Colgate-Palmolive Faces Mixed Results Amid Market Trends

New York-based Colgate-Palmolive Company (CL) stands as a global frontrunner in the oral care hygiene sector. The company manufactures and distributes a wide range of household, healthcare, and personal care products. With a market capitalization of $73.5 billion, its operations cover three segments: Oral, Personal & Home Care, and Pet Nutrition.

Performance Overview

Over the past year, Colgate has underperformed the broader market, although it shows some resilience in 2025. CL stock registered a marginal 10 basis points increase year-to-date but has experienced a 2.3% decline over 52 weeks. In contrast, the S&P 500 Index ($SPX) faced a 4.7% drop in 2025 but gained 8.2% over the previous year.

Comparative Analysis with Consumer Staples

Focusing more closely, CL has underperformed the Consumer Staples Select Sector SPDR Fund’s (XLP) 3.5% gains year-to-date and 7.2% returns over the past year.

Recent Earnings and Forecast

Colgate-Palmolive’s stock saw a 1.3% increase following the release of its favorable Q1 results on April 25. Although the company’s top line suffered from currency fluctuations and reduced private label pet product volume, net sales amounted to $4.9 billion, down 3.1% year-over-year but exceeding analysts’ expectations by 1.2%. Adjusted earnings per share (EPS) rose by 5.8% year-over-year to $0.91, surpassing consensus estimates significantly. However, after this initial rise, CL stock declined by 3.1% in the subsequent trading session.

For the current fiscal year ending in December 2025, analysts predict CL will report a 1.4% increase in adjusted EPS, bringing it to $3.65. Historically, Colgate has consistently surpassed analysts’ bottom-line estimates over the past four quarters, demonstrating robust earnings performance.

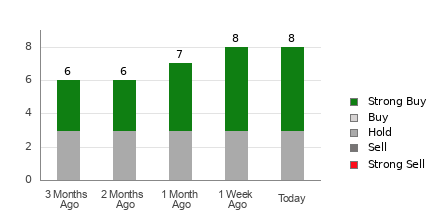

Analyst Ratings and Price Targets

CL holds a consensus rating of “Moderate Buy.” Among the 22 analysts covering the stock, opinions include 11 “Strong Buys,” two “Moderate Buys,” seven “Holds,” and two “Strong Sells.” This consensus has remained fairly stable over the last three months.

On April 28, Citigroup (C) analyst Filippo Falorni reaffirmed a “Buy” rating on CL, while increasing the price target from $103 to $108. The mean price target of $99.14 indicates an 8.9% premium over current price levels, while the street-high target of $110 suggests a potential upside of 20.9%.

On the date of publication, Aditya Sarawgi did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article are solely for informational purposes. For more information, please view the Barchart Disclosure Policy here.

The views and opinions expressed herein are those of the author and do not necessarily reflect those of Nasdaq, Inc.