The Cato Corporation Reports Fourth Quarter Losses, Stock Surges 15.8%

Shares of The Cato Corporation (CATO) have risen 15.8% since the company announced its earnings for the quarter that ended on February 1, 2025. In contrast, the S&P 500 index saw a slight decrease of 0.1% during the same period. Over the past month, Cato’s stock increased by 9.7%, significantly outperforming the S&P 500’s decline of 4.9%. This performance indicates that investors responded favorably to the company’s reduced quarterly loss and encouraging operational updates.

See the Zacks Earnings Calendar to stay ahead of market-making news.

Quarterly Performance Overview

In the fourth quarter, Cato reported a net loss of 74 cents per share, an improvement from the previous year’s loss of $1.14 per share. Quarterly sales fell by 10% year over year, totaling $155.3 million compared to $172.1 million. Adjusting for an extra week in the prior fiscal fourth quarter, sales on a comparable 13-week basis decreased by a more modest 5.1%, with same-store sales declining 0.8%. The company incurred a net loss of $14.1 million, which was narrower than the $23.4 million loss reported in the previous year.

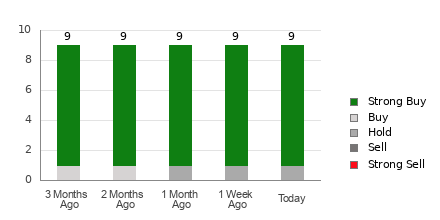

The Cato Corporation price-consensus-eps-surprise-chart | The Cato Corporation Quote

Key Business Metrics Show Mixed Trends

For the fourth quarter, Cato’s gross margin decreased to 28% of sales from 31% a year earlier. This decline was attributed to increased markdowns, higher distribution and freight costs, alongside an increase in occupancy expenses. However, selling, general & administrative (SG&A) expenses dropped by $8.8 million, improving as a percentage of sales from 39.2% to 37.8% year over year, primarily due to cuts in incentive compensation, insurance, and impairment charges despite rising professional fees.

Management Insights and Strategic Initiatives

Management has acknowledged ongoing macroeconomic challenges affecting discretionary spending, along with operational disruptions earlier in the fiscal year. CEO John Cato indicated that the company faced difficulties in its third quarter due to three hurricanes and supply chain interruptions. However, he noted that fourth-quarter trends showed marked improvement as distribution center efficiencies rebounded and previously encountered DC automation issues were resolved.

In February, the company took steps towards cost efficiency by eliminating approximately 40 corporate positions and plans further reductions. Enhancements in merchandise assortment, including new product offerings, are being prioritized to drive traffic and sales.

Challenges Behind the Financials

Cato attributed its weaker sales to persistent pressure on consumer discretionary budgets combined with external market disruptions. Increased markdown activity and high logistics costs constrained margins. Despite these challenges, expense controls in multiple categories and better investment income helped mitigate losses.

Last year, a non-cash valuation allowance against federal and state deferred tax assets resulted in a significant reduction of income tax expenses from $10.9 million in Q4 2023 to just $0.3 million in Q4 2024.

Annual Summary and Projections

For fiscal year 2024, Cato’s net loss narrowed to $18.1 million, or 97 cents per share, compared to a loss of $23.9 million, or $1.17 per share, in 2023. Full-year sales declined by 8.3% to $642.1 million, or a decrease of 6.8% on a comparable 52-week basis, with same-store sales down 3.1%.

The gross margin for the full year declined from 33.7% to 32%. SG&A expenses decreased by $21.3 million, while the company enjoyed an increase in interest and other income, which more than doubled to $11.8 million from $5.1 million the previous year.

Other Operational Developments

During fiscal 2024, Cato closed 62 underperforming stores while opening one and relocating four. As of February 1, 2025, the company operated 1,117 stores across 31 states, a reduction from 1,178 locations the prior year. For fiscal 2025, plans include opening up to 15 new stores and closing up to 50 additional locations as leases expire. Management anticipates these closures will have minimal financial impact.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.