“`html

JPMorgan Chase & Co. reported a 9% year-over-year increase in total revenues for Q3 2025, driven by strong performances in markets, banking, asset management, and payments. The firm’s net interest income continued to benefit from higher card revolver balances and improved deposit margins, while investment banking fees rose due to increased M&A activity. Despite facing pressures from Federal Reserve rate cuts, JPMorgan remains well-positioned for continued growth, despite expectations of a challenging environment ahead.

In comparison, Bank of America and Citigroup both recorded 7% revenue growth over the first nine months of 2025, reaching $81.9 billion and $65.4 billion respectively. Both firms benefitted from strong net interest income and a rebound in investment banking fees, indicating a generally favorable macroeconomic environment.

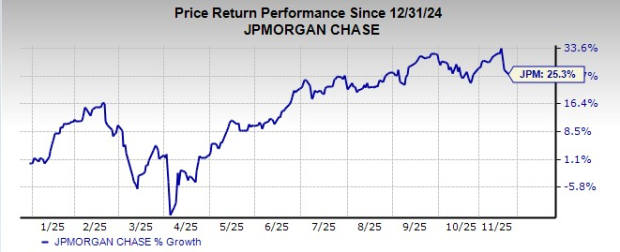

JPMorgan’s shares have risen 25.3% this year. The company’s 2025 earnings are projected to grow by 2.5% year-over-year, with estimates for 2026 showing a 3.6% increase, demonstrating a positive long-term growth outlook.

“`