Market Awaits Key Nvidia Q4 Results Amid Uncertain Times

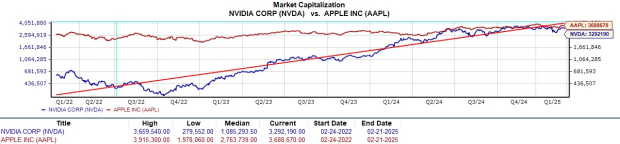

Investors are closely monitoring Nvidia’s NVDA upcoming fourth-quarter results set for release after-market hours on Wednesday, February 26. With a market cap of $3.29 trillion, Nvidia holds the largest position in the S&P 500 and Nasdaq after Apple AAPL, but its stock often experiences more significant fluctuations, which may affect the direction of broader market indices.

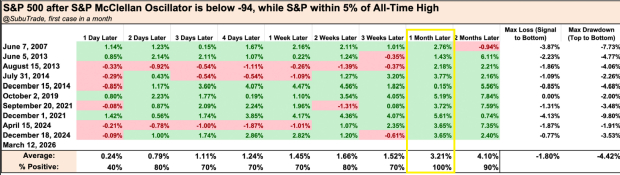

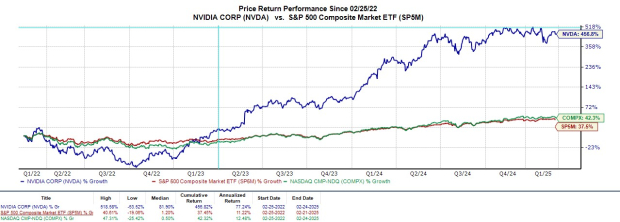

Image Source: Zacks Investment Research

The Importance of Nvidia’s Q4 Report

Nvidia’s quarterly reports typically draw attention, but this Q4 release is particularly crucial for assessing the state of the artificial intelligence boom. The recent entry of Chinese enterprise DeepSeek into the global market has raised eyebrows, as their advanced AI technology is drawing comparisons with U.S. competitors.

Rumors suggest DeepSeek’s AI models are comparable or superior in performance and efficiency to U.S. alternatives, including a chatbot that competes with OpenAI’s ChatGPT. Additionally, their services are significantly cheaper, raising concerns about the demand for Nvidia’s AI chips among U.S. firms increasing their AI investments.

Economic anxieties are resurfacing, partly due to tariff measures from the Trump administration. Following recent record highs, the S&P 500 and Nasdaq have experienced a pullback, resulting in a shift in investor sentiment.

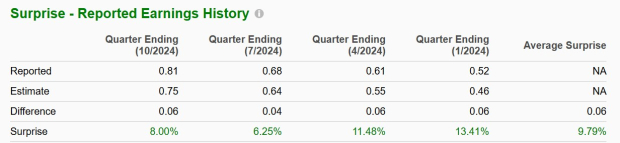

Image Source: Zacks Investment Research

Nvidia’s Q4 Sales Expectations

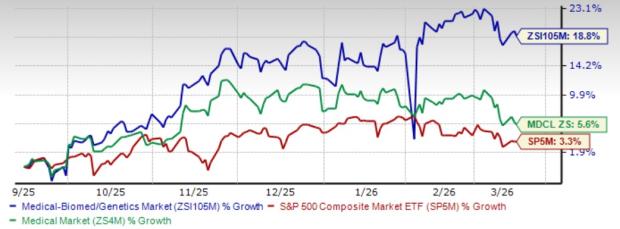

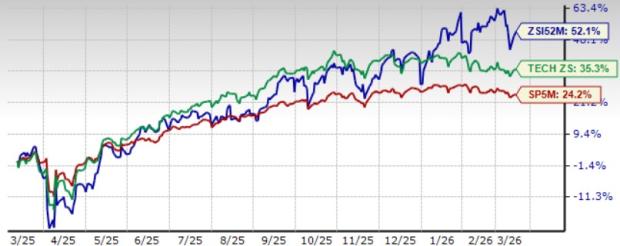

According to performance charts, Nvidia’s stock has significantly contributed to the overall growth of broader market indices recently.

Analysts anticipate a 70% increase in Nvidia’s Q4 sales to $37.72 billion, up from $22.1 billion the previous year. For earnings, projections stand at $0.84 per share, a 61% rise from the EPS of $0.52 reported last year. Impressively, Nvidia has exceeded sales estimates for 23 consecutive quarters and earnings expectations for eight quarters. The company has recorded an average EPS surprise of 9.79% in its last four quarterly reports.

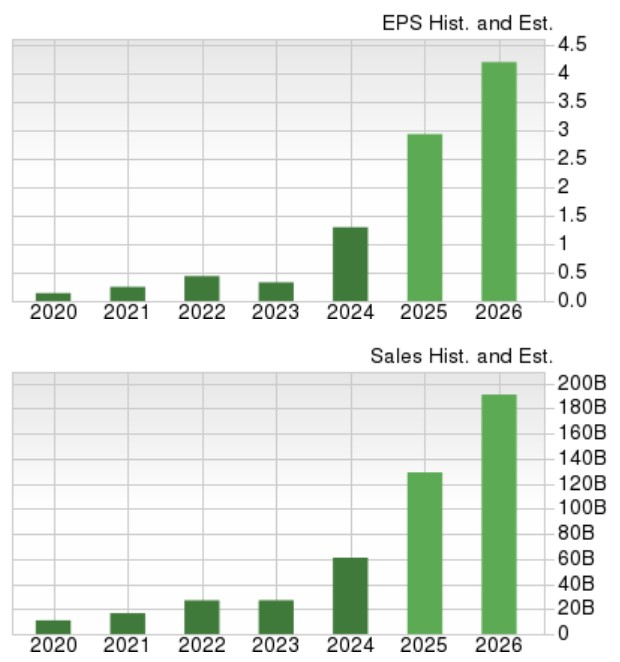

Image Source: Zacks Investment Research

Outlook for Nvidia

For fiscal year 2025, total sales for Nvidia are projected to surge 112% to $129.02 billion, up from $60.92 billion in FY24. Furthermore, annual earnings are expected to climb 126% to $2.94 per share, a notable increase from $1.30 in FY24.

Additionally, Zacks forecasts a further 48% growth in total sales for FY26, reaching $191.13 billion, with EPS growth projected at 43%, amounting to $4.21.

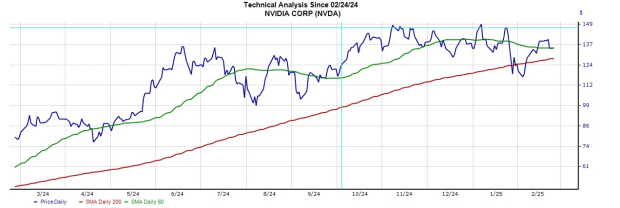

Image Source: Zacks Investment Research

Technical Insights

Currently, Nvidia’s stock is trading below its 50-day simple moving average (SMA) of around $134. Technical analysts hope for a rebound above this level to signal a positive trend. Conversely, a decline below the 200-day SMA of $128 could indicate further downturn potential for both Nvidia and the broader S&P 500 and Nasdaq indices.

Image Source: Zacks Investment Research

Conclusion

As Nvidia approaches its Q4 report, it holds a Zacks Rank #2 (Buy). The higher FY25 and FY26 EPS estimates are noteworthy, with NVDA currently trading at a reasonable P/E valuation of 31.9X forward earnings.

Strong Q4 results from Nvidia might propel the markets closer to their previous highs, but investors must remain aware of ongoing geopolitical tensions regarding Trump’s tariffs. Additionally, significant inflation data releases from Japan and Australia this week may provide further insights into global economic health.

Recently Released: Zacks’ Top Stocks for 2025

Don’t miss the chance to access our top 10 stock picks for 2025. Curated by Zacks Director of Research Sheraz Mian, this portfolio has consistently outperformed the market. Since inception in 2012, the Zacks Top 10 Stocks have gained +2,112.6%, significantly surpassing the S&P 500’s +475.6%. Mian has evaluated over 4,400 companies covered by the Zacks Rank to select the best 10 for 2025. Be among the first to view these newly released stocks with great potential.

NVIDIA Corporation (NVDA) : Free Stock Analysis Report

Apple Inc. (AAPL) : Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.