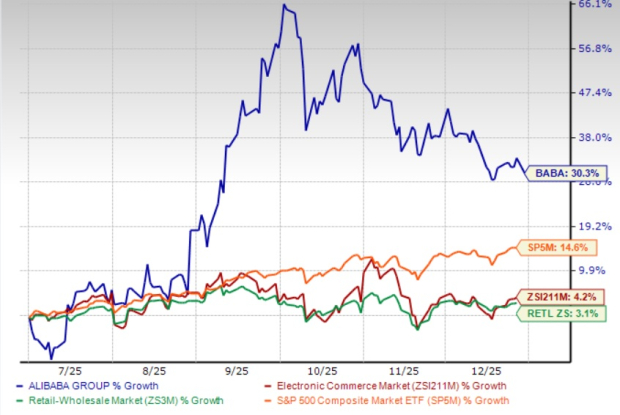

Alibaba Group Holding Limited (BABA) reported a 5% year-over-year revenue increase to RMB247.8 billion for Q2 of fiscal 2026, but faced a dramatic 71% drop in non-GAAP earnings per American Depositary Share, falling to RMB4.36. This missed analyst expectations by approximately 20%. Operating income also declined 85% from RMB35.2 billion to RMB5.4 billion, largely due to increased competition and significant investments in artificial intelligence and e-commerce.

Despite a 16% growth in local e-commerce revenues supported by government consumption stimulus measures, intensified competition from firms like PDD Holdings and JD.com has forced Alibaba to adopt costly defensive strategies. The company is pushing forward with its “10-Billion Subsidy” program to maintain market share, while also planning to expand its instant commerce infrastructure through its Cainiao logistics arm across 31 mainland Chinese cities by January 2026.

In contrast, competitors Amazon and JD.com are also expanding their logistics infrastructure but report stronger profitability metrics. Amazon has opened over 300 micro-fulfillment centers in India, garnering a 25% month-over-month increase in daily orders since September 2025. Meanwhile, JD.com surpassed 700 million active customers and demonstrated improved unit economics, with a 40% growth in shoppers during the last Singles’ Day event. Both companies appear better positioned to navigate infrastructure costs than Alibaba.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.