BlackBerry, once a titan in the mobile device industry, has seen its stock plummet by 50% since pivoting from smartphones to software solutions in late 2016. Despite improvements in revenue and earnings in fiscal Q4 of 2024, the stock is down 12.4% year-to-date, lagging significantly behind broader market indices primed for all-time highs.

With IoT sales hitting record highs, BlackBerry boasts a gross margin of 85%, overshadowing its overall margin of 75%. Cybersecurity sales, though showing a 5% growth, are dwarfed by competitors like CrowdStrike, raising questions about market share. Adjusted losses are projected for fiscal 2025, accompanied by an expected sales dip to $600.9 million in the coming year.

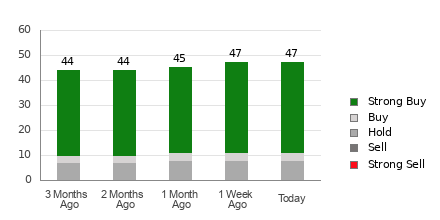

Optimistic Analysts and Target Price

Despite these challenges, analysts remain cautiously optimistic, maintaining a “hold” rating on BlackBerry stock. With an average target price of $3.49, there exists a 12% upside potential from current levels, providing a glimmer of hope for investors eying a turnaround.

In light of these considerations, it appears that less risky investment avenues may offer more promising returns than the tumultuous path of BlackBerry stock.

On the date of publication, Aditya Raghunath did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.