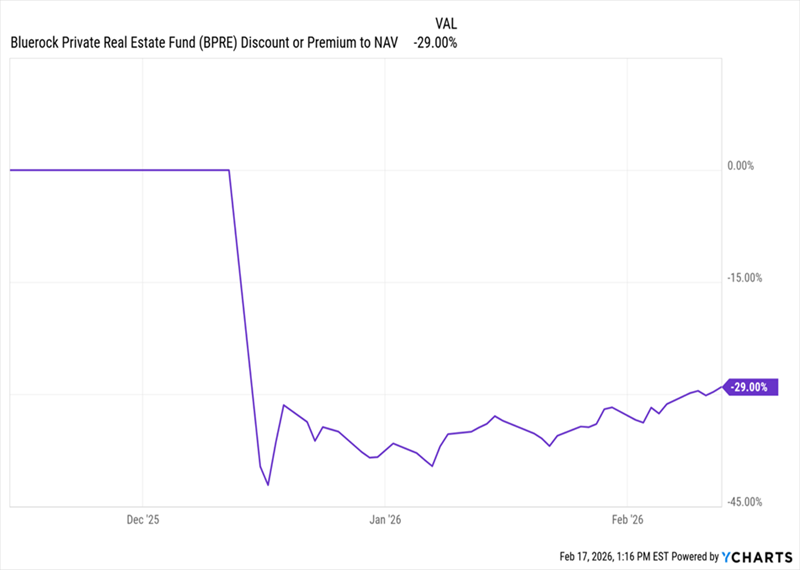

Investors in closed-end funds (CEFs) may be making costly mistakes by chasing large discounts to net asset value (NAV). Currently, the Bluerock Private Real Estate Fund (BPRE) is trading at a significant 29% discount, largely due to investor concerns about the illiquidity of its private real estate assets after its transition from a privately held to a publicly traded fund. In contrast, the Reaves Utility Income Fund (UTG) has a much smaller 1.1% discount, reflecting its established status and consistent income generation.

BPRE’s prolonged discount does not indicate a compelling buying opportunity, especially as nearly 10% of its assets are held in a money-market fund, raising questions about its liquidity management and long-term dividend sustainability. Meanwhile, UTG has shown strong performance with an annualized return of approximately 11% over the last decade and provides a current yield of 5.9%, making it a more favorable option for income-focused investors.

Understanding the reasons behind a fund’s discount is crucial. High dividends can attract attention, but without solid underlying performance or asset management, such discounts may not narrow as expected, potentially impacting investors negatively.