Analyzing Investment Potential: General Motors vs. Ford

General Motors (GM) and Ford (F) have historically been major competitors in the American auto industry. As both companies navigate economic uncertainties and tariff implications, potential investors may wonder which stock, if any, represents a smart buying opportunity today. Both automakers have demonstrated resilience in the face of financial challenges, possess substantial liquidity, and are adapting to the electric vehicle (EV) market. This article examines their fundamentals, growth trajectories, and challenges.

Why Choose General Motors?

In 2024, General Motors solidified its position as the top-selling automaker in the United States, increasing its full-year market share by 30 basis points to 16.5%. The company reported a record annual earnings per share (EPS) of $10.60, marking a 38% increase. Looking ahead, GM forecasts an EPS between $11 and $12 for 2025.

General Motors is making significant strides in its electrification strategy. By the end of 2024, the company’s EV portfolio achieved variable profit positivity. GM produced 189,000 EVs last year, with plans to increase that to 300,000 in 2025. They also expect a reduction in EV operating losses by about $2 billion this year. Strategic partnerships with Vianode, Lithium Americas, LG Chemical, POSCO Chemical, and Livent are strengthening GM’s EV supply chain, aligning with its long-term goals.

The company’s restructuring efforts in China are bearing fruit, having reported positive equity income there last quarter, excluding $5 billion in restructuring costs. GM aims to return its China operations to profitability within this fiscal year. The company met its $2 billion cost-cutting target by the end of 2024, anticipating $1 billion in ongoing savings from halting robotaxi developments and refining its autonomy strategy. As of last year, GM closed with total automotive liquidity of $35.5 billion, which includes $21.7 billion in cash, and returned $7.6 billion through dividends and share buybacks. Notably, GM announced a 25% increase in dividends along with a $6 billion buyback program, with $2 billion expected to be completed by the second quarter of 2025.

However, projections indicate a slight decline in internal combustion engine (ICE) wholesale volumes in North America, though growth in EV sales may serve as a counterbalance. GM anticipates a 1% to 1.5% year-over-year decline in pricing, which could lead to increased incentives and pressure on profit margins.

The Case for Ford

Ford emerged as the third-best seller in the U.S. market in 2024, with just over 2 million vehicles sold. The company’s strong lineup, which includes F-series trucks and SUVs, is set to expand with new models like the Maverick, Bronco, and Expedition Navigator. Ford is also focusing on growth in its Pro business across vehicles, software, and physical services, leveraging software and technology as key drivers.

At the end of 2024, Ford reported approximately $28 billion in cash and a total liquidity of around $47 billion. The company successfully reduced its net costs by $500 million in the latter half of 2024 and has identified $1 billion in design cost savings for 2025. Ford’s dividend yield remains attractive, exceeding 6%. Yet, significant near-term challenges loom.

The Model e segment is currently struggling, facing fierce competition, pricing pressures, and high costs from new EV developments. After sustaining $4.7 billion in losses in 2023, Ford’s losses in this segment increased to $5.07 billion in 2024, with expectations of losses between $5 billion and $5.5 billion for the coming year. Additionally, the Ford Blue division shows signs of slowing momentum, with projected EBIT of $3.5 billion to $4 billion in 2025, down from $5.3 billion in 2024, as the company anticipates a decline in ICE vehicle sales.

In February, Ford announced plans to inject up to €4.4 billion ($4.8 billion) into its German operations to strengthen competitiveness and reduce debt. However, the European auto market faces pressures from rising costs, weak demand, and intensified competition from Chinese EV manufacturers. The effectiveness of Ford’s capital investment in revitalizing its European presence remains uncertain.

Comparative Estimates: Ford vs. GM

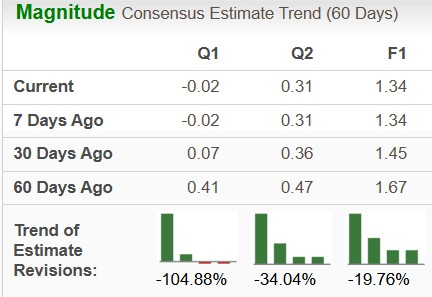

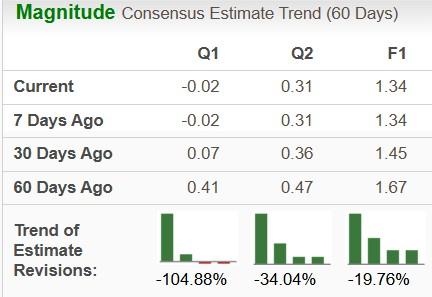

The Zacks Consensus Estimate for Ford indicates a potential year-over-year decline in 2025 sales and EPS by 4% and 27%, respectively. This bearish trend in EPS estimates has been observed over the last 60 days.

Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

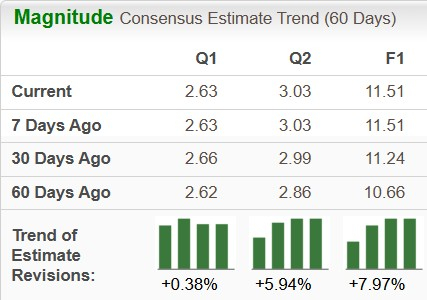

Conversely, the Zacks Consensus Estimate for General Motors shows a 4% year-over-year decline in sales for 2025, but anticipates a 9% increase in EPS, with upward trends in EPS estimates over the last 60 days.

Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

Valuation Comparison: GM vs. Ford

General Motors is currently trading at a forward earnings multiple of 4.06X, which is below its three-year median of 4.96X. In contrast, Ford’s forward earnings multiple stands at 7.25X, above its median of 6.44X during the same period.

Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

Preparing for Tariff Challenges

The impending 25% tariff on auto imports is poised to disrupt the automotive supply chain, affecting both GM and Ford. GM appears better positioned, having reduced its international inventory by 30% to mitigate exposure to abrupt cost increases. The company is also enhancing its supply chains through collaborations with logistics partners. Ford’s CEO, Jim Farley, has expressed concerns, stating that tariffs would lead to “a lot of cost and a lot of chaos” within the U.S. auto industry. This situation is likely to escalate raw material costs, ultimately raising vehicle prices and potentially dampening demand and profitability.

Conclusion

General Motors has made noteworthy progress through cost-cutting initiatives and strategic partnerships, positioning itself favorably in the evolving auto market. In contrast, while Ford is expanding its product offerings and focusing on software and services, it faces considerable challenges, especially in its EV segment and broader competitive environment. Investors should carefully weigh these factors when considering investments in either company.

General Motors Outshines Ford Amidst Electric Vehicle Market Challenges

General Motors (GM) demonstrates strong momentum in the electric vehicle (EV) sector and shows improved results in China, establishing itself as a resilient contender against market difficulties. GM is proving to be more operationally efficient compared to its rival Ford, notably with strategies that effectively navigate the current tariff environment.

In contrast, Ford faces significant losses within its EV segment and experiences heightened challenges from pricing pressures and intensifying competition. Furthermore, GM’s valuation is currently more attractive, bolstered by upwardly revised earnings estimates that foster investor confidence. These elements suggest that GM presents a more favorable investment opportunity than Ford at this time.

Currently, GM holds a Zacks Rank of #3 (Hold), while Ford is significantly lower at a Rank of #5 (Strong Sell).

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here

7 Best Stocks for the Next 30 Days

Experts have just released a curated list of 7 elite stocks from the current pool of 220 Zacks Rank #1 Strong Buys. These selections are labeled “Most Likely for Early Price Pops.”

Since 1988, this comprehensive list has outperformed the market, achieving an impressive average gain of +24.3% per year. It is advisable to pay immediate attention to these carefully selected 7 stocks.

See them now >>

Interested in the latest recommendations from Zacks Investment Research? You can download the report entitled “7 Best Stocks for the Next 30 Days” for free. Click here to access this resource.

For analysis on Ford Motor Company (F), you can find a Free Stock Analysis report.

For insights on General Motors Company (GM), you can also access a Free Stock Analysis report.

This article originally appeared on Zacks Investment Research (zacks.com).

Zacks Investment Research

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Nasdaq, Inc.