KKR & Co. KKR is a leading global investment firm, with a long and successful history in the private equity industry. KKR & Co. operates a diversified platform across three primary segments: Private Equity, Credit, and Alternative Asset Management.

Over the last ten years these businesses have been booming, and KKR has executed the strategies with some of the best returns across the industry. Such success has led to annualized returns of 34% over the last five years, considerably outperforming many of its competitors and the broad market.

For the average retail investor, access to private equity, credit and alternative investment opportunities are extremely limited. But with KKR now trading as a public company, any investor can get access to these powerful opportunities.

Additionally, KKR & Co. currently enjoys a Zacks Rank #1 (Strong Buy) rating, further increasing the odds of a near-term rally in the share price.

Here, I will highlight several further bullish factors powering KKR stock and share why it makes for a worthy consideration in many investors’ portfolios.

Image Source: Zacks Investment Research

Earnings Surge: Riding the Wave

The proprietary methodology used at Zacks is one of the most powerful techniques there is for picking stocks as it aggregates the earnings estimates of all analysts’ forecasts. The strategy has been quantitatively tested and shows strong market outperformance over the long term.

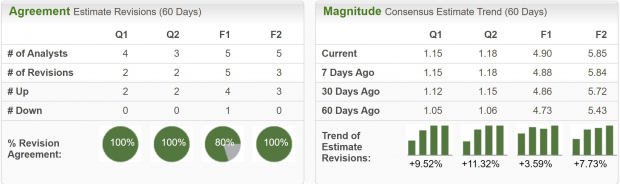

KKR & Co. boasts the highest Zacks Rank, with nearly all analysts covering the stock upgrading the EPS outlook over the last two months.

Current quarter earnings estimates have increased by 9.5% over the last two months and are expected to climb 42% YoY to $1.15 per share. FY24 earnings estimates have been boosted by 3.6% and are projected to jump 43.3% YoY to $4.90 per share.

KKR’s topline as set to expand nicely over the next two years as well, with sales forecast to grow 17.9% this year and 18.2% next year.

Image Source: Zacks Investment Research

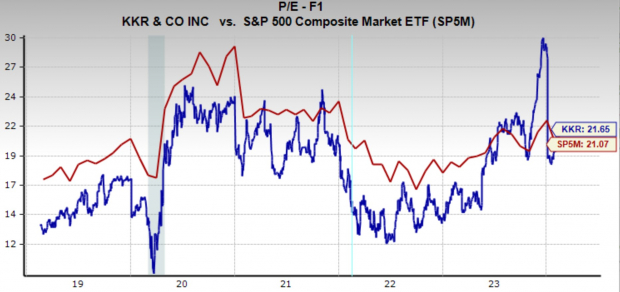

Valuation: A Diamond in the Rough

KKR is trading at a one year forward earnings multiple of 21.7x, which is about in line with the broad market. However, because of KKR’s exceptional EPS growth estimates, the stock is potentially undervalued.

EPS at the asset manager are forecast to grow 25% annually over the next 3-5 years. Not only is this an impressive growth rate, but because its below the forward earnings multiple it means its PEG Ratio is below 1x, indicating undervalued status based on the metric.

KKR currently has a PEG Ratio of 0.86x.

Image Source: Zacks Investment Research

Conclusion: The Golden Choice

Private equity and KKR’s other businesses are very strong business models and are executed at the highest level. This means investors can now access these strategies as easily as buying an ETF.

The advantages of these strategies are numerous as well. Private equity is known for offering lower volatility than public markets, potentially higher returns, and uses active management to identify the best business opportunities.

Furthermore, Credit and Alternative Assets offer additional diversification from equities. Credit provides regular income through lending, and Alternatives give exposure to projects like infrastructure.

KKR & Co. is trading at an appealing valuation, with a powerful business model, and upward trending earnings revisions. Because of these multitude of bullish catalysts, I think investors can consider investing in KKR at current levels.

7 Best Stocks for the Next 30 Days

Just released: Experts distill 7 elite stocks from the current list of 220 Zacks Rank #1 Strong Buys. They deem these tickers “Most Likely for Early Price Pops.”

Since 1988, the full list has beaten the market more than 2X over with an average gain of +24.0% per year. So be sure to give these hand-picked 7 your immediate attention.

To read this article on Zacks.com click here.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.