If you are an income-focused investor, you have likely come across energy midstream companies (including master limited partnerships (“MLPs”)). These specialized companies generally transport oil and gas through pipelines, and they can offer some of the biggest and steadiest income payments in the market. However, before you invest in any of these companies, you need to understand the unique nuances and tax risks of the MLP structure, particularly with regards to account types (i.e. should you hold MLPs in your IRA, your taxable account, or neither). In this report, we share data on the top 10 midstream companies (including the top 5 MLPs), review Energy Transfer (an MLP) in particular (including its business, big yield, valuation and risks), and then conclude with our strong opinion on if (and where) your should even consider including Energy Transfer in your prudently-diversified big-yield investment portfolio.

![]()

![]()

Energy Transfer Overview

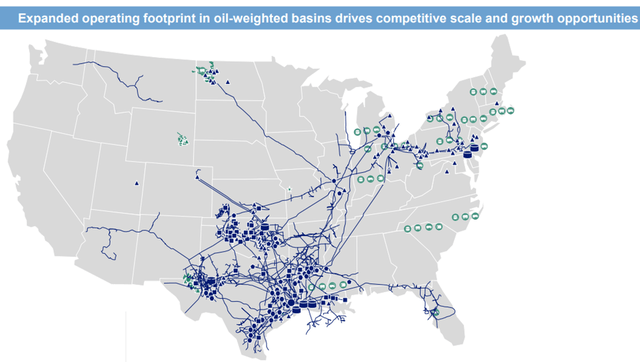

Energy Transfer is one of the largest and most diversified midstream energy companies in North America. It has more than 125,000 miles of pipelines and associated energy infrastructure in 44 states. It transports much of the oil and gas products that make modern life possible (including everything from the clothes you wear and the food you eat to the transportation you use).

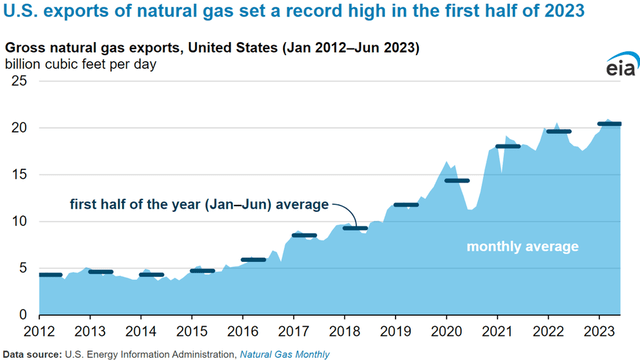

The business is particularly attractive (especially as compared to some other midstream companies) because it is diversified across multiple geographies and commodities, thereby giving it access to big customers. Further still, Energy Transfer is well positioned to benefit from growing natural gas exports.

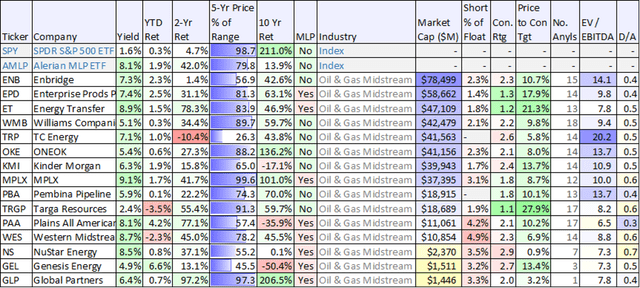

Top 10 Midstream Companies

Before going deeper into Energy Transfer, here is a quick look (for comparison and perspective) at some data points for a variety of the largest midstream companies, sorted by market cap.

(ENB) (EPD) (ET) (WMB) (TRP) (OKE) (KMI) (MPLX) (TRGP) (PBA) (WES) (PAA)

As you can see in, Energy Transfer is one of the largest midstream companies, and it has one of the lower valuations (arguably quite attractive, as we will discuss later in this report). Wall Street analysts also rate it a strong buy (1.0 = strong buy, 5.0 = strong sell).

High Distribution Yield

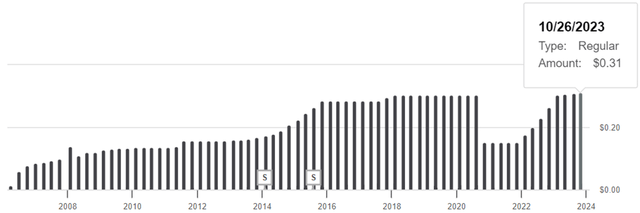

One of the main reasons many investors are attracted to Energy Transfer is its substantial distribution yield (currently ~9.0%). The company targets a 3% to 5% annual distribution growth rate, and recently announced another increase in the distribution to $0.3125 per unit.

For the most recently reported quarter, total distributable cash flow was $2.0 billion, and the company had ~$1.0B in excess cash flows after distributions. Share (“unit”) repurchases are also an option, although the company has been more recently working on getting its leverage (debt) level down to the 4.0 to 4.5 target range. And on that front, the company has been making positive progress (in August, Energy Transfer’s senior unsecured credit rating was upgraded by S&P to BBB with a stable outlook).

Preferred Unit Distributions

Also important to mention, Energy Transfer (or its subsidiary, Energy Transfer Operating, L.P.) has issued multiple series of preferred units, but they will be redeemed soon (as per this press release). Specifically, series C, D and E preferred units (listed on the NYSE under ticker symbols (ET.PR.C) (ET.PR.D) (ET.PR.E)) will be redeemed following the issuance of $3 billion of senior notes and $800 million of junior subordinated notes. We view this as a positive for the company (but not necessarily for the holders of the preferreds) considering the transactions will essentially allow the company to refinance outstanding debt (i.e. the preferred shares) at a lower rate.

DRIP Plan

Also noteworthy, Energy Transfer offers a Distribution Reinvestment Plan, which can be an outstanding way for owners to reinvest their distributions. The plan allows owners to purchase additional common units by reinvesting all or a portion of the quarterly cash distributions paid. Importantly, additional units purchased through the plan will be sold at a discount ranging from 0% to 5% (unfortunately it’s currently set at 0.0%) but investors do not pay any service fees, brokerage trading fees or other charges (this is a good thing).

Valuation

From a valuation standpoint, Energy Transfer appears very attractive. Specifically, the company currently has one of the lowest EV/EBITDA valuations (see our earlier midstream data table) and one of the best Wall Street analyst ratings (again, see our earlier table, it’s rated “1.2” or “strong buy”). However, the units have been a bit chronically undervalued over time. Possible reasons for the low valuation include the risks of converting from an MLP to a C-Corp (more on this later) and the risk of more pricey acquisitions (the company has a history of this). However, the upside of the low valuation is that the distribution yield is quite high (attractive).

Energy Transfer: Navigating the Perils of MLP Investments

Master Limited Partnership Structure: A Blessing or a Curse?

Energy Transfer, a publicly traded master limited partnership (MLP), offers investors the promise of cash distributions, but with a twist. The tax implications are a crucial nuance. Instead of a traditional 1099, investors receive a K-1 statement, and the company’s income, gains, losses, deductions, and credits flow through to unitholders, requiring them to report allocated amounts on their individual tax returns. This structure presents unique challenges for investors.

MLPs and Retirement Accounts: A Complex Relationship

While it is technically possible to hold an MLP in a retirement account, such as a Traditional or Roth IRA or a 401K, there are significant tax considerations to bear in mind. The tax benefits of MLPs are diminished in retirement accounts where income is already tax-deferred, and holding an MLP in such an account can result in unforeseen income taxes due to the concept of “Unrelated Business Tax income” (“UBTI”).

Potential C-Corp Conversion: A Looming Threat

Energy Transfer’s potential shift from an MLP to a C-Corp structure is a risk factor that investors cannot afford to overlook. Such a conversion often triggers taxable sales for unit holders, leading to substantial tax obligations on their adjusted cost basis. The possibility of this conversion presents a substantial risk, particularly for long-term MLP unit holders.

Environmental Risks: Navigating Regulatory Pressures

Energy Transfer, as a major player in the energy sector, grapples with ongoing environmental and regulatory challenges. Legal battles, such as the prolonged dispute concerning its Dakota Access pipeline, underscore the significant regulatory pressures and risks faced by the company. These factors contribute to the complexity of investing in Energy Transfer.

Conclusion: Evaluating the Investment Landscape

Despite the myriad risks and complexities surrounding MLP investments, Energy Transfer remains an enticing prospect for investors seeking substantial cash flows and high yields. However, potential tax impacts, the challenges of MLP ownership, and the uncertainties related to a conversion to a C-Corporation warrant careful consideration. Ultimately, the decision to invest in Energy Transfer hinges on individual circumstances and risk tolerance, and it must form part of a well-diversified high-income portfolio.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.