Prospects for Investment

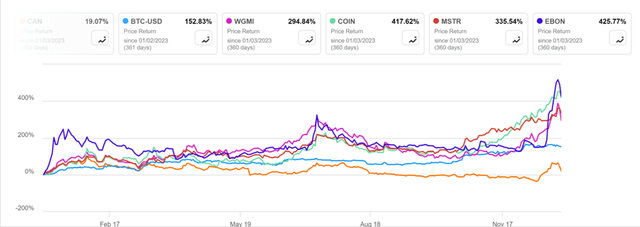

In theory, Canaan Inc. (NASDAQ:CAN) should be an ideal stock to ride Bitcoin’s bull cycle, being one of the top three manufacturers of bitcoin mining machines globally. Alongside Bitmain and MicroBT, Canaan’s stock is anticipated to closely parallel the movement of Bitcoin price. However, the stark reality has been quite the contrary: Canaan underperformed significantly and decoupled from the entire Bitcoin-related stock universe in 2023. Ironically, its smaller peer, Ebang International Holdings Inc. (EBON), soared 425% in 2023, outshining not only Canaan but also Bitcoin, Valkyrie Bitcoin Miners ETF (WGMI), leading crypto exchange Coinbase (COIN), and the Bitcoin holding company MicroStrategy (MSTR) (see chart below).

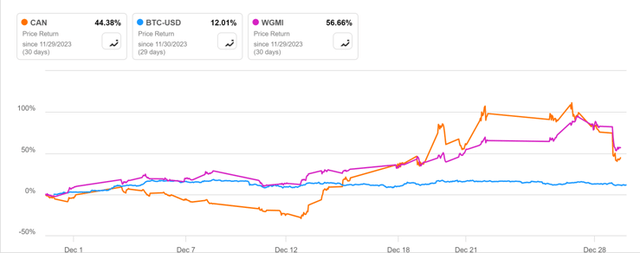

With an impending tailwind in 2024 and the industry fundamentals on the mend, the disconnect between Canaan and Bitcoin price may be fully reversed, possibly as soon as January 2024. Encouraging signs of a resurgence in momentum between the two were witnessed in December 2023, with Canaan’s stock surging by 44%.

The base case scenario for Canaan in 2024 entails reestablishing the correlation between its stock price and Bitcoin, ultimately closing the wide performance gap. In 2023, Canaan lagged Bitcoin by approximately 135 percentage points. A potential convergence of the two would imply a target price of $4.95 for Canaan, i.e., 2.6 times the closing price of $1.94 on January 12, 2024.

Comparing Canaan’s valuation with its Bitcoin-related peers using the Price to Sales ratio reveals that Canaan has the lowest P/S ratio at 1.5x, while its peers range from 2.5x to 6.0x. Trading within this range could propel Canaan’s stock price to between $3.24 and $7.76. If Bitcoin maintains its bullish trajectory in 2024, Canaan’s stock could witness further upside, considering its previous peak above $36 per share in March 2021 when it was still closely correlated with Bitcoin.

|

Market Cap * |

2024 Sales** |

Price/Sales |

|

|

Iris Energy Limited (IREN) |

$391 MM |

$162 MM |

2.5x |

|

HIVE Digital Technologies (HIVE) |

$336 MM |

$107 MM |

3.1x |

|

Cipher Mining (CIFR) |

$838 MM |

$145 MM |

5.8x |

|

Bitfarms (BITF) |

$808 MM |

$263 MM |

3.1x |

|

Canaan |

$332 MM |

$221 MM |

1.5x |

*Market capitalization as of January 12, 2024.

**Based on Seeking Alpha estimates.

Source: Seeking Alpha.

For those who missed the Bitcoin rally in 2023, Canaan, at the current level, could be a good catchup play during 2024. It is essential to note, however, that being long on Canaan is speculative, and its stock price could be exceedingly volatile despite the positive industry catalysts. With an upside target at $4.95, Canaan’s downside floor could stand at $1.13, being its all-time low since its IPO in November 2019.

The Long Dormancy of Canaan

Canaan, as one of the largest crypto mining rig manufacturers worldwide, should theoretically closely track the Bitcoin price. This is attributed to the higher the Bitcoin price, the higher the average selling price of the Bitcoin mining rigs, consequently elevating Canaan’s stock price. Additionally, Canaan is expected to benefit from scarcity value; being among the world’s top three Bitcoin mining rig manufacturers; it is the only publicly listed entity. However, the past four years have seen the reality diverge notably from this theory (refer to the chart below).

Canaan closely tracked Bitcoin in early 2020, but the correlation broke down in mid-May 2020 primarily due to the expiration of its IPO lockup period and a negative online research report. Although the correlation was somewhat re-established during the initial wave of a robust Bitcoin price rally in early 2021, it faltered, and Canaan’s stock price essentially stagnated into a deep hibernation, no longer responsive to any Bitcoin price movement whatsoever.

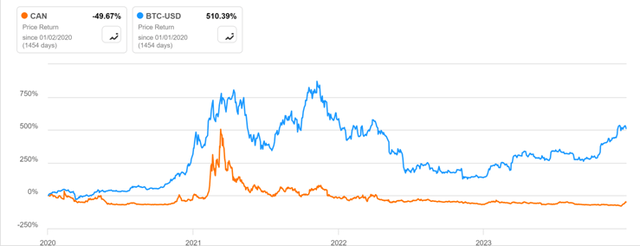

One conceivable explanation for this prolonged dormancy may be the China factor. The US Congress enacted the Holding Foreign Companies Accountable Act (HFCA) in December 2020, and the SEC issued implementing regulations in March 2021. Under this legislation, if the Public Company Accounting Oversight Board (PCAOB) fails to review a company’s audits for three consecutive years, the SEC must delist it. Suddenly, all US-listed Chinese ADRs faced potential delisting three years from March 2021. The Invesco Golden Dragon China ETF (PGJ) plummeted by 42% in 2021, dragging Canaan down by 23%, despite recording historically high revenue while Bitcoin surged 48% that year (refer to the chart below).

The Golden Age of Canaan in the Wake of Bitcoin’s Boom in 2023

2023 was a spectacular year for Bitcoin, which surged by 155%, accompanied by a remarkable rally of 295% for WGMI (see chart below). This exceptional performance led to fervent speculation about the reasons for the outperformance of WGMI, with particular emphasis on rising prices and high short interest in the underlying stocks, which could potentially result in a short squeeze as cited in the media article.

On the other hand, Canaan experienced a modest 19% increase during 2023, trailing even behind the 25% return of the S&P 500 Index (SPY). However, there was a glimmer of hope as Canaan seemingly roused from its prolonged hibernation, marking a 44% surge in December alone while Bitcoin only managed an ascent of 12%. At one point in December, Canaan even outperformed WGMI before relinquishing a portion of its gains by year-end (see chart below). If this resurgence prevails in 2024, Canaan is positioned not only to narrow the performance gap with Bitcoin but also to capitalize on the anticipated commencement of a new Bitcoin bull cycle.

Exploring Canaan’s Foundation

The Bitcoin mining business is intrinsically cyclical, and Canaan’s management has adeptly navigated the company through industry downturns and ongoing regulatory transformations. The following are our primary observations:

1) Canaan’s revenue and profit margin have been largely dictated by the fluctuating Bitcoin price.

Canaan’s revenue was predominantly influenced by the total computing power sold and the average selling price (ASP). The ASP was subject to the Bitcoin price, anticipated mining returns, and the performance of the mining rigs. Elevated Bitcoin prices and projected mining returns typically led to increased demand for mining rigs, thereby inflating the ASP. Conversely, a downturn in the cycle reduced demand and ASP. The performance of the mining rigs, though a critical factor, was not as decisive as the former two, since a superior mining rig could sometimes command a lower ASP than an older version if launched during a suboptimal period within a downcycle or following a sharp correction in Bitcoin price.

Being a fabless model, Canaan’s cost of revenues was primarily steered by raw materials and contract manufacturing costs. Typically, a newly launched mining machine model would entail higher production costs per Thash early in its product life due to initial setup costs, subsequently tapering as the production process matured and optimization improved over the ensuing years. Consequently, Canaan’s gross margin was more dependent on ASP (ultimately influenced by Bitcoin price) than production costs per Thash. As long as the ASP remains steady or trends upwards, the gross margin would increment over time. However, a substantial decline in ASP during a downturn would significantly impact the gross margin, as production costs and inventory write-down could surpass the ASP.

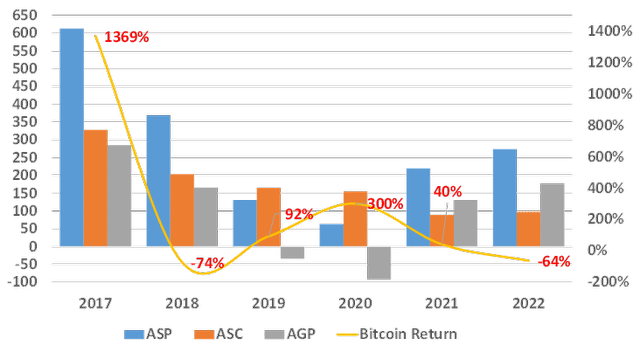

Canaan debuted as a public company in 2019, with financial data available only until 2017. Between 2017 and 2023, Canaan weathered two Bitcoin cycles, with Bitcoin reaching its peak price in 2017 and 2021, respectively (see chart below). 2024 constitutes the probable second year of the third cycle that Canaan is maneuvering through.

Bitcoin Price Cycles

In the subsequent chart, we juxtaposed Canaan’s ASP, average selling cost per Thash (ASC), and average gross profit per Thash (AGP) with the yearly return of the Bitcoin price to assess the correlation between the Bitcoin cycle and the company’s profit cycle. It is unequivocally evident that the Bitcoin price exerted a direct and substantial impact on Canaan’s gross margin. Moreover, the Bitcoin cycle led Canaan’s profit cycle by approximately a year, likely due to the production and delivery process for the mining rigs. For instance, although Bitcoin prices plummeted by 74% in 2018, Canaan still realized 166 Yuan in gross profit per Thash with a 45% gross margin per Thash that year. In 2019, the company began to feel the delayed adverse effects of the Bitcoin selloff, reporting a 34 Yuan gross loss per Thash. Ironically, Bitcoin had already commenced its ascent during that period. Canaan also reported a gross loss per Thash in 2020, primarily attributable to COVID-19 disruptions and should not be factored into the cycle.

Canaan’s Gross Margin vs. Bitcoin Return

During the second cycle, Bitcoin prices tumbled by 64% in 2022, though Canaan did not experience the tremors until 2023, reporting a gross loss of $167 million and a net loss of $242 million in the first 9 months – the highest in the past six years (see charts below). Nevertheless, with Bitcoin prices surging by 155% in 2023 and likely to rally further in 2024, given our current position in this cycle, it is reasonable to expect Canaan to transition back to a phase of gross and net profits over the next two years.

The Future of Canaan’s Mining Rig Profit Analysis and Prospects

Canaan, a leading provider of supercomputing solutions, has seen a surge in mining rig orders, signaling a potentially profitable period ahead. Let’s delve into the recent market trends, financial strategies, and industry-specific catalysts that could shape the company’s future.

Profit Analysis

The company’s profit saw a sharp incline bolstered by recent significant purchase orders. As of January 3, 2024, Canaan confirmed two substantial deals late December 2023, amounting to approximately $59 million or $67 million, including an option for additional purchases. These orders dwarfed Canaan’s 3Q 2023 revenue of $33 million, portraying an auspicious trajectory.

Financial Strategy

Canaan’s deliberate financial maneuvering, including securing a $125 million convertible preferred share deal and an At Market Issuance Sales Agreement with B. Riley Securities, magnified the company’s liquidity position amidst industry headwinds. Furthermore, the exponential growth in Bitcoin holdings to over $36 million enriched the company’s balance sheet, depicting prudence and astuteness in financial management.

R&D Commitment

Canaan’s unwavering dedication to research and development, with a team comprising over 50% of the company’s total employees, demonstrates the company’s commitment to innovation. Despite industry challenges, Canaan sustained its R&D investment, expending over $54 million during the first nine months of 2023. This steadfast approach has undeniably borne fruit, evident in the continual enhancement of mining rig performance over the last decade.

Key Favorable Catalysts

In 2024, Canaan is poised to leverage several industry and company-specific catalysts. The potential SEC approval of spot Bitcoin ETFs and the imminent Bitcoin halving could significantly benefit the company. The approval of spot Bitcoin ETFs, confirmed by the SEC by the January deadline, is projected to catalyze a positive trajectory for Bitcoin.

If history repeats itself, the price impacts of the new Bitcoin ETFs will play out surely but gradually as it will take time for those ETFs to build up their AUM and to slowly push up Bitcoin price.

The impact of these developments is paralleled by the substantial surge in demand for gold post the introduction of gold ETFs, offering a promising precedent for Bitcoin’s future amidst such financial instruments and institutional investment.

Canaan: The Potential Windfall in 2024

The recent launch of multiple spot Bitcoin Exchange-Traded Funds (ETFs) created waves in the market, impacting Canaan and related stocks. Although a short-term downside was witnessed due to profit-taking, the long-term trajectory remains promising, akin to a sturdy ship sailing through choppy seas.

Bitcoin Halving – A Game Changer

The impending April 2024 Bitcoin halving is set to reduce the mining reward, potentially driving up the Bitcoin price. Historical trends indicate that such events have led to price surges due to the reduced supply, attracting immense investor interest and propelling Canaan towards a prosperous year in 2024.

Company-Specific Catalysts

Canaan is poised to benefit from various internal factors, including an impending earnings release, the independent funding of its AI business, and the prospect of increased ETF inclusion, each contributing to the company’s positive outlook and financial appeal.

Risks and Conclusion

Undeniably, investor enthusiasm for the approved spot Bitcoin ETFs and the relationship between Canaan’s stock and Bitcoin price remain as unavoidable risks. Nonetheless, Canaan’s current position, in the wake of multiple industry catalysts, presents an enticing opportunity for investors seeking potential gains in the 2024 Bitcoin upcycle.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.