The Estee Lauder Companies Inc. EL exhibited a volatile stock trajectory in recent months, driven by weak consumer sentiment amid high inflation and rising interest rates. The company is also grappling with issues such as market instability in mainland China and Asia travel retail, lower conversion rates, and negative foreign currency impacts.

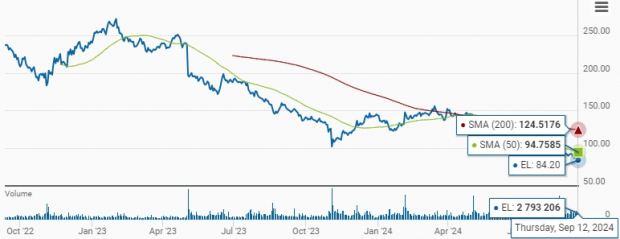

As a result, shares of this New York-based provider of skincare, makeup, fragrance and hair care products have plunged 42.4% year to date compared with a 37.7% drop in the broader industry. In contrast, the Consumer Staple sector and the S&P 500 have posted increases of 9.4% and 16.3%, respectively, during the same period. Closing the trading session at $84.20 on Thursday, shares of EL stand close to its recently reached 52-week low of $82.39.

Image Source: Zacks Investment Research

EL is trading below its 50 and 200-day moving averages, indicating a bearish outlook and challenges in sustaining the recent performance levels.

EL Stock Trades Below 50 and 200-Day Moving Average

Image Source: Zacks Investment Research

Decoding Challenges Faced by EL

In the fiscal 2024, The Estee Lauder Companies faced significant challenges in the Asia-Pacific region, particularly in mainland China, due to a broader slowdown in the prestige beauty sector. Sales in the Asia-Pacific region fell 7% to $1,205 million during the fiscal fourth quarter. The downtick was largely caused by weakness in mainland China. Consumer confidence remained low and cautious spending behavior contributed to a decline in prestige beauty retail sales, which worsened from mid-single digits in the third quarter to low-double digits. The Asia travel retail market also struggled, with sales in Hainan plunging more than 40% in the fiscal fourth quarter. Weaker consumer sentiment, smaller basket sizes and a shift toward spending on experiences played a key role in these declines. Looking ahead to fiscal year 2025, the recovery in China and Asia travel retail is expected to be slow, which might limit sales growth and profitability in these key markets.

Another concerning point is the contraction in adjusted operating margins, which contracted 120 basis points to 10.2% in the fiscal 2024. While there was a modest recovery in the later part of the fiscal 2024, the outlook for fiscal 2025 indicates a slower-than-expected pace of margin expansion. This delay is partially attributed to continued pressure from high-margin categories like skin care, which are still facing declines in sales.

The company is losing market share in channels that are growing more slowly, such as traditional retail, despite some gains in high-growth platforms like Amazon AMZN. However, these gains are not enough to offset losses in brick-and-mortar stores, particularly in North America, where competition is fierce.

The Estee Lauder Companies faces significant financial pressure due to unfavorable currency rates. Currency fluctuations, particularly in regions like Israel and the Middle East, compounded by business disruptions, further impacted the company’s profitability in the fiscal 2024. These currency headwinds are expected to continue affecting earnings, potentially reducing earnings per share (EPS) by approximately 3 cents in the fiscal 2025.

What to Expect From The Estee Lauder Companies in FY25?

The company continues to face a challenging macroeconomic environment, with ongoing volatility in the global prestige beauty market, especially in mainland China and Asia travel retail. For fiscal year 2025, management expects a more modest performance compared to industry averages, primarily due to its strong presence in these regions. Weak consumer sentiment and changing traveler behavior, with more spending on experiences over products, are impacting Asia travel retail. Additionally, risks such as retailer destocking and intense competition, particularly in North America, are further complicating the company’s outlook.

In the first quarter of fiscal 2025, the company anticipates continued pressure from these challenges, projecting a 3-5% year-over-year decline in reported and organic net sales. Adjusted EPS are expected to fall sharply, ranging between 1 and 9 cents and suggesting a decline of 17-89% on a constant-currency basis.

Analysts Downgrade EL’s Earnings Estimates

EL appears to be in a troubled spot. The Zacks Consensus Estimate for the current and next fiscal year EPS has moved downward by 2.9% and 4.3% to $2.97 and $4.03, respectively, in the past seven days. This downward adjustment reflects a negative sentiment among analysts and suggests potential challenges in achieving projected profitability.

Image Source: Zacks Investment Research

EL’s Valuation Premium Raises Questions

The Estee Lauder Companies valuation remains a point of contention. Despite the pullback in the stock price, EL is trading at a premium relative to industry peers like Coty Inc. COTY and Inter Parfums, Inc. IPAR, which seems increasingly difficult to justify. EL is currently trading at a forward 12-month P/E of 25.99, higher than the industry’s 21.89. This valuation discrepancy indicates that while investors have high expectations for the company’s future growth, the stock’s current performance and the broader market challenges could pose risks.

Can Growth Strategies Turn the Tide?

Despite several challenges, The Estee Lauder Companies is making significant strides with its Profit Recovery and Growth Plan (PRGP). This initiative focuses on three core areas — accelerating margin expansion, targeted growth investments, and simplifying processes for greater agility. For the fiscal 2025, the PRGP is expected to deliver substantial benefits, with around 80% of gains improving gross profit through optimized pricing, reduced discounts and enhanced precision marketing. The remaining 20% aims to cut operating expenses by streamlining operations and expanding shared services. These efforts are projected to generate $1.1-$1.4 billion in net savings by the fiscal 2026.

The company is also leveraging its strengths in high-growth areas, including its global prestige skin care portfolio and luxury fragrance brands such as Jo Malone London, TOM FORD and Le Labo. Its focus on digital transformation is another key growth driver, with strong online sales growth across nearly 50 markets. Digital initiatives, combined with precision marketing using AI and consumer profiles, position the company for sustained growth and future market leadership.

While EL is resorting to restructuring, the fiscal 2025 forecast reveals more conservative sales growth and profitability improvements than originally anticipated. This suggests that the company’s recovery will take longer than planned, leaving investors wary of future profitability in the near term.

What’s Next for Investors?

The Estee Lauder Companies is facing significant challenges, including weak consumer sentiment, declining sales in key markets like China, and currency headwinds. Its reliance on Asia travel retail and luxury beauty has led to pressure on margins and overall profitability. The stock is trading below key moving averages, signaling a bearish trend. While the profit recovery plan aims to improve margins and streamline operations, the road to recovery might be longer than anticipated. With a lofty valuation and analysts downgrading earnings estimates, investors should approach EL stock with caution. EL currently carries a Zacks Rank #5 (Strong Sell).

You can see the complete list of today’s Zacks #1 (Strong Buy) Rank stocks here.

Zacks Names #1 Semiconductor Stock

It’s only 1/9,000th the size of NVIDIA which skyrocketed more than +800% since we recommended it. NVIDIA is still strong, but our new top chip stock has much more room to boom.

With strong earnings growth and an expanding customer base, it’s positioned to feed the rampant demand for Artificial Intelligence, Machine Learning, and Internet of Things. Global semiconductor manufacturing is projected to explode from $452 billion in 2021 to $803 billion by 2028.

See This Stock Now for Free >>

Want the latest recommendations from Zacks Investment Research? Today, you can download 5 Stocks Set to Double. Click to get this free report

Amazon.com, Inc. (AMZN) : Free Stock Analysis Report

The Estee Lauder Companies Inc. (EL) : Free Stock Analysis Report

Inter Parfums, Inc. (IPAR) : Free Stock Analysis Report

Coty (COTY) : Free Stock Analysis Report

To read this article on Zacks.com click here.

Zacks Investment Research

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.