the siren call of frugality, beckoning the finest biotech enterprises to its embrace.

Rounding off this triumvirate of resilience, Realty Income Corporation (O) strides forth, ensconced within the citadel of net lease REITs, and often hailed as the embodiment of excellence within this orbit. Enveloped within the cocoon of its net leases, incorporating a modest 1% average annual rent escalation and an average lease term of approximately 10 years, O unfurls its wings as a phoenix amidst the ebb and flow of interest rates. As the long-term interest rates wane, O embodies an ascent akin to the mythical bird, with the trajectory undeterred by the veils of uncertainty. Moreover, O basks in the luminescence of the highest credit rating within the net lease REIT domain, bestowing an imposing advantage upon its cost of capital, poised to burgeon amidst the cadence of descending interest rates.

A Finale of Conviction

Bill Ackman, a doyen within the financial labyrinth, echoes the sentiments we have fostered for months, heralding the encroaching shadows of a weakening economy, a dwindling consumer spending power, and the specter of an impending recession, catalyzing an expeditious descent of rates by the Federal Reserve. In the wake of this economic prelude, we have remained steadfast in our pursuit of accumulating REIT shares amidst their tenuous descent, fortuitously seizing the opportunity to procure shares at remarkable prices. Even in the wake of the November rally, an assortment of compelling buying opportunities still linger amidst REITs, sparking the unyielding conviction that these entities are poised to unfurl a resplendent resurgence in the years to come.