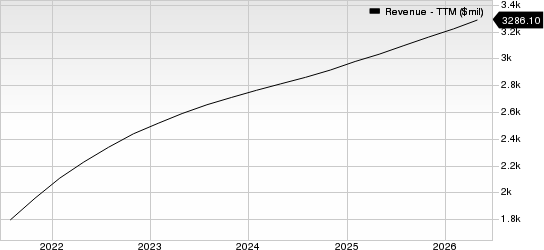

Docusign, Inc. (DOCU) has seen a rise in customer demand for its eSignature solutions, experiencing consistent growth in its customer base from 1.3 million in fiscal 2023 to an expected 1.8 million in fiscal 2026. The company is capitalizing on its subscription model, which has driven revenue growth, with its international revenues growing from 26% of total revenues in fiscal 2024 to 29% in fiscal 2026.

Despite this growth, DOCU faces challenges such as a low current ratio of 0.73, significantly below the industry average of 1.92, indicating liquidity issues. Additionally, its pricing strategy is under pressure from competitors, which may affect profitability. The company does not offer dividends, limiting its attractiveness to income-focused investors.

DOCU continues to invest in partnerships, notably with Salesforce and Microsoft, to enhance its product offerings and expand market reach. The integration of eSignature with Microsoft Teams, for example, aims to significantly increase client accessibility and product sales.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.