The Allstate Corporation ALL enjoys a sweet spot as it benefits from a variety of factors such as expanding insurance premiums, a thriving Protection Services business, and strategic acquisitions. A robust financial standing further solidifies the case for holding onto ALL shares.

Performance Ratings and Market Resilience

Presently, Allstate holds a Zacks Rank #3 (Hold).

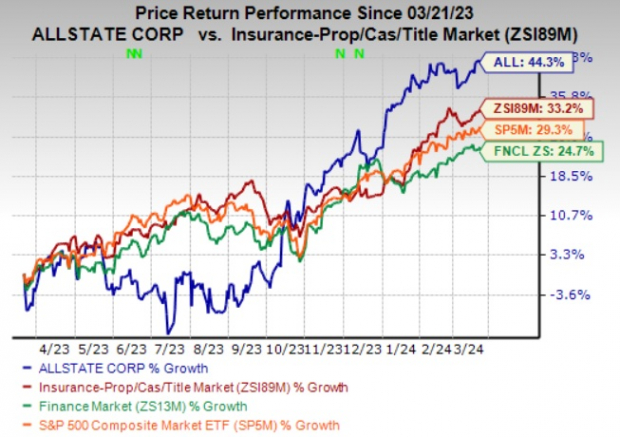

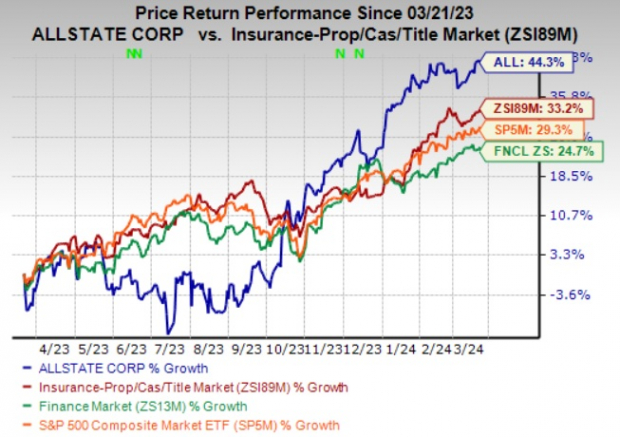

Over the past year, the stock has outperformed the industry, securing a substantial 44.3% increase. In comparison, the Finance sector and S&P 500 index experienced growth rates of 24.7% and 29.3%, respectively, during the same period.

Image Source: Zacks Investment Research

Favorable Style Score and Growth Projections

ALL displays promising potential with an impressive VGM Score of B, incorporating Value, Growth, and Momentum metrics. The score is a composite evaluation of these three vital factors.

Robust Future Prospects

Analysts project Allstate’s earnings in 2024 to reach $12.97 per share, indicating a substantial 14-fold surge from the previous year. Revenue forecasts are equally impressive, with estimates pointing to a 10.1% increase to $63.2 billion.

The outlook for 2025 is equally bright, with estimated earnings of $16.45 per share, signaling a robust 26.8% growth from the prior year. Revenue forecasts for 2025 also suggest a healthy 7.3% rise to $67.8 billion.

Strong Track Record of Earnings Beat

In the last four quarters, Allstate surpassed earnings expectations thrice and fell short once, with an average surprise of 43.92%.

Promising Market Trends and Business Strategies

Allstate’s revenue growth is propelled by strategic rate increases, particularly in property and casualty insurance premiums, which surged by 10.3% in 2023. Management remains bullish about further rate hikes in 2024 within its auto insurance division, enabling the company to navigate inflation-related challenges effectively.

Furthermore, the insurer benefits from increased returns on fixed income securities, driving a 3.1% YoY growth in net investment income in 2023. The Allstate Protection Plans are also performing well, reflecting a 9.2% growth in revenues in 2023.

Through strategic acquisitions like National General in 2021, Allstate is expanding its footprint and revenue streams. Additionally, divestitures, such as the sale of life and annuity businesses in 2021, allow the company to focus on high-growth areas within the personal property-liability segment.

Embracing digital transformation, Allstate is trimming operational costs and redirecting resources towards growth and technological advancements. Such initiatives strengthen its financial position and drive shareholder value through buybacks and dividend hikes, exemplified by a recent 3.4% quarterly dividend increase in February 2024.

Noteworthy Industry Peers and Final Thoughts

Other top-performing stocks in the insurance sector include Skyward Specialty Insurance Group, Inc. SKWD, Corebridge Financial, Inc. CRBG, and W. R. Berkley Corporation WRB. Skyward Specialty boasts a Zacks Rank #1 (Strong Buy), while Corebridge and W.R. Berkley hold a Zacks Rank #2 (Buy). These companies have demonstrated strong financial performance and stock appreciation over the last year.

Zacks Names #1 Semiconductor Stock

Highly promising growth opportunities and sound fundamentals make Allstate a compelling investment option in the current market environment. Coupled with its strategic initiatives and solid financial foundation, ALL stock shows great promise for long-term investors looking for stable growth.

Read the original article on Zacks.com here.

Check out Zacks Investment Research for more insights.

Please note that the opinions and views expressed in this article are based on the author’s analysis and may not necessarily align with those of Nasdaq, Inc.