Amazon’s Stock Performance and Earnings Outlook: A Comprehensive Review

Amazon (AMZN) has recently caught significant attention on Zacks.com. With the stock’s recent performance under scrutiny, it’s worth examining critical data that could influence its future trajectory.

In the past month, Amazon’s shares have declined by -9.2%, while the Zacks S&P 500 composite index has decreased by -6.2%. By comparison, the Zacks Internet – Commerce industry, which includes Amazon, has seen a loss of 7.1% during this time. The pressing question remains: What are the prospects for the Stock moving forward?

Impact of Earnings Estimates Revisions

While media speculation or rumors can briefly affect a company’s stock price, it’s the fundamental factors that ultimately drive long-term investment decisions. At Zacks, we prioritize changes in earnings estimates when evaluating a company’s future potential. The present value of expected earnings is crucial in determining a stock’s fair value.

We analyze how sell-side analysts are updating their earnings estimates to reflect shifting business conditions. If earnings estimates rise, it usually indicates an increase in fair value, catching the interest of investors and potentially elevating the stock price. This correlation between earnings estimate revisions and stock price movements is well-documented.

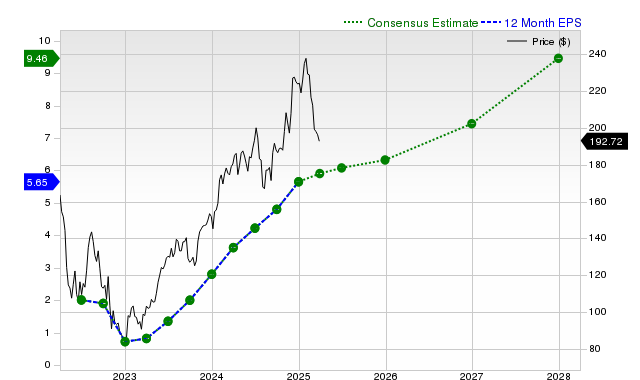

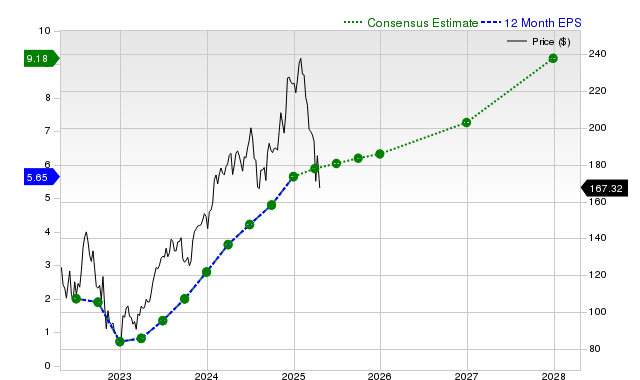

For the current quarter, Amazon’s expected earnings are projected at $1.38 per share, reflecting a year-over-year increase of +22.1%. In the last 30 days, the Zacks Consensus Estimate has increased by +0.4%.

The consensus earnings estimate for the current fiscal year stands at $6.32, indicating a +14.3% year-over-year growth, with a slight adjustment of +0.2% over the past month.

Looking ahead to the next fiscal year, analysts predict earnings of $7.44 per share, marking a +17.7% change from last year. This estimate has remained steady over the last month.

Our proprietary stock rating tool, the Zacks Rank, employs earnings estimate revisions to provide clearer insights into price direction. Currently, Amazon holds a Zacks Rank #3 (Hold), reflecting the consensus estimate changes and other key earnings factors.

The chart below depicts the evolution of Amazon’s forward 12-month consensus EPS estimate:

12-Month EPS

Revenue Growth Projections

Earnings growth can indicate financial health, but a company also needs to increase its revenues. Sustained earnings growth typically requires a concurrent rise in revenue. Therefore, understanding potential revenue growth is essential.

For the current quarter, the consensus sales estimate for Amazon is $154.82 billion, anticipating a +8% year-over-year growth. Over the next two fiscal years, revenue estimates of $697.68 billion and $769.2 billion predict increases of +9.4% and +10.3%, respectively.

Recent Financial Results and Performance Trajectory

Amazon’s last reported quarter showed revenues of $187.79 billion, which is a +10.5% increase from the previous year. The EPS for this period was $1.86, compared to $1.01 one year prior.

Amazon’s reported revenues surpassed the Zacks Consensus Estimate of $187.28 billion, resulting in a revenue surprise of +0.28%. The EPS surprise was a healthy +22.37%.

The company has consistently exceeded consensus EPS estimates in the last four quarters, and it has achieved revenue estimates above consensus three times during this span.

Valuation Considerations

No investment decision is complete without evaluating a stock’s valuation. Understanding whether Amazon’s stock price accurately reflects its intrinsic business value and growth potential is critical for future performance predictions.

To assess valuation, analyzing multiples like price-to-earnings (P/E), price-to-sales (P/S), and price-to-cash flow (P/CF) relative to historical figures helps determine if the stock is fairly valued. Comparison against peers provides additional context regarding the stock price’s reasonableness.

According to the Zacks Value Style Score, which uses various traditional and unconventional valuation metrics to grade stocks, Amazon receives a grade of D. This indicates the stock is trading at a premium compared to its peers. For detailed valuation metric values, click here.

Conclusion

The information outlined above, along with additional insights from Zacks.com, may aid in evaluating the market consensus around Amazon. Presently, its Zacks Rank #3 suggests that the stock may perform in line with overall market trends in the near future.

Zacks Identifies Top Semiconductor Stock

In a market where valuations are rapidly changing, a semiconductor stock stands out. Though it is only 1/9,000th the size of NVIDIA, which has surged over +800% since its recommendation, this new chip stock shows promise for substantial growth.

With its robust earnings growth and expanding customer base, this semiconductor firm is well-positioned to capitalize on the booming demand across sectors such as Artificial Intelligence, Machine Learning, and the Internet of Things. Global semiconductor manufacturing is forecasted to increase from $452 billion in 2021 to $803 billion by 2028.

Find out more about this promising stock for free.>>

For the latest recommendations from Zacks Investment Research, you can download the “7 Best Stocks for the Next 30 Days.” Click here to get this free report.

Amazon.com, Inc. (AMZN): Free stock analysis report available here.

This article originally published on Zacks Investment Research (zacks.com).

Zacks Investment Research

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Nasdaq, Inc.