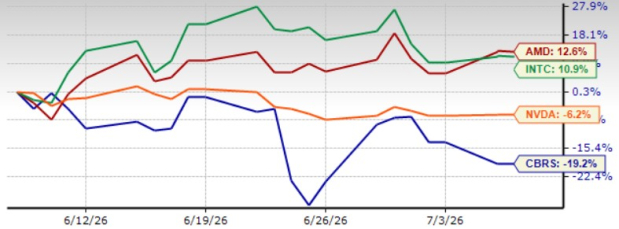

Cerebras Systems (CBRS) shares have dropped 19.2% in the past month, significantly underperforming the Zacks Business Services sector, which rose 4.5%. In the first quarter of 2026, Cerebras reported revenues of $193.4 million, up 94% year-over-year, yet incurred a loss of 4 cents per share and forecasted a decline in adjusted gross margin to 36-38% for Q2 2026. The company anticipates a gross margin of 38-41% for the full year, impacted by increased infrastructure investments and temporary capacity costs related to its $20 billion agreement with OpenAI.

The company faces execution risks with concerns about tight data-center capacity and potential effects from insider lock-up expirations post-IPO. Cerebras is also heavily reliant on a small number of customers, including OpenAI, which could affect revenue stability. CBRS’s wafer-scale architecture offers substantial processing advantages but must contend with stiff competition from NVIDIA, AMD, and Intel, who dominate the AI space.

Analysts estimate a loss of 89 cents per share for CBRS in 2026, contrasting sharply with profits forecasted for competitors like NVIDIA and AMD. Despite the recent drop, the company’s partnerships and innovative architecture may provide growth opportunities, warranting a cautious “Hold” recommendation for investors.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.