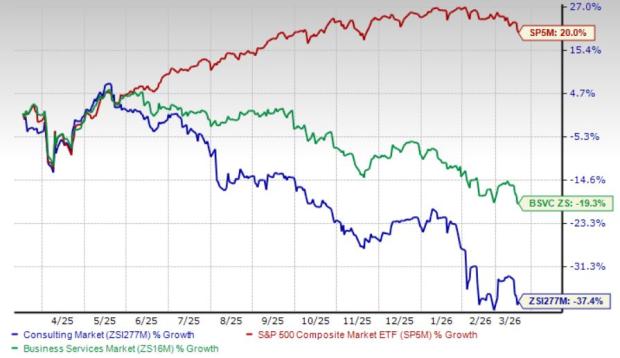

Devon Energy Stock Outperforms Industry and Sector Amid Challenges

Devon Energy Corporation’s DVN shares have seen a year-to-date gain of 1.6%. This performance stands in stark contrast to the Zacks Oil & Gas Exploration and Production – United States industry, which has declined by 22.8%, and the broader Zacks Oil and Energy sector, down 1.3% for the same period.

While the year-to-date progress is encouraging, examining the past year’s performance provides a fuller perspective. Over the last year, DVN’s stock has dropped by 32.7%, indicating a gradual recovery trend. In comparison, another sector competitor, Occidental Petroleum Corporation (OXY), has also faced challenges with a 31.7% share price decline during the same timeframe.

Price Performance Overview

Image Source: Zacks Investment Research

Should you consider buying DVN stock based on its positive price movements? To answer this, it is essential to evaluate the underlying factors that may indicate whether this is a good time to add this stock to your portfolio.

Key Factors Behind DVN’s Stable Performance

Devon Energy benefits from a balanced mix of commodities, including oil, natural gas, and natural gas liquids. The company aims to enhance its portfolio with quality resources. In 2024, exploration activities have resulted in a production replacement rate of 154%, securing the company’s ability to maintain production levels into the future through significant reserve additions.

DVN’s diversified portfolio of high-margin oil and gas assets presents strong growth potential. The company is actively enhancing its asset base through strategic acquisitions.

For instance, the acquisition of Grayson Mill Energy’s Williston Basin assets expanded DVN’s net acreage significantly, from 123,000 to 430,000 acres. This deal is projected to increase production from 50,000 to 150,000 barrels of oil equivalent per day (Boe/d). The newly acquired assets have quickly begun contributing to overall output, expected to bolster long-term growth.

Additionally, Devon Energy’s low-cost operating model supports profitability. By selling higher-cost assets and introducing more efficient production methods, the company is strengthening its cost structure. Continuous efforts to lower drilling and completion costs, along with workforce streamlining, are enhancing Devon Energy’s margins.

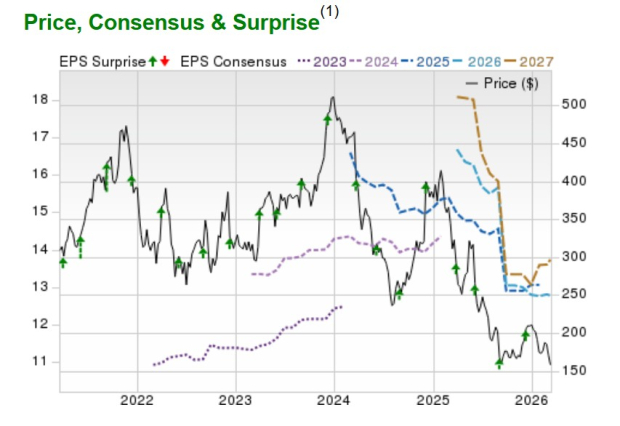

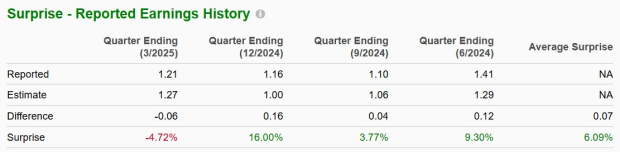

Devon Energy’s Earnings Surprise Record

In general, DVN has demonstrated strong earnings, thanks to solid financial performance across its multi-basin assets. However, the company missed expectations in its most recent quarter, with a mixed record of surpassing expectations in three out of the last four quarters, averaging a 6.09% earnings surprise.

Image Source: Zacks Investment Research

In contrast, Occidental Petroleum has reported a positive earnings surprise in each of the last four quarters, achieving an average positive surprise of 24.34%.

Devon’s Returns Compared to the Industry

Devon Energy’s return on invested capital (ROIC) has outperformed the industry average over the past 12 months. DVN’s ROIC was 8.71%, whereas the industry’s average stood at 7.33%. This metric indicates the company’s effectiveness in generating returns on its investments, serving as a key measure of profitability and operational performance.

Image Source: Zacks Investment Research

In comparison, Cheniere Energy (LNG), another industry player, boasts a superior ROIC of 9.26%.

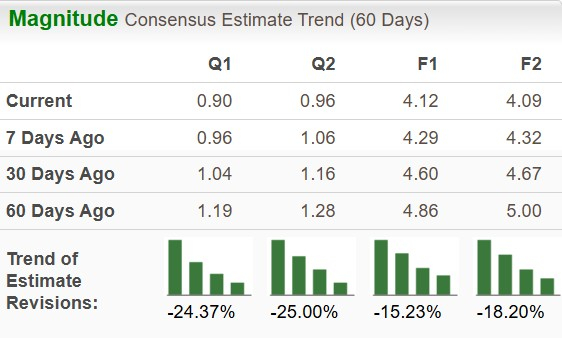

Declining Earnings Estimates for DVN

Recently, the Zacks Consensus Estimate for DVN’s earnings per share has decreased by 15.23% and 18.2% for 2025 and 2026, respectively, over the past two months.

Image Source: Zacks Investment Research

Meanwhile, Cheniere Energy’s 2025 earnings estimate shows a decline of 4.74%, whereas 2026 estimates have risen by 1.36% in the same timeframe.

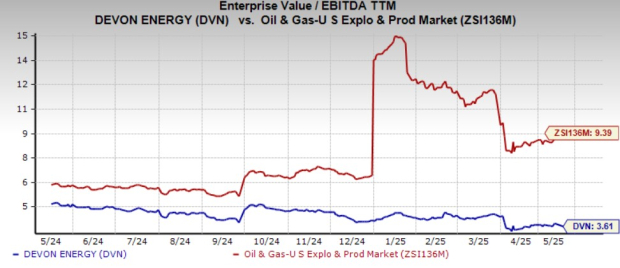

DVN Shares Valuation Outlook

Currently, Devon Energy’s shares appear relatively inexpensive, with a trailing 12-month Enterprise Value/Earnings before Interest Tax Depreciation and Amortization (EV/EBITDA TTM) of 3.61X compared to the industry average of 9.39X.

Image Source: Zacks Investment Research

Conclusion

Devon Energy’s strengths lie in its multi-basin assets and balanced exposure to oil, natural gas, and NGL production. The company’s better return compared to the industry, combined with its attractive valuation, presents noteworthy qualities. However, the decline in earnings estimates may temper some of these positive attributes at this time.

Investors currently holding this Zacks Rank #3 (Hold) stock might consider retaining it, while new investors may want to wait for a more favorable entry point.