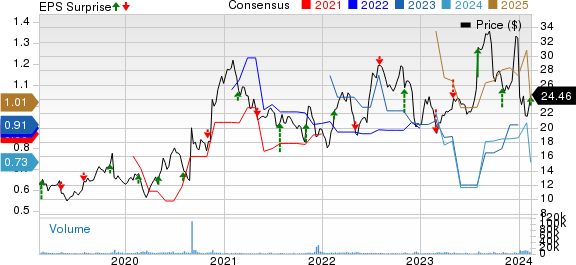

A corporate success story unfurled for Corcept Therapeutics Incorporated as it revealed fourth-quarter 2023 earnings, signaling an impressive performance that smashed through the Zacks Consensus Estimate. Reporting 28 cents per share, Corcept soared above the expected 25 cents, all enroute to a stark improvement from the 14 cents per share reported during the same period in the previous year.

Revenues also witnessed a remarkable surge, escalating by an eye-popping 31% year over year to $135.4 million. This impressive figure surpassed the Zacks Consensus Estimate of $130 million, primarily bolstered by the burgeoning product sales of Korlym, the company’s specialized Cushing’s syndrome drug.

Quarter in Detail

Delving into the nitty-gritty of the quarter, revenues from Korlym dovetailed with the estimated $135.4 million, showcasing substantial alignment with expectations. However, the company grappled with ascendant research and development expenses, which surged a whopping 48.8% year over year to reach $54.7 million. Meanwhile, selling, general, and administrative expenses ballooned approximately 11.4% year over year to $47.1 million. Operating expenses predictably surged to $103.7 million, escalating by 28.8% from the previous quarter.

Corcept’s shares underwent a tumultuous journey in the stock market, witnessing a plummet by 20% in the past six months, a stark contrast to the industry’s commendable growth of 4.3%. Targeting future prospects, the company positioned itself lucratively with cash and investments amounting to a staggering $425.4 million as of December 31, 2023, a leap from the $414.8 million reported on September 30, 2023.

2023 Results

Glancing at the overall performance for 2023, revenues demonstrated a robust upswing, escalating by 20% from the 2022 level and in unison with the Zacks Consensus Estimate. Earnings per share also leaped to 94 cents, a significant upturn from the 87 cents in 2022. The bottom line outperformed the Zacks Consensus Estimate of 92 cents, underlying its stellar performance.

2024 Guidance

Looking ahead to 2024, Corcept reaffirmed its guidance, anticipating total revenues in the wide range of $600-630 million. Although the Zacks Consensus Estimate for revenues is tethered at $609 million, the company’s commitment to the pursuit of excellence remains unwavering. In January, Corcept trumpeted a program to repurchase up to $200 million of its common stock, funded using cash and investments.

Pipeline Updates

Striding forward, Corcept’s lead pipeline candidate, relacorilant, is navigating phase III of the GRACE study, a pivotal step toward treating Cushing’s syndrome. The company anticipates submitting a new drug application in the second quarter of 2024, a promising development that signifies their unwavering commitment to innovation and patient care.

Meanwhile, the phase III GRADIENT study evaluating relacorilant for patients with Cushing’s syndrome caused by adrenal adenoma is presently enrolling patients, with results anticipated in the second half of the year. Corcept also expects data from the phase Ib study, assessing relacorilant in combination with Merck’s blockbuster PD-1 checkpoint inhibitor, Keytruda (pembrolizumab), for treating patients with adrenal cancer with cortisol excess, in mid-2024.

To read the full article and explore more insights, visit Zacks.com

For all things investment-oriented, engage with Zacks Investment Research