Alibaba’s Stock Performance: Analyzing Earnings and Revenue Trends

Alibaba (BABA) continues to attract attention among investors. Given its recent performance, reviewing factors that may impact the near-term trajectory of this stock is prudent.

In the past month, Alibaba shares have decreased by -12.1%, compared to a -4.8% decline in the Zacks S&P 500 composite. Within the Zacks Internet – Commerce industry, which includes Alibaba, the average loss has been 7.8%. This raises a key question: What is the potential short-term direction for the stock?

Media reports and rumors can create short-term price fluctuations, but long-term investment decisions hinge on fundamental factors. Understanding earnings estimates is crucial, as they play a significant role in determining a company’s fair value.

Changes in Earnings Estimates

At Zacks, we emphasize earnings projections when evaluating a company’s outlook. The future income stream primarily dictates the intrinsic value of its stock.

We monitor how analysts adjust their earnings forecasts based on recent business developments. An increase in earnings estimates typically signals a higher fair value for the stock, attracting investor interest and driving prices up. Research consistently demonstrates a strong link between earnings estimate revisions and near-term stock price movements.

For the current quarter, Alibaba anticipates earnings of $1.48 per share, reflecting a year-over-year increase of +5.7%. Notably, the Zacks Consensus Estimate has remained stable over the past 30 days.

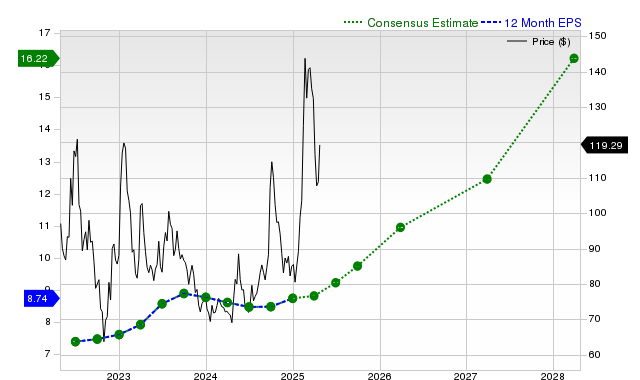

Looking at the fiscal year, the consensus earnings estimate stands at $8.92, indicating a +3.5% rise compared to last year. This estimate has recently increased by +1.2% in the past month.

For the next fiscal year, analysts expect earnings of $10.95 per share, up +22.8% from last year’s forecast. This estimate has also increased by +1.1% recently.

To provide a more accurate outlook, our Zacks Rank rating system incorporates earnings estimate changes alongside other key factors. Currently, Alibaba holds a Zacks Rank of #1 (Strong Buy), signaling positive near-term price potential based on these revisions.

The following chart illustrates the trend of Alibaba’s 12-month consensus EPS estimates:

12-Month EPS Trend

Revenue Growth Potential

Earnings growth is a critical indicator of financial health. Companies typically cannot sustain earnings growth without a corresponding increase in revenue. Thus, evaluating revenue growth potential is essential.

For Alibaba, the consensus sales estimate for the current quarter is $33.08 billion, representing a year-over-year growth of +7.6%. Sales estimates for this fiscal year and the next are projected at $137.03 billion and $143.44 billion, reflecting anticipated increases of +5% and +4.7%, respectively.

Recent Performance and Earnings Surprise History

In its most recent quarter, Alibaba reported revenues of $38.38 billion, a +4.7% year-over-year increase. Earnings per share (EPS) stood at $2.93, compared to $2.67 in the prior year.

Alibaba’s reported revenues exceeded the Zacks Consensus Estimate of $38.19 billion, yielding a surprise of +0.51%. However, its EPS fell short of the consensus by -4.87%.

Over the last four quarters, Alibaba outperformed consensus EPS estimates twice and exceeded revenue forecasts three times.

Valuation Analysis

A stock’s valuation is critical when making investment decisions. It is vital to determine whether the current price is in line with the intrinsic value of the underlying business and its growth prospects.

Analyzing a company’s valuation multiples—like price-to-earnings (P/E), price-to-sales (P/S), and price-to-cash flow (P/CF)—against historical and peer benchmarks can indicate whether a stock is undervalued, fairly valued, or overvalued.

Alibaba has received a B grade from the Zacks Value Style Score, suggesting it is currently trading at a discount to its peers.

Conclusion

The insights presented here may help you assess whether Alibaba is worth monitoring in light of market developments. Its Zacks Rank of #1 suggests a likelihood of outperformance compared to the broader market in the near term.

For more detailed stock analysis, including Alibaba’s performance metrics, please refer to our previous reports.

The views expressed herein are those of the author and do not necessarily reflect those of Nasdaq, Inc.