Written by Sam Kovacs.

The Story Unfolds

I published an article earlier this week titled “Sell Alert: The Slaughter of Office REITs is just beginning.”

When I began scrutinizing office real estate investment trusts (REITs) last October, I was on a dedicated quest to unearth a REIT that promised a good investment. However, systemic issues within the sector, as underscored in the aforementioned article, dissuaded me from delving into these stocks.

Since June last year, my exposure to REITs has incrementally grown, and on October 6th, just 20 days before the REITs reached their nadir, I penned a piece, “The REIT opportunity is still alive and well,” for the members of our exclusive investing group. This proved to be prescient, as the recommendations we proffered in that article have yielded quite the returns.

Make no mistake – I’m not an advocate of doom and gloom for REITs. I am of the firm belief that REITs will thrive in 2024.

Understanding the Dynamics

Post the year-end REIT rally, I felt compelled to elucidate the nuances of office REITs for investors, so they can differentiate:

- The conclusion of the Federal Reserve’s rate hike cycle and its implications for REITs (bullish).

- The lasting change in the demand for office spaces.

As interest rates trend downward, financing costs for REITs follow suit, bestowing a bullish sentiment that has been instrumental in propelling all REITs, including office REITs, skyward. This has triggered commentary, such as:

Slaughter of office REITS????? Why is the VNO share price so high???????

Let’s not conflate the sector effect with a secular shift that will play out over years.

Notably, the investor presentations by office REITs endeavor to spin the facts into a convincing narrative.

A Looming Paradigm Shift

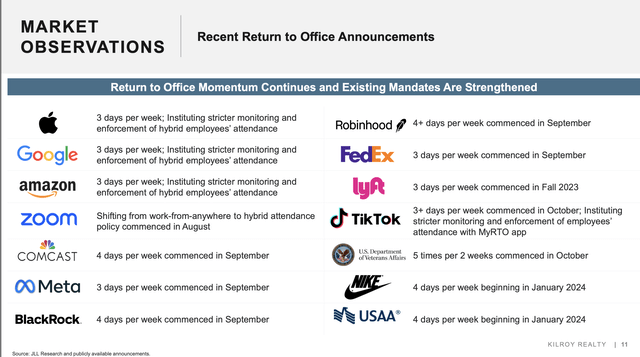

However, when I look at the slide from Kilroy Realty Corporation’s (KRC) November presentation:

From the aforementioned slide, all I can glean is that major employers like Apple Inc. (AAPL), Amazon.com, Inc. (AMZN), Meta Platforms, Inc. (META), FedEx Corporation (FDX), and Alphabet Inc. (GOOG) (GOOGL) predominantly anticipate employees to work three days a week at the office.

Scrutinizing Kastle Systems index, which surveys the number of access card swipes across 2,600 buildings and 41,000 businesses in the U.S., the return to offices has barely exceeded 50% of pre-pandemic levels.

While the chart suggests progress, the pace of recovery has been sluggish since late 2022. Based on my projections, reaching 60% of 2019 levels at the current rate of progress will extend into 2026.

Yet, even if 60% is attained next year and sustained (assuming a median hybrid three-day workweek in the office), it spells colossal trouble for Office REITs.

The demise of Office REITs will be akin to a “slow-motion train wreck,” a sentiment powerfully articulated by one of the comments on our last article. (Kudos to you, @Phil1125, for phrasing it so eloquently).

In my previous article, the crux of the criticism was that I was “late to the game,” that this was “old news,” and that it was “fully priced.”

Take heed – these are the exact sentiments echo

Some things require time. To quote Buffett, “you can’t make a baby in one month by getting nine women pregnant.”

One needs only to explore the saga of the rise and fall of malls to discern the parallels transpiring in office REITs.

Navigating the Past: The rise and fall of the U.S. Mall

The Genesis of the U.S. Mall

Post-World War II, the U.S. witnessed a monumental surge in births during the baby boom – four million new children annually, necessitating the emergence of new family infrastructures.

The GI Bill and the Federal Highway Act, both enacted in 1944, played pivotal roles: the former granting returning veterans access to low-cost mortgages, stoking a surge in homeownership, while the latter spearheaded an extensive network of highways that facilitated suburbanization.

Over a million homes were constructed annually, and these highways linked the burgeoning suburban areas to urban centers.

Ironically, amidst these grand government initiatives, central public spaces were overlooked.

The focus on homes and roads marginalized the necessity of a so-called “town square” for communal interaction.

It is against this backdrop that the U.S. mall emerged, not merely as a retailing haven, but as an emblem of American consumerism.

The first wholly enclosed mall premiered in 1956 in the Minneapolis suburbs, sparking a phenomenon. By 1960, the U.S. boasted 4,500 malls, signaling an average of three inaugurals daily since the pioneer.

In the 1970s, the introduction of the food court brought

Lessons from the Collapse of Malls: A Cautionary Tale for Investors

The acclaim of malls in the ’70s and ’80s made them a symbol of economic prosperity. At that time, malls were more than a place to shop; they were the “de facto town square,” where people congregated and connected.

The Erosion of the U.S. Mall

The decline of the U.S. mall was a two-fisted blow, starting with the gradual impact of e-commerce and culminating in the sharp trauma of the Great Financial Crisis (GFC) of 2007-2009.

- The rise of e-commerce, which was a slow and persistent trend over decades, took a toll on mall foot traffic and sales.

In 2000, e-commerce only comprised 0.8% of U.S. retail sales, but by 2019, it had leaped to 11%, and today it stands at 15%. The slow but steady encroachment of online shopping ate away at the profitability of traditional brick-and-mortar stores.

- The GFC, a sudden and severe event, exacerbated the devastation of malls, as reduced discretionary income among Americans led to a shift in consumption patterns and a focus on thriftiness.

This shift favored e-commerce, which offered the convenience of comparison shopping and lower prices. Consequently, iconic mall proprietors such as General Growth Properties found themselves filing for bankruptcy in 2009.

The aftermath of the recession unveiled a burgeoning preference for digital-first brands and the exponential growth of e-commerce giants like Amazon, exacerbating the strain on malls.

Statistics reflect the sea change: by 2013, half of Americans owned smartphones, paving the way for a surge in mobile shopping.

The closure of major anchor stores such as JC Penny and Sears in 2014 and 2015 left cavernous gaps in malls that were hard to fill, but mall owners sought to adapt by introducing experiential retail concepts like theaters and gyms.

The following years witnessed a record number of brick-and-mortar store closures, signaling the irreversible impact of e-commerce on traditional retail revenue and profits.

The abiding consequences were felt most acutely in the plummeting share prices of U.S. mall REITs, underscoring the inability of investors to distinguish between cyclical market shifts and a profound structural change in consumer behavior.

The Social Media Revolution

The rise of social media as the new virtual town square played a pivotal role in reshaping consumer interaction and further marginalizing the traditional town square represented by malls.

As people gravitated towards hobby-centric online communities, the camaraderie once fostered at physical malls dissipated, hastening their obsolescence.

The reduced need for malls as social hubs, coupled with the allure of e-commerce, sounded an inevitable death knell for these erstwhile beacons of consumerism, an omen overlooked by many.

Indeed, the evolving landscape of consumer behavior underscores the adage that yesterday’s town square is today’s social media platform.

Mall REITs: A Tale of Adaptation and Redemption

Amid the wreckage of the U.S. mall, Simon Property Group, Inc. (SPG) emerges as a testament to astute adaptation. By investing in premium properties and divesting underperforming assets into Washington Prime Group, SPG deftly navigated the storm, albeit with its share price yet to reclaim its pre-crisis highs.

The pandemic delivered another crushing blow to malls, yet the resilient ones have shown signs of recovery.

The narrative of the U.S. mall imparts invaluable lessons that could be extrapolated to the plight of Office REITs, crystallizing essential takeaways for investors in this sector.

Transposing Lessons for Office REITs

Lesson 1: The Nexus of Technological Advancement and Unforeseen Shocks

The continual march of internet technology has an unparalleled capacity to disrupt established industries. Meanwhile, external shocks can act as a catalyst, unearthing latent vulnerabilities within these sectors.

The Decline of the Paper Industry: Recession and Rate Hikes in Focus

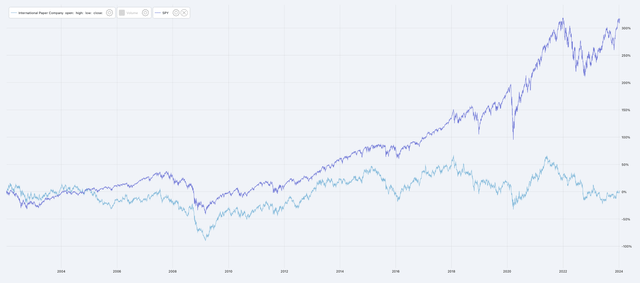

At the turn of the century, the writing was on the wall for the paper industry. International Paper Company (IP) has only matched its 1997 and 2000 highs a couple of times since then. But even if you bought in 2002, after the dust had settled, and you were looking to make a smart investment, excluding dividends, your position would be flat 22 years later. 0% returns.

Of course, the opportunity cost of being invested in a struggling asset class is just too damn high. And International Paper is the one that thrived in its industry.

Verso Corp, a leading U.S. paper producer filed for bankruptcy in 2016. Van Gelder, a large Dutch paper company, filed for bankruptcy last year in 2023.

Secular changes will grind away, and a financial shock, or a series of financial shocks, will weaken those on the losing side until they have to throw in the towel.

The Slow Unraveling of Industries

I believe this cannot be stressed enough. Companies can lay off staff. They can increase prices. They can try and tap into new markets. People who have a nice well paid management job want to keep it, and they’ll do what they can to keep the business afloat.

In real estate, we’ve seen with the malls that the unravelling takes a long time because of long-term rental contracts. 10-20 year contracts mean that only 5-10% of leases expire in any given year.

The process of creative destruction isn’t nearly as fast as some might believe.

People were already buying stuff online in 2000, but it wasn’t until 2015-2017 that the unravelling of the U.S. malls happened.

It’s a slow-motion trainwreck.

Now with offices, some Americans have been working from home for years.

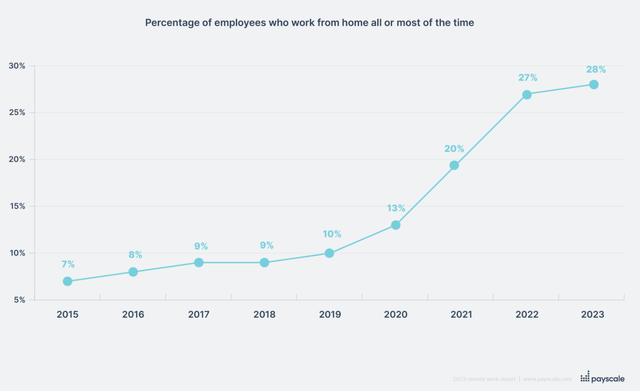

According to a Payscale survey of 400,000 employees, in 2015 7% of respondents worked from home. In 2023, it was 28%.

I’m not saying that this is representative of the whole economy, but what we’re clearly seeing at a wide scale is that there is at most 60% as much demand for offices as pre-Covid, and there has been little progress throughout 2023.

A hybrid model seems to benefit companies and employees.

Those who are talking about the productivity thing I don’t buy it. In fact, I suspect that when you see the likes of Jamie Dimon from JPMorgan Chase & Co. (JPM) expecting employees at the office, it is because he sees the potential disaster and knock-on effects on the economy and, therefore, on his business if nobody went back to the office.

It doesn’t take a lot of math to realize that if you can cut your office space by 30%, you can give up some worker productivity on the days they are not in the office, and that you’ll likely make up for it with a non-monetary induced increase in worker satisfaction.

As vacancies continue to rise with no end in sight, there is little reason to believe that the low retention rates which office REITs witnessed in 2023 will improve in 2024, 2025, or 2026.

There is a lot more pain in sight.

Pricing in Market Uncertainty

People who read these articles and say this is “yesterday’s news” and that it is already fully priced, don’t understand how markets work.

As long as more bad news is coming, it’s not priced.

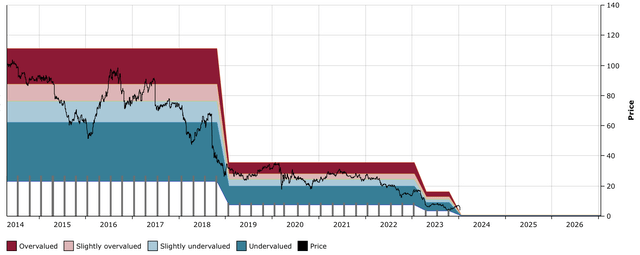

Office Properties Income Trust (OPI) is a good example of this.

You can see that every time the dividend was cut (3x now since 2019), the price took a hit when the news came out.

The writing was on the wall every time, but until something happens, there is always the possibility that it doesn’t happen.

This glimmer of hope, which blindsides long investors who don’t want to give up on their position, means that the market is “pricing” the stock with an overly confident probability of “this won’t happen.”

Then it does happen, and that probability gets removed.

As a rule of thumb in investing, when you say “this is priced in,” it usually isn’t.

The Perils of Perma-Bulls

If you have a SA premium subscription, you’ll be able to see the bullish bias of anyone (me included) that financial authors have.

It is bad business to realize you’re wrong, and because the stock market is tilted upwards, and there are 2 up days for stocks for every down day, and up days are on average up more than down days are down, there is an incentive to keep “blaming the market” on asset price movements.

You’ll find articles on Kite Realty Group Trust (KRG), for example, saying it’s a buy from 2015 to 2017. Instead you’ll have had at best a flat 7-9 years.

Taubman Centers was presented as a bull case from 2015 to 2017, at prices ranging from $68 to $55. It got bought by SPG for $43.

Look, we all make mistakes. I’m not taking jabs at any Seeking Alpha author.

We’ve had our fair share of losers. You can look at our article history, you’ll find them.

My point is, that as investors we’re all somewhat subject to the

Observations on the Office REIT Market

It’s a tough task to admit we’ve misjudged a situation, especially when we, as investment experts, have made bold recommendations in favor of certain assets. It’s akin to the famed endowment effect, where we attach greater value to something simply because we possess it. Yet, it’s crucial to recognize that even the most esteemed assets are susceptible to turmoil, as demonstrated by the downfall of U.S. malls and, more recently, the struggles faced by office real estate investment trusts (REITs).

The Fallout in the Market

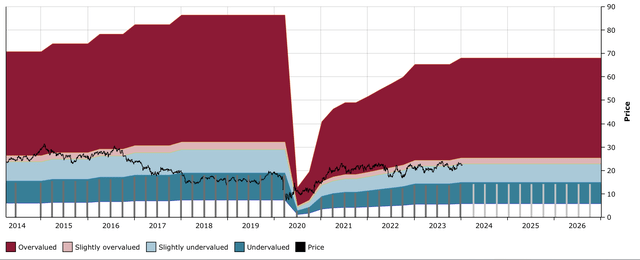

Consider the alarming decline of the U.S. mall. While it didn’t succumb to a complete demise, numerous closures were unmistakable. However, the market showcased resilience through the repurposing of assets and a shift towards an experiential business model. Those with substantial resources, possessing high-quality assets, and the capability to adapt did indeed manage to turn the tide. A prime example is Simon Property Group (SPG), the largest mall operator in the U.S., which has seen its stock price recover to pre-pandemic levels, currently standing at $143, having been suggested as a buy for investors at $130-135 in 2021.

The Office REIT Conundrum

On the flip side, office REITs face a distinct set of challenges. For instance, Boston Properties, Inc. (BXP), often lauded for its superiority in this space, represents a prime example. The pandemic’s impact has resulted in a surplus of office space, with fewer firms signing new leases. As a result, there’s intensified pressure on office real estate, affecting even the highest-quality assets.

Navigating Uncertainty

Given this landscape, investors are advised to exercise prudence with regards to office REITs. Those facing significant losses would do well to consider reducing their exposure to this market in light of the recent rally. Succumbing to the endowment effect or fear of selling at a low point may hinder the potential of redeploying funds into more promising avenues beyond office REITs. Ultimately, it is essential to recognize the changing dynamics within the market and adapt investment strategies accordingly.

In offering this perspective on the evolution of office REITs, the intent is to equip investors with a panoramic understanding of the unfolding scenario.