Semiconductor Industry Booms: Analyzing Intel vs. Nvidia for Investment

The semiconductor sector is experiencing remarkable growth due to the increasing demand for artificial intelligence (AI) solutions. In 2024, the industry reported a 19% year-over-year revenue growth, reaching $627 billion, with expectations to soar to $981 billion by 2029.

Two major players in this expanding market are Intel (NASDAQ: INTC) and Nvidia (NASDAQ: NVDA). Intel has held a dominant position in the PC sector for decades, while Nvidia’s semiconductor chips gained traction with the rise of AI applications.

Where should you invest $1,000 today? Our analyst team recently unveiled the 10 best stocks to consider for investment right now. Learn More »

This article evaluates both companies to determine which presents a better long-term investment opportunity in the semiconductor space.

Analyzing Intel: Strengths and Weaknesses

Intel’s shares appear undervalued, especially with a price-to-book (P/B) ratio of 0.87 as of now. This suggests that the stock is priced below its asset value.

However, Intel faced challenges in fiscal 2024, which ended on December 28. Its revenue declined to $53.1 billion from $54.2 billion in fiscal 2023, a disappointing outcome given the booming AI landscape.

A key factor behind this drop was Intel’s struggling foundry business. Unlike Nvidia, which is a fabless chipmaker and outsources chip production, Intel operates its own foundries.

Specifically, Intel’s foundry revenue decreased to $17.5 billion in 2024 from $18.9 billion in the previous year. Rising costs in tandem with reduced sales pressured Intel’s gross margin, which fell to 32.7% in fiscal 2024 from 40% the year before. Consequently, the company reported a net loss of $19.2 billion.

On a positive note, Intel is expanding into manufacturing chips for other companies, with notable clients including Microsoft and Amazon. These companies are interested in custom chips to support their AI initiatives.

Excluding the foundry segment, Intel’s semiconductor products achieved a 3% year-over-year revenue growth, totaling $48.9 billion in fiscal 2024. The anticipated launch of its new PC chip, Panther Lake, later this year, may bolster sales in fiscal 2025.

Nvidia’s Advantages

Nvidia has carved its niche in the AI sector, achieving an extraordinary revenue of $130.5 billion in its 2025 fiscal year, which ended on January 26, marking a remarkable 114% year-over-year increase.

Without the burden of foundry operations, Nvidia boasts a robust gross margin of 75% for fiscal 2025, up from 72.7% the previous year, resulting in a net income rise of 145%, totaling $72.9 billion.

The company’s financial performance is complemented by the recent launch of the Blackwell Ultra platform in March. This advanced technology allows AI to tackle complex problems by breaking them down into manageable steps, leading to improved responses. It signifies a shift toward AI reasoning, moving beyond mere data pattern recognition.

As companies strive for enhanced computing capabilities, Nvidia’s Blackwell Ultra caters to these demands, with tech giants like Microsoft and Amazon already adopting the platform.

Comparing Intel and Nvidia for Investment

When assessing Intel versus Nvidia, Intel’s stock appears undervalued, but its operational results have lagged. For example, Intel estimates fiscal first-quarter revenue between $11.7 billion and $12.7 billion, compared to $12.7 billion generated in the same quarter last year, indicating stagnant sales.

Conversely, Nvidia is set for continued growth. The company projects first-quarter sales of approximately $43 billion, reflecting a 65% increase from the previous year’s $26 billion.

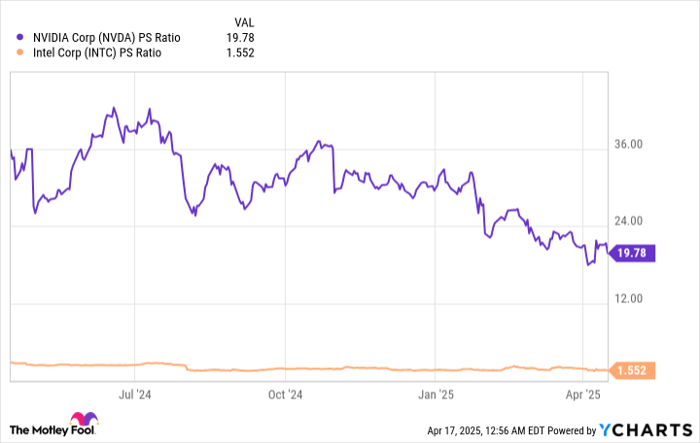

Additionally, recent stock market fluctuations have reduced Nvidia’s share price, making its valuation more appealing. An analysis of the price-to-sales (P/S) ratios for both companies shows that Nvidia’s P/S ratio is nearing a historical low, while Intel’s remains significantly lower—but this is symptomatic of its recent business struggles.

Data by YCharts.

Intel has the potential for a turnaround with the introduction of new CEO Lip-Bu Tan in March. However, notable improvements may take years under new leadership.

In contrast, Nvidia’s upward trajectory combined with innovative technologies like the Blackwell architecture positions it as the more favorable investment in the long term within the semiconductor sector.

Is Nvidia the Right Stock for Your $1,000 Investment?

Before you consider investing in Nvidia, take this into account:

The Motley Fool Stock Advisor team identified what they believe are the 10 best stocks available now, and Nvidia was not part of that list. Their selected stocks are projected to yield significant returns in the coming years.

Remember when Netflix was recommended on December 17, 2004… an investment of $1,000 then would now be worth $524,747!* Or when Nvidia was recommended on April 15, 2005… an investment of $1,000 would have grown to $622,041!*

Notably, Stock Advisor has achieved a total average return of 792%—significantly surpassing the 153% return for the S&P 500. Don’t overlook the latest top 10 list, now accessible when you join the Stock Advisor.

Explore the 10 recommended stocks »

*Stock Advisor returns as of April 21, 2025

John Mackey, former CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool’s board of directors. Robert Izquierdo has positions in Amazon, Intel, Microsoft, and Nvidia. The Motley Fool has positions in and recommends Amazon, Intel, Microsoft, and Nvidia. The Motley Fool also recommends the following options: long January 2026 $395 calls on Microsoft, short January 2026 $405 calls on Microsoft, and short May 2025 $30 calls on Intel. The Motley Fool’s disclosure policy is available for reference.

The views and opinions expressed herein are those of the author and do not necessarily reflect those of Nasdaq, Inc.