Micron Technology, Inc. reported fiscal third-quarter 2026 revenues of $41.46 billion, marking a 74% increase sequentially. The company attributes this growth to strong demand for AI memory products, with a projected revenue of $50 billion for the fiscal fourth quarter. Micron’s gross margin improved to 84.6%, up from 37.7% in the previous year, and it generated a robust operating cash flow of $25.39 billion.

Meanwhile, Taiwan Semiconductor Manufacturing Company Limited (TSMC) reported second-quarter 2026 revenues of NT$1.27 trillion, up 36% year over year, and net income of NT$706.56 billion, reflecting a 77.4% increase. TSMC is also witnessing strong demand for its advanced semiconductor chips, which positions it well within the expanding AI ecosystem. The company’s net margin was reported at 55.6% for the quarter.

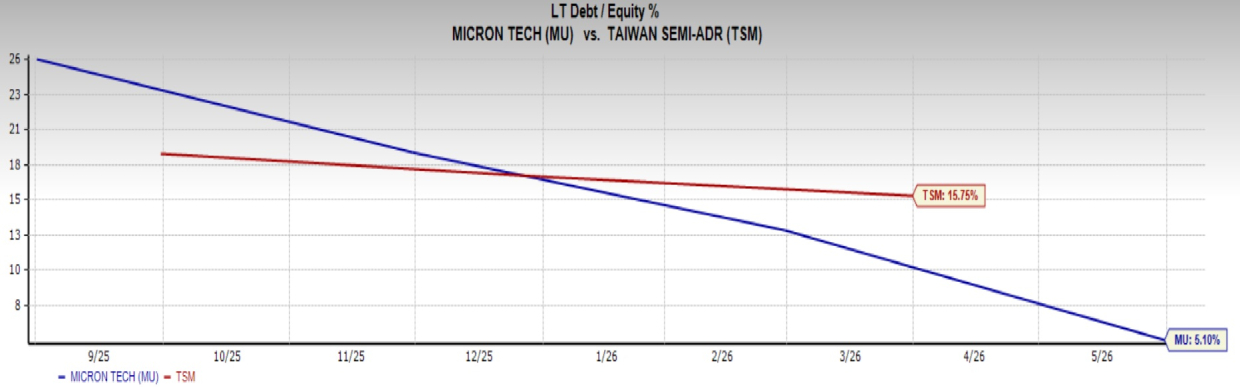

Despite the impressive performance by both companies, Micron is seen as a better investment due to its lower debt-to-equity ratio of 5.1% compared to TSMC’s 15.8%. Micron also has a higher return on equity (ROE) of 72.5%, surpassing TSMC’s 40.9%, and is more attractively valued with a forward price-to-earnings ratio of 11.55 compared to TSMC’s 26.62.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.