Amidst the cacophony of stock market chatter, two companies not only stand out but thrive. Eli Lilly & Company (LLY) and Novo Nordisk A/S (NVO) hog the limelight, thanks to their GLP-1 weight loss drugs. While Eli Lilly and Novo Nordisk shine, today’s enlightening discussion will revolve around the formidable Novo Nordisk, which declared financial results on Jan. 31.

The Growth Surge

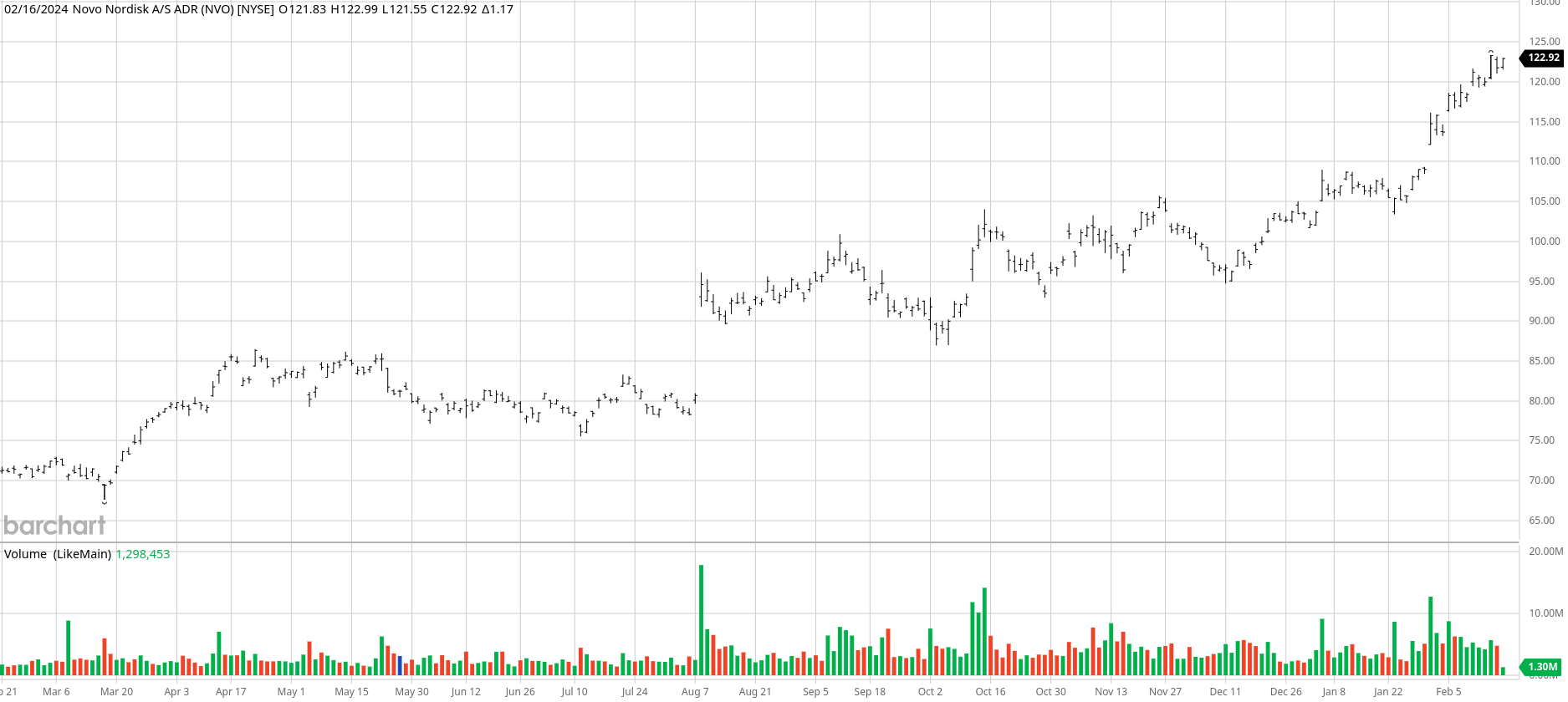

NVO shares have soared to unprecedented heights, owing to the Danish pharmaceutical company’s stellar weight-loss drugs that witnessed a monumental surge in sales and profits throughout 2023. Novo Nordisk proudly announced a 36% surge in sales, amounting to $33.7 billion, accompanied by profits soaring to $12.14 billion or $2.70 per share.

The fourth quarter alone witnessed an 85% growth in the sales of diabetes drug Ozempic and a staggering 311% surge in sales of the obesity drug Wegovy.

Lars Fruergaard Jørgensen, CEO of Novo Nordisk, amplified this triumph during the Q4 conference call, expressing delight at the robust 2023 performance and highlighting that over 40 million people now benefit from their revolutionary diabetes and obesity treatments.

A Bright Future Beckons

Management’s projection of revenue growth up to 26% and operating profit by up to 29% at constant exchange rates might seem modest. However, I firmly believe in the potential for far greater expansion.

Is there expansive growth lying in wait for GLP-1 treatments beyond diabetes and obesity? These drugs might herald a new era in the fight against a spectrum of diseases including cardiovascular ailments, fatty liver disease, chronic kidney disease, sleep apnea, and even Alzheimer’s.

The trial results published in November, revealing that Wegovy slashes the risk of death by 18% for patients with cardiovascular disease (with the risk of heart attack reduced by 28%), are poised to catalyze health systems and insurers to renderfinancial support for the treatment.

The broadening scope of GLP-1 medicines is witnessed in the potential to alleviate depression. Preliminary data from the health records of 4 million people consuming GLP-1s, such as Novo Nordisk’s Wegovy and Eli Lilly’s Zepbound, hint at an improved mental well-being. Despite the necessity for clinical studies to confirm and comprehend this effect, the potential of these drugs to address not only physical but also mental health is likely to mount pressure on insurers to cover their costs.

Defeating the Bears

Numerous naysayers criticize Novo Nordisk, pointing to its challenges in meeting the demand for both Wegovy and Ozempic, which share the same active ingredient, semaglutide. Shrugging off these detractors’ claims, the company displayed its determination through announcing $8.7 billion in investments last year to bolster manufacturing capacity. Accelerating this, on Feb. 5, the acquisition of three manufacturing sites for $11 billion was struck.

Is rampant competition encroaching on the weight loss sector, spelling trouble for Novo Nordisk? Here’s where we separate the wheat from the chaff. Novo Nordisk possesses an underappreciated advantage – a weight-loss pill that dodges the drawbacks of an injection. Test results released last year projected a 17% body weight reduction over 68 weeks for individuals utilizing the pill alongside diet and exercise counseling. It is estimated that this pill could generate billions in revenue in what Bloomberg Intelligence analysts predict to be an $80 billion market by 2030.

An Undeniable Asset

Beyond being a trailblazer in diabetes care, incorporating a heritage of over 85 years, Novo Nordisk steadfastly retains its prominent position in the $66 billion diabetes treatment market. With a 33.8% share at the end of 2023, signifying a 190 basis point increase compared to 2022, Novo has established its dominance, commanding a 54.8% share of the GLP-1 sector and a 43.9% share of the insulin segment.

Surpassing the half-billion market cap, Novo Nordisk has elegantly dethroned luxury conglomerate LVMH (LVMUY) to emerge as Europe’s most valuable company.

Regarding investment, NVO stock is a hard-hitting recommendation at any price under $135 per share.

On the date of publication, Tony Daltorio did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.