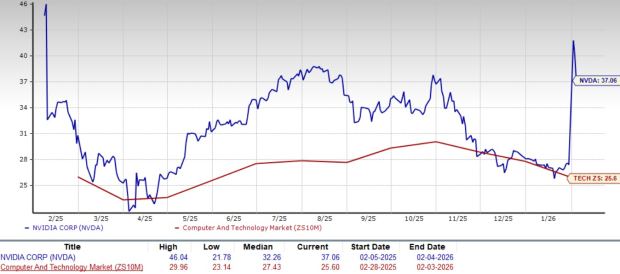

NVIDIA Corporation (NVDA) is currently valued at a forward 12-month price-to-earnings (P/E) ratio of 37.06, significantly higher than the Zacks Computer and Technology sector average of 25.60. Over the past year, NVIDIA’s shares have increased by 37.9%, outpacing the sector’s overall growth of 23%. In comparison, key competitors like Advanced Micro Devices and Broadcom have surged 85.3% and 40.5% respectively, while Marvell Technology has seen a decline of 37.1% within the same timeframe.

In the third quarter of fiscal 2026, NVIDIA reported a 62% year-over-year revenue increase, amounting to $65 billion, with a gross margin projected at 75%. The company’s Data Center business, accounting for 89.8% of total revenues, generated $51.22 billion—up 66% year-over-year—driven by increased demand for AI-related technology. NVIDIA generated a free cash flow of $23.75 billion in the same quarter and returned $243 million to shareholders.

The strong demand for NVIDIA’s GPU solutions, particularly in AI and high-performance computing, positions the company favorably for future growth. Analysts maintain a positive outlook, with expectations for continued revenue and earnings growth, making NVDA a recommended buy.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.