Rocky days for the dominant stocks in the S&P 500.

While the S&P 500 surged to hit an all-time high last week, the leadership within this index has dwindled. The once formidable “Magnificent Seven” – Tesla (TSLA), Apple (AAPL), Amazon (AMZN), Alphabet (GOOGL) (GOOG), Microsoft (MSFT), Nvidia (NVDA), and Meta (META) – has been replaced by the “Troubling Three” – Microsoft, Meta, and Nvidia.

An Index of 3

The “Troubling Three” have given the impression of a robust equity market, propelling the S&P 500 to new heights. But a closer look reveals that nearly all the gains in the index this year can be attributed to them.

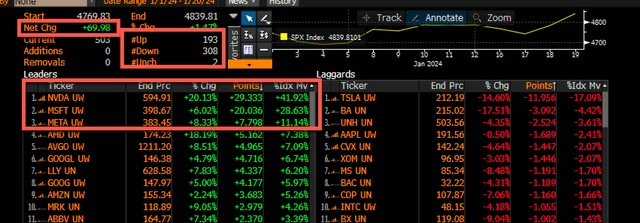

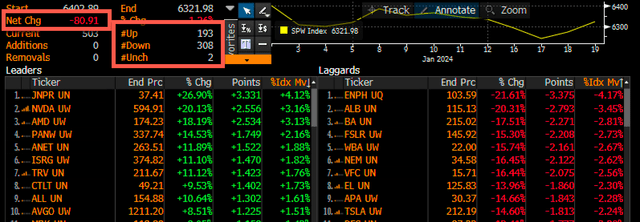

The S&P 500 has risen by 69.98 points this year (1.47%), with most gains traceable to just three stocks: Nvidia (29.3 points), Microsoft (20.0 points), and Meta (7.8 points). This means that 80% of the gains in the S&P 500 are from these three stocks, reflecting a significant concentration of influence.

Meanwhile, two of the former Magnificent Seven stocks have detracted from the S&P 500, with Tesla dragging it down by 11.95 points and Apple by 1.7 points in 2024. Of the 500 stocks in the S&P 500, only 193 are up for the year, with 308 down and two unchanged. Consequently, the S&P 500 Equal Weight Index is down 1.26% year to date.

The Trouble Unveiled

The disquieting aspect of these three front-running stocks is the contraction in the number of stocks driving the market’s rise. Moreover, these same three stocks had shown a buildup in call delta over the past few months, and these call options expired on Friday, January 19.

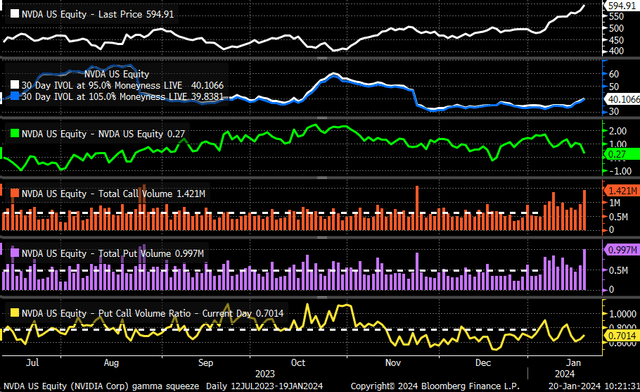

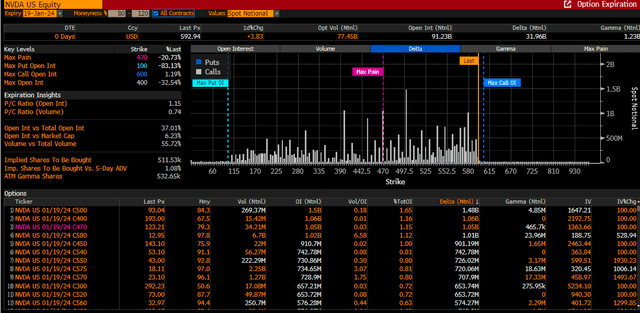

Nvidia is exhibiting signs of a gamma squeeze, with soaring call volumes, low put-to-call ratios, increasing implied volatility skewed towards calls, and a surging stock price. A gamma squeeze is a self-reinforcing phenomenon where investors purchase out-of-the-money call options, leading market makers to hedge the underlying asset by buying shares and driving the stock higher. This upward spiral intensifies as more calls are bought.

While this may seem bullish, it also suggests excess, as excessively high call implied volatility often triggers the end of a gamma squeeze, leading to a significant stock decline.

Of concern is that Nvidia, in the midst of a gamma squeeze, also had an extensive amount of call delta expiring on Friday. These call delta positions tend to reinforce themselves, pushing the stock value higher and fueling the gamma squeeze further.

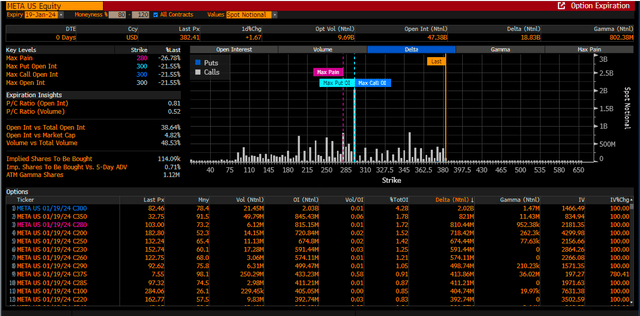

A similar pattern is discernible in Meta, with substantial amounts of in-the-money call options expiring last Friday, reinforcing the delta dynamic and flows that have shored up the stocks and sustained their climb.

This predicament exposes the S&P 500 as predominantly influenced by just three stocks, primarily driven higher by options activity and hedging flows. Consequently, it no longer provides an accurate representation of the entire equity market and is vulnerable to a sharp decline if these flows dissipate post option expiration next week.

Rising Implied Volatility

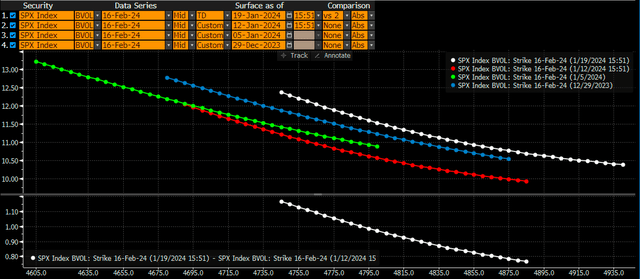

Furthermore, fixed strike implied volatility for the S&P 500 is surging for the February 16 option expiration. Despite the apparent decline in the VIX, the uptick in implied volatility for lower strike prices for the February options expiration indicates a demand to purchase downside protection at the S&P 500 index level.

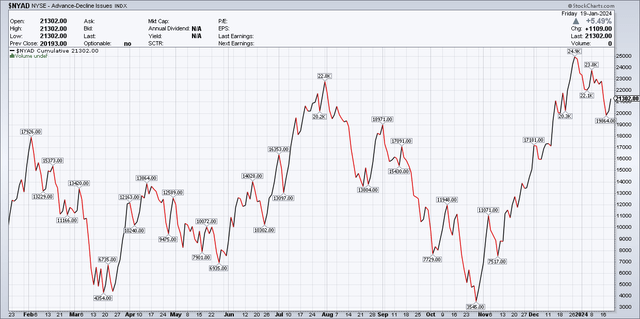

Despite rosy headlines, the bona fide market structure and flows disclose that the market is being propelled by fewer stocks, which is why the advance-decline on the NYSE is currently below its July peak.

Could the S&P 500 continue its ascent? It is no longer a representation of 500 stocks, posing a risk for S&P 500 index fund investors. However, if the hedging flows from last week’s options expiration end and Nvidia’s gamma squeeze subsides, the window for a significant pullback widens exceedingly.

Editor’s Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.