Avis Budget Group Stock Surges Following Trump’s Tariffs on Imports

Avis Budget Group CAR has seen its shares increase by over 20% this past week. This rise is attributed to President Trump’s 25% tariffs on all imported vehicles, which are expected to enhance the fleet value for this leading rental car operator.

The anticipated pricing leverage Avis will have on its rental services has contributed to positive investor sentiment.

Given its substantial earnings potential, the essential question is whether the recent rebound in Avis’s stock can sustain itself, or if it is prudent to temper expectations moving forward.

Avis Performance Overview

Despite a notable rebound from its 52-week low of $54 per share in March, Avis stock remains 43% lower than its one-year high of over $130 recorded in May. The cyclical nature of rental car operations, which fluctuate with seasonal demand, contributed to a string of three straight quarterly earnings misses, leading to the drop in CAR shares, as evidenced by the accompanying chart.

Recently, however, Avis outperformed expectations in its Q4 earnings report from February, posting an adjusted loss of -$0.23 per share instead of the anticipated -$0.96.

Image Source: Zacks Investment Research

Outlook for Avis

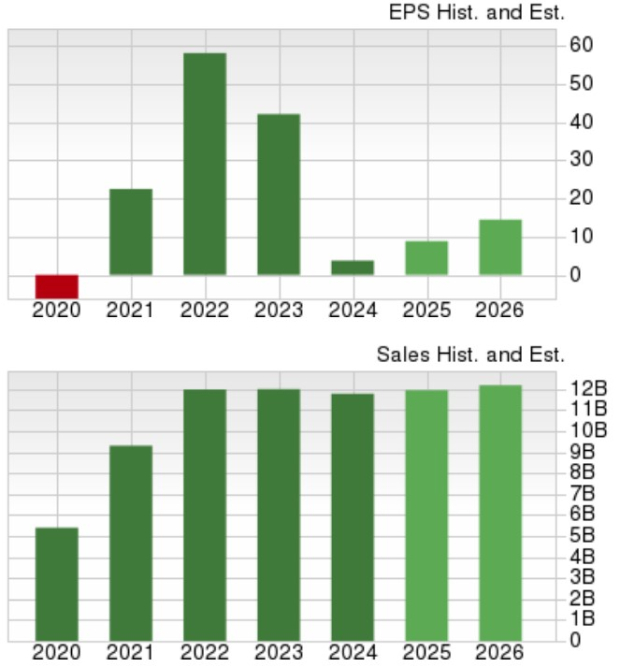

Looking ahead, Avis’s annual earnings are projected to recover dramatically, climbing to $8.84 per share this year compared to $3.74 in fiscal 2024. This anticipated rebound follows a one-time non-cash impairment of $2.3 billion last year, along with an additional $180 million in non-cash charges related to a strategic decision to expedite fleet rotations by acquiring new vehicles.

This initiative is designed to enhance operational efficiency over the long term and reduce future fleet costs, with EPS projected to rise another 63% to $14.47 in FY26. However, it is important to note that EPS estimates for FY25 and FY26 have seen downgrades over the past two months.

Image Source: Zacks Investment Research

On the revenue side, Avis is expected to see a 1% increase in total sales in FY25, followed by another projected rise of 2% in FY26, culminating in $12.2 billion in sales.

Image Source: Zacks Investment Research

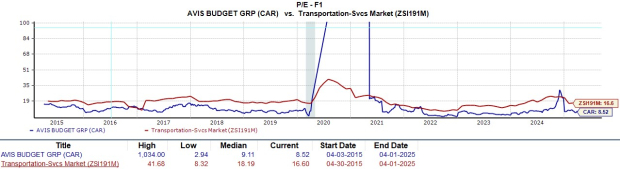

Avis Valuation Comparison

Currently, CAR trades at a multiple of 8.7X forward earnings, significantly lower than the Zacks Transportation-Services Industry average of 16.5X. Companies like C.H. Robinson Worldwide CHRW, REV Group REVG, and Hertz Global HTZ provide context for this comparison.

It’s important to note that Hertz is not currently profitable, making a P/E ratio comparison less relevant. Nonetheless, like Hertz, Avis’s stock trades at under 1X sales, which aligns with the industry average.

Image Source: Zacks Investment Research

Conclusion and Strategic Considerations

Certainly, Avis stock presents an attractive opportunity for long-term investors priced under $100 a share; however, there may be more opportune buying moments ahead. A decline in EPS estimates could indicate it is advisable to temper enthusiasm for the recent rally, suggesting potential downside risk for CAR shares, despite their appealing valuation.

Conversely, should EPS revisions trend upward, a buy rating could be justified, especially if the impact of imported vehicle tariffs positively affects the company’s operations and fleet valuation. At this time, Avis stock holds a Zacks Rank #3 (Hold).

5 Stocks Poised for Significant Growth

Each stock featured was selected by a Zacks expert as potentially gaining +100% or more in 2024. While not all selections may yield success, previous recommendations have seen notable increases, including +143.0%, +175.9%, +498.3%, and +673.0%.

Most of the stocks in this report are currently under the radar of Wall Street, presenting a prime opportunity for early investors.

Discover These 5 Potential Winners >>

Avis Budget Group, Inc. (CAR): Access Free Stock Analysis Report

Hertz Global Holdings, Inc. (HTZ): Access Free Stock Analysis Report

C.H. Robinson Worldwide, Inc. (CHRW): Access Free Stock Analysis Report

REV Group, Inc. (REVG): Access Free Stock Analysis Report

This article was first published on Zacks Investment Research (zacks.com).

The views expressed here are solely those of the author and do not reflect the opinions of Nasdaq, Inc.