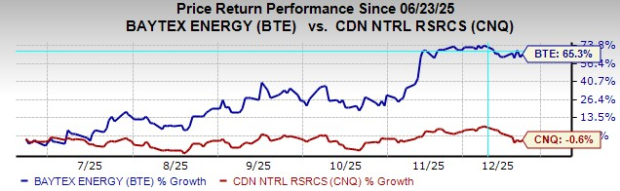

Baytex Energy (BTE) has significantly improved its financial position heading into 2026 by selling its Eagle Ford assets, resulting in a stronger balance sheet and reduced debt. This strategic move, alongside a focus on higher-return Canadian assets and a capital allocation strategy that prioritizes cash flow, positions Baytex for better free cash visibility. As a result, BTE shares have surged 65.3% over the past six months.

Conversely, Canadian Natural Resources (CNQ) is maintaining stability through a C$6.3 billion capital budget for 2026, focusing on low-cost production across oil sands, conventional crude, and natural gas. Although CNQ’s production is projected to grow by about 3%, its shares have declined by 0.6% in the same timeframe, reflecting slower-growth conditions in comparison to Baytex.

Investment outlooks reveal a significant earnings divergence, with Baytex expected to achieve 9.5% growth in EPS by 2025, while CNQ anticipates a slight decline of 0.8%. This data underscores Baytex’s advantage for investors seeking higher returns as market dynamics shift toward balance-sheet strength and capital discipline in the energy sector.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.