Today’s Market Highlights: Apple, Meta, Chevron, and Micro-Caps Under Review

Thursday, March 20, 2025

The Zacks Research Daily showcases key insights from our analyst team. In today’s edition, we spotlight the latest reports on 16 significant stocks, including Apple Inc. (AAPL), Meta Platforms, Inc. (META), Chevron Corp. (CVX), and two micro-cap companies: Taylor Devices, Inc. (TAYD) and GSI Technology, Inc. (GSIT). Notably, Zacks micro-cap research offers unique insights into these lesser-known firms, standing out as the only research of its kind in the country.

Our reports have been carefully selected from approximately 70 publications by our analysts today.

You can access all of today’s research reports here >>>

Ahead of Wall Street Insights

The daily ‘Ahead of Wall Street’ article is essential for investors keen on understanding the day’s trading landscape. Released before the market opens, it analyzes the morning’s economic reports and their anticipated impact on market performance. Readers can enjoy this article for free on our homepage and sign up to receive email notifications each morning.

Read today’s AWS article here >>> Pre-Markets Lower; Economic News Decent

Featured Stock Research Reports

Apple Inc. shares have outperformed the Zacks Computer – Micro Computers sector over the past year, rising 26.7% compared to the industry’s 24.8% growth. Apple is experiencing robust growth in its Services revenues, boasting over 1 billion paid subscribers—more than double from four years ago.

The expansion of content for Apple TV+ and Apple Arcade has been pivotal in this subscriber increase. For the March quarter (second-quarter fiscal 2025), Apple anticipates revenue growth in the low to mid-single digits year-over-year, with its Services segment expecting a double-digit growth rate.

Additionally, the launch of Apple Intelligence, an advanced personal intelligence system integrated into iOS 18, iPadOS 18, and macOS Sequoia, may further enhance its stock value. However, a decline in iPhone sales in China and regulatory challenges present risks.

(You can read the full research report on Apple here >>>)

Meta Platforms, Inc. has seen its shares exceed the Zacks Internet – Software industry growth, increasing by 20.1% versus 3.8%. Steady user growth across all regions, particularly in Asia Pacific, with enhanced engagement in platforms like Instagram and WhatsApp has significantly contributed to this success.

Meta is also leveraging artificial intelligence to enhance the effectiveness of its offerings; their services are now utilized by over 3.35 billion people daily. The increasing presence of AI features, particularly among younger audiences, bolsters its competitiveness and advertiser appeal, driving potential revenue growth.

While Meta plans substantial investments in AI over the coming years to develop advanced technology, the timeline for monetizing these features remains uncertain.

(You can read the full research report on Meta Platforms here >>>)

Chevron Corp.‘s stock has outperformed the Zacks Oil and Gas – Integrated – International sector in recent months, with a 13.5% increase compared to 6.9% for its peers. As a fully integrated energy company, Chevron is positioned for sustainable production growth, notably due to its substantial operations in the Permian Basin.

The planned acquisition of Hess Corporation should strengthen Chevron’s foothold in the oil-rich area of Guyana. However, the company is also operating under the pressures of fluctuating oil prices and high valuation concerns. Weak margins in refined products led the downstream segment to its first quarterly loss in four years. Investors may want to wait for a more favorable entry point.

(You can read the full research report on Chevron here >>>)

Taylor Devices, Inc. shares have lagged compared to the Zacks Manufacturing – General Industrial sector, declining 24.8% over the past year against a 6.0% drop for the industry. The microcap, valued at $99.73 million, reported a 7% decrease in U.S. sales, which comprise 82% of its total revenues. For the first half of fiscal 2025, the total revenue reached $20.17 million, a slight drop from the previous year. Net income and operating income both fell by 3%, although SG&A expenses increased by 7% year-over-year.

Despite these challenges, Taylor Devices is well-positioned to thrive, driven by increasing global demand for seismic protection and industrial dampers. The backlog rose to $34.5 million, assuring solid revenue prospects for fiscal 2025-26. International sales experienced a 37% increase, particularly in Asia, while industrial segment sales grew by 43%, demonstrating broader acceptance of vibration control systems in various industries. Improved gross margin to 47% from 45% highlights operational efficiency, and a strong balance sheet enhances the company’s financial flexibility for expansion.

(You can read the full research report on Taylor Devices here >>>)

GSI Technology, Inc. has performed poorly in the Zacks Computer-Storage Devices sector, with stock down 34.5% compared to a sector decline of 32.1%. The microcap, valued at $68.36 million, recorded an $8.4 million loss in the first nine months of FY2025, an 11.9% revenue drop, and margin compression to 46.7%. The company faces hurdles due to weakness in SRAM sales and questions regarding customer concentration risks.

Nevertheless, GSI Technology is broadening its presence in defense AI with significant contracts from the U.S. government, including a $0.3 million Army SBIR contract and ongoing projects with the Air Force and Space Development Agency. The firm is active in growing high-performance computing and AI markets, with products like the Gemini-II and Plato chips tailored for low-power, high-speed AI tasks. Increased demand for SRAM from AI hardware is expected to bolster revenue, thanks to a major customer projected to drive FY2025 sales. Moreover, strategic asset sales have improved liquidity, providing $15.1 million in cash without incurring debt.

(You can read the full research report on GSI Technology here >>>)

Other noteworthy reports today include Pfizer Inc. (PFE), Corning Inc. (GLW), and Johnson Controls International plc.

Market Insights: Earnings Reports Reflect Strength Across Various Sectors

Mark Vickery

Senior Editor

Note: Sheraz Mian leads the Zacks Equity Research department and is a well-known expert in aggregate earnings. He is regularly referenced in both print and digital media and publishes the weekly Earnings Trends and Earnings Preview reports. To receive email notifications for new articles by Sheraz, please click here>>>

Today’s Key Insights

Apple’s Portfolio and Services Anticipated to Drive Growth (AAPL)

Meta Platforms (META) Benefits from User Growth and Instagram Success

Chevron (CVX) Experiences Production Growth from Permian Assets

Featured Reports Analysis

Pfizer (PFE) Projects Sales Growth Driven by New Product Launches

Pfizer’s non-COVID revenue rose in 2024, supported by key medications like Vyndaqel and new products from Seagen. The Zacks analyst expects this positive trend to continue into 2025.

Corning (GLW) Boosted by Strong Demand and Innovative Products

According to the Zacks analyst, the rise in AI-powered optical connectivity products and the introduction of domestically produced wafers are expected to enhance Corning’s revenue stream.

Johnson Controls (JCI) Sees Revenue Growth from HVAC & Controls Segment

The Zacks analyst notes that demand in the Building Solutions North America segment will likely boost Johnson Controls’ revenues, despite ongoing foreign exchange challenges.

Exact Sciences (EXAS) Ready to Launch New Tests Amid Cost Pressures

Impressively, Exact Sciences is set to introduce three significant tests, including the Oncodetect MRD test. Nevertheless, rising costs may impact profit margins, according to the Zacks analyst.

Murphy Oil (MUR) Maintains Production with Low-Cost Assets

The Zacks analyst highlights that Murphy Oil’s diverse portfolio enhances production efforts, while its cost-efficient operations in North America support its overall performance.

Perrigo (PRGO) Implements Cost-Saving Measures

Despite facing macroeconomic pressures like currency fluctuations and inflation, the Zacks analyst is optimistic about Perrigo’s initiatives aimed at cost reduction and margin improvement.

Signet (SIG) to Benefit from Cost Management Strategies

The Zacks analyst reports that Signet’s focus on controlling labor costs and optimizing SG&A expenses has yielded positive results, with a year-over-year decline in SG&A expenses by 4.9% to $639.2 million in Q4.

Recent Upgrades

Affirm Holdings (AFRM) Rises Due to Organic Growth and Partnerships

The Zacks analyst attributes Affirm’s revenue growth to increased card network revenue and servicing income, along with valuable partnerships and innovative products.

Commerce Bancshares (CBSH) Supported by Loan Demand and Higher Rates

Relatively higher interest rates, strong loan demand, and effective balance sheet strategies are expected to strengthen Commerce Bancshares’ financial standing, as per the Zacks analyst.

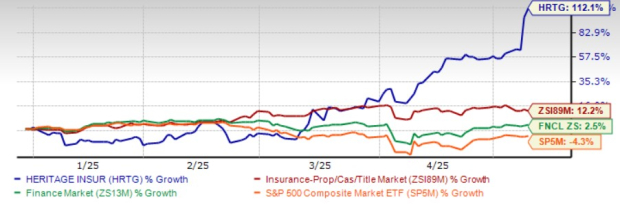

Palomar (PLMR) Experiences Growth from Solid Top Line and Capital Position

According to the Zacks analyst, Palomar’s increasing revenues from higher premiums and net investment income, as well as a strong capital position, enable effective capital deployment.

Recent Downgrades

Landstar (LSTR) Struggles with Weak Freight Market Conditions

The Zacks analyst notes that overall volume weakness stemming from decreased freight demand and supply chain disruptions is negatively affecting Landstar’s revenue.

IPG Photonics (IPGP) Faces Challenges from Diminished Market Demand

The Zacks analyst reports that muted demand in key sectors like industrial manufacturing and e-mobility, along with cautious spending, is impacting IPG Photonics’ prospects.

Dave & Buster’s (PLAY) Affected by Soft Comparisons and Economic Woes

The Zacks analyst warns that Dave & Buster’s is likely to suffer from weakened comparison metrics and disruptions due to ongoing renovations, compounded by an uncertain economic backdrop and decreased consumer spending.

Zacks Highlights Top Semiconductor Stock

Identified as only 1/9,000th the size of NVIDIA, which has risen over 800% since Zacks’ recommendation, this emerging chip stock is projected to have significant growth potential. With robust earnings growth and a widening customer base, it stands to benefit from increasing demand in Artificial Intelligence and the Internet of Things. The global semiconductor market is expected to surge from $452 billion in 2021 to $803 billion by 2028.

For more detailed insights into this stock, click here to access the report.

To stay updated with the latest insights from Zacks Investment Research, you can also download the report entitled “7 Best Stocks for the Next 30 Days” here.

Discover more with free stock analyses for:

- Apple Inc. (AAPL)

- Chevron Corporation (CVX)

- GSI Technology, Inc. (GSIT)

- Taylor Devices, Inc. (TAYD)

- Meta Platforms, Inc. (META)

This article was originally published on Zacks Investment Research (zacks.com).

Zacks Investment Research

The views and opinions expressed herein are those of the author and do not necessarily reflect those of Nasdaq, Inc.