Philip Morris International Shows Strong Performance Amid Market Trends

Philip Morris International Inc. (PM), boasting a market capitalization of $238.7 billion, is a major player in the tobacco industry. The company is actively pursuing a smoke-free future while diversifying its portfolio beyond traditional tobacco and nicotine products. Based in Stamford, Connecticut, PM offers a range of alternatives such as heat-not-burn devices and oral nicotine products, marketed under brands like IQOS and ZYN.

As a “mega-cap” stock, PM exemplifies companies valued over $200 billion. It benefits from a robust brand portfolio, extensive global market coverage, and a leading position in smoke-free alternatives. Key drivers of PM’s market strength include its pricing power, substantial research and development investments, and adaptability to regulatory changes. Overall, with a solid financial performance and a commitment to reduced-risk products, PM is positioned for sustainable long-term growth.

Active Investor: FREE newsletter uncovering the hottest stocks and new trade opportunities.

Recent Stock Performance

Recently, the tobacco giant has experienced a 5.4% decrease from its 52-week high of $159.51, reached on March 3. Despite this decline, shares of PM have risen 15.6% over the past three months, outperforming the broader Dow Jones Industrial Average’s ($DOWI) 4.1% drop during the same period.

Performance Over Time

In the last six months, PM shares have jumped 20%, overshadowing the DOWI’s 6.1% increase. Over the past year, PM has surged 65%, far exceeding the DOWI’s 10.3% growth in the same timeframe.

PM has maintained trading levels above its 200-day moving average since late April and its 50-day moving average since mid-January, signaling a bullish market trend.

Q4 Earnings Highlights

On February 6, Philip Morris announced its Q4 earnings, resulting in an 11% jump in share prices. The company reported net revenues of $9.7 billion for the quarter, reflecting a year-over-year increase of 7.3%. Notably, revenue from smoke-free products rose by 9.2%, now accounting for 40% of total revenues.

Competitive Standing and Analyst Outlook

In comparison, PM has outperformed its main competitor, Altria Group, Inc. (MO), which saw a 39.1% rise over the past year and a 7.6% increase in the past six months.

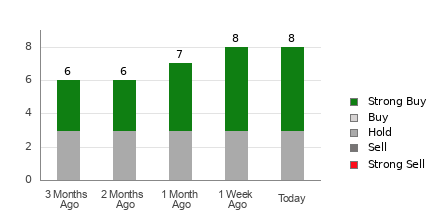

Despite these positive trends, analysts express cautious optimism regarding PM’s future. The stock holds a consensus rating of “Moderate Buy” from 12 analysts, currently trading above its mean price target of $150.60.

On the date of publication, Kritika Sarmah did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article are solely for informational purposes. For more information, please view the Barchart Disclosure Policy here.

The views and opinions expressed herein are those of the author and do not necessarily reflect those of Nasdaq, Inc.