Unsettling News Regarding Spirit AeroSystems

Once more, Spirit AeroSystems (NYSE:SPR) finds itself entangled in a significant quality concern involving the Boeing 737 series. An Alaska Airlines (ALK) 737 Max-9 experienced a door detachment, marking another unsettling incident.

Surprisingly, the situation did not result in casualties. However, the recent history of erroneous occurrences has put a dent in the reputation of the aviation industry. My previous article projected a bullish outlook for Spirit AeroSystems, but the recent turn of events has forced me to reassess my stance.

Since my last assessment in October, the stock has enjoyed a hearty rally, outperforming the S&P 500 by a substantial margin. However, the recent pre-market plunge of 18% has brought this surge to an abrupt halt. In this article, I intend to delve into the ramifications of the unfortunate incident, the company’s strategies for improvement, and the associated risk and rewards.

An Additional Setback for Spirit and Boeing

On a recent Friday, an Alaska Air 737 Max-9 was compelled to make an emergency landing after a door malfunction led to a rapid loss of cabin pressure. Although the passengers escaped unharmed, the incident has raised valid concerns over the safety of Boeing’s 737 Max series.

Following a similar pattern from the past, Boeing’s 737 Max model is once again under scrutiny after being emphatically endorsed as the safest aircraft worldwide. Despite the Federal Aviation Administration’s affirmation of its safety, the recent episode involving Alaska Airlines has prompted temporary grounding and inspections of specific Boeing 737 Max-9 aircraft.

Regrettably, the incident has sparked doubts about the integrity of the plane’s design and manufacturing, amplifying the existing production challenges and regulatory hitches for both Boeing and Spirit AeroSystems.

Even more disconcerting, the Alaska Air flight involved a recently delivered Boeing Max variant in October and has 19 planes on order. Consequently, the occurrence has reignited apprehensions about the aircraft’s structural soundness.

Moreover, the incident has triggered speculations regarding the future safety of the Boeing 737 Max series, with China – a major growth market for commercial aviation – contemplating a response that could substantially affect Boeing’s orders.

Impact on Ongoing Recovery

Although the extent of the impact is yet to unfold, it is expected that the recent incident will disrupt the progress Spirit AeroSystems had been striving to accomplish. The aftermath will likely necessitate additional endeavors for enhancing and ensuring the safety of the remaining Max-9 models.

In my October article, I alluded to the potential for significant growth for SPR if it could successfully address its operational issues and streamline its supply chains. However, the recent turn of events has derailed this optimistic outlook.

[…] if SPR can effectively address its operational issues and streamline its supply chains, it may see significant growth, potentially doubling in value over the next four to five years.

In November, the company’s quarterly earnings revealed improving demand in the industry, with an unprecedented surge in the aerospace sector and a substantial $42 billion backlog. Additionally, the company solidified ties with Boeing through a memorandum of agreement, resulting in a significant reversal of forward loss and a higher price on the 787 program.

Spirit AeroSystems Faces Turbulence Following Recent Setbacks

In the current deal-making ecosystem, the aerospace company Spirit AeroSystems Holdings, Inc. has been presented with a Material Order Agreement (MOA) by a parachuting conglomerate, Boeing. The lifeline includes a range of reciprocal obligations and commitments including a release of claims and liabilities, funding for tooling and capital, and extended repayment dates on customer financing.

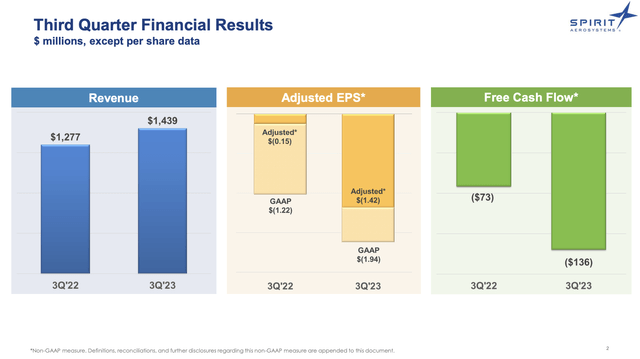

The agreement seeks to mend the chinks in Spirit’s armor following a testing period where the company grappled with a series of production mishaps and financial hiccups. Although the company’s third-quarter report saw a glimmer of hope, with revenues reaching $1.4 billion, marking a 13% increase from the previous period, the road to recovery now appears bumpier than ever.

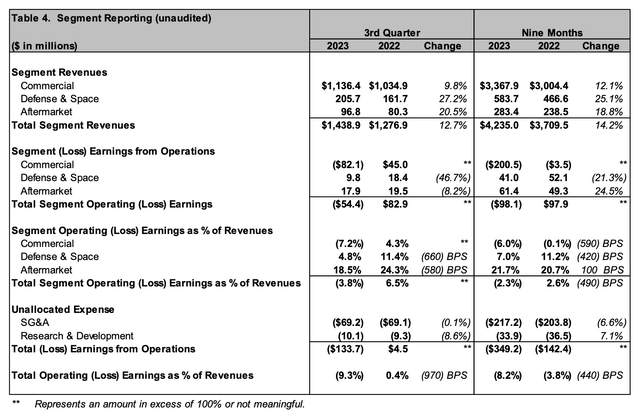

- The commercial segment revenue witnessed a 10% upswing in the quarter, propelled by enhanced production volumes. However, the operating margin plummeted to negative 7%, primarily attributed to unfavorable changes in estimates and excess capacity costs.

- The Defense and Space segment saw a revenue surge of 27%, reaching $206 million. However, the operating margin dropped to 5% due to upward revisions in cost estimates. A further blow came from forward losses of $15 million linked to the Sikorsky CH-53K program.

- Aftermarket revenues experienced a robust climb to $97 million, up by 21% from Q3 2022, largely driven by a spike in spare parts sales. Nonetheless, the operating margin for the quarter nosedived to 19%, sliding from the 24% reported during the same period in 2022, primarily due to sales and model mix.

Regrettably, Spirit’s delivery operations were adversely affected by various disruptions, including the IAM work stoppage and the 737 aft pressure bulkhead issue, resulting in a negative $1.94 in earnings per share, a negative 9% operating margin, and forward losses totaling $101 million.

The company is currently grappling with the aftermath of an issue where it mistakenly drilled holes in 737 fuselages, adding to its list of woes as it struggles to regain its footing in the market.

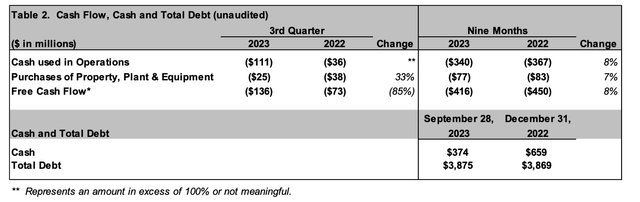

Consequently, the company incurred a free cash flow usage of $136 million for the quarter, primarily due to working capital issues and operational disruptions. It foresees a full-year free cash flow in the range of negative $275 million to negative $325 million, intensifying the financial strain it faces.

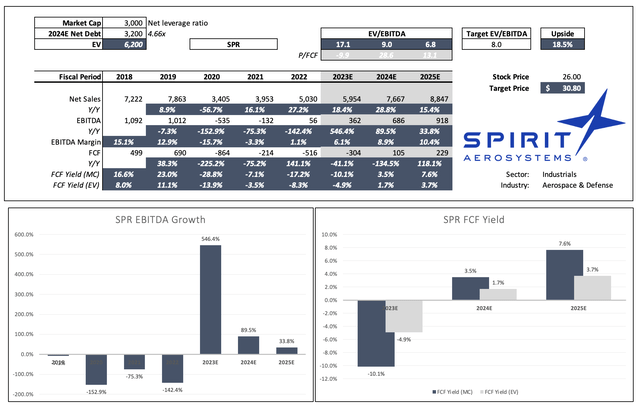

As the quarter came to a close, Spirit found itself holding $374 million in cash but also staring down $3.9 million in debt. With an expected net debt of $3.3 billion, resulting in a concerning 9.0x net leverage ratio, the company is navigating treacherous financial waters. It attempts to assuage the fears of stakeholders by envisioning a net debt ratio decline to 4.7x EBITDA in 2024, driven by projected robust performance.

Aligning with the company’s efforts, addressing $1.2 billion in debt maturities in 2025 has been labeled as a near-term priority. However, the margin for error in 2024 seems slim, reflecting the prevailing uncertainty and risk in the company’s trajectory.

During the Q&A session of its earnings call, Spirit underscored the progress in both the 737 and 787 programs. Specifically, the strategic focus on attaining positive free cash flow and stabilizing program performance within the 737 program was highlighted, with plans to increase production rates aiming for the 50s in 2025.

The company accentuated Boeing’s confidence in meeting demands in 2024 and managing the intricacies of 737 production, signifying an optimistic outlook for the program. Despite an air of positivity, the lingering impact of past and potential future challenges on the 737 program is evident, suggesting that the path to recovery remains clouded with uncertainty.

Rough Valuation Waters Ahead

The valuation landscape for Spirit AeroSystems has become more complex for two chief reasons:

- Amidst the pre-market trading, the stock witnessed an 18% downturn, casting a shadow on its valuation. The ensuing market hours are expected to be tumultuous, characterized by heightened volatility.

- The financial impact of the new incident has not yet been factored into the financial metrics, hinting at a prolonged period of uncertainty that could exert further influence on valuations.

Based on an 18% lower market cap, the stock is currently trading at 6.8x 2025E EBITDA. A target of 8.0x EBITDA would imply roughly 20% upside from the recent valuation, setting the stage for potential recovery.

This estimation equates to a price target of approximately $31, aligning with the ongoing consensus price target. Nevertheless, looming uncertainties coupled with potential cost escalations could spell trouble for free cash flow and borrowing costs, affecting the company’s long-term outlook and refinancing prospects.

As a result, the bullish sentiment toward the stock has waned, with the company’s recovery potential appearing less robust than previously anticipated.

In hindsight, Spirit AeroSystems was once viewed as a recovery prospect in the industry. However, with the recent turn of events, the outlook has dampened, prompting a shift in focus towards alternative investment opportunities among industry peers such as RTX Corp. (RTX), General Electric (GE), HEICO (HEI), and TransDigm (TDG).

Navigating the uncertainty ahead, vigilance will be paramount in identifying potential investment prospects in the future.

Closing Sentiments

The recent incident involving Alaska Airlines’ 737 MAX-9 has unleashed a storm of adversity for Spirit AeroSystems and its partner, Boeing. Although no lives were lost, the event has reignited concerns regarding the safety of the Boeing 737 Max series, potentially rattling the global demand chain.

Arriving at a precarious juncture for SPR, the company now finds itself contending with a fresh set of challenges that threaten to undermine its path to recovery. The incident is projected to disrupt the positive momentum the company had strived to regain, perpetuating the era of uncertainty looming over its financial health and market outlook.

As a result, the once splendid prospects for Spirit AeroSystems have dimmed, leading to a shift in sentiment from optimistic to cautious, signaling the need to explore alternative investment avenues in response to the prevailing challenges.