The Cooper Companies (COO) reported second-quarter revenues of $358 million for CooperSurgical, marking a 6% organic growth, with fertility revenues increasing by 10% to $143.8 million. However, the company faced challenges in the Asia-Pacific region, with sales dropping 6% to $130.6 million, attributed to weakened demand in Japan, China, and Korea.

Despite a net pre-tax charge of $271.6 million linked to litigation and a recall, COO raised its fiscal 2026 free cash flow outlook to approximately $650 million. As of April 2026, COO’s cash and cash equivalents stood at $138.8 million against $2.46 billion in total debt, highlighting the importance of cash generation and debt reduction for future growth.

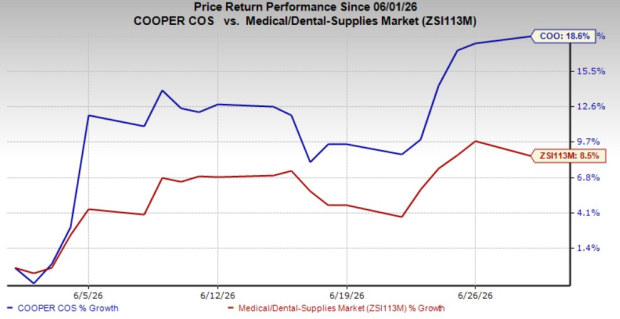

COO shares increased 18.6% over the past month, outperforming the industry average of 8.5%. Analysts currently assign a Zacks Rank #3 (Hold) to the stock, reflecting mixed sentiment amid ongoing operational challenges.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.