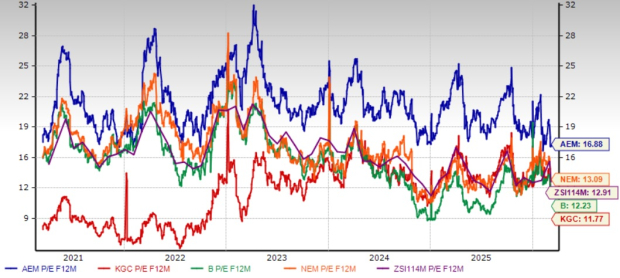

Agnico Eagle Mines Limited (AEM) is currently trading at a forward price-to-earnings ratio of 16.88X, representing a 30.8% premium over the Zacks Mining – Gold industry average of 12.91X. AEM’s shares have surged by 123.5% over the past year, though this growth trails the industry’s 132.9% increase and the S&P 500’s 24% rise. Key competitors such as Barrick Mining Corporation, Newmont Corporation, and Kinross Gold Corporation have reported even greater gains, with increases of 148.3%, 169.4%, and 191.1%, respectively, over the same period.

Agnico Eagle reported an operating cash flow of approximately $2.1 billion for Q4 2025, up 87% from the previous year, contributing to a record $6.8 billion in full-year cash flow. The company ended 2025 with a strong net cash position of nearly $2.7 billion, facilitating significant shareholder returns—around $1.4 billion through dividends and share buybacks—while reducing total long-term debt by approximately $950 million. AEM’s projected earnings for 2026 are estimated at $13.28, reflecting a year-over-year growth of 60.4%.

With a robust pipeline of growth projects and favorable market conditions, AEM is poised for continued advances in profitability and cash flow generation, supported by high gold prices driven by geopolitical tensions and macroeconomic uncertainties. The company’s dividend yield stands at 0.8% with a healthy payout ratio of 19%.