From the era of the Magnificent 7, the market has transitioned into a troubling phase with the Troubling Three taking the lead.

While the S&P 500 rose this past week to a new all-time high, what became clear was that the leadership in this index has contracted further. Gone are the magnificent seven of Tesla (TSLA), Apple (AAPL), Amazon (AMZN), Alphabet (GOOGL), Microsoft (MSFT), Nvidia (NVDA), and Meta (META). Enter the Troubling 3, made up of Microsoft, Meta, and Nvidia.

Analysis of the Troubling Three

The Troubling Three have given the illusion of a strong equity market, helping to lift the S&P 500 to a fresh all-time high. But digging deeper reveals that the Troubling Three accounts for nearly all of the gains seen in the index this year.

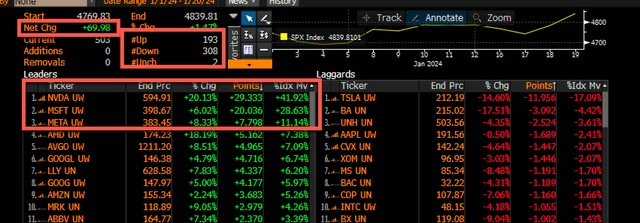

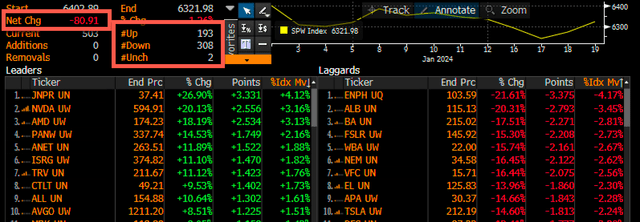

The S&P 500 is up 69.98 points this year, or 1.47%. Most of those gains can be attributed to three stocks: Nvidia, Microsoft, and Meta. Nvidia has accounted for 29.3 points, Microsoft has accounted for 20.0 points, and Meta has accounted for 7.8 points. That means that 57.1 points, or 80%, of the roughly 70 points gained in the S&P 500 are from just three stocks.

Meanwhile, 2 of the former Magnificent 7 stocks, Tesla has taken 11.95 points away from the S&P 500, and Apple has subtracted 1.7 points from the S&P 500 in 2024. Only 193 stocks in the S&P 500 are up for the year, 308 are down for the year, while two are unchanged. That is why the S&P 500 Equal Weight Index is down 1.26% year to date.

The Trouble with the Troubling 3

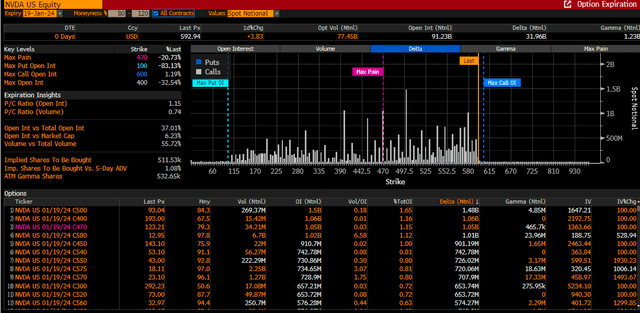

What is troubling about the three stocks leading the market higher is that the number of stocks driving the market is contracting. Second, these are the same three stocks noted earlier last week that had seen tremendous amounts of call delta built up over the past several months, and call options expired on Friday, January 19.

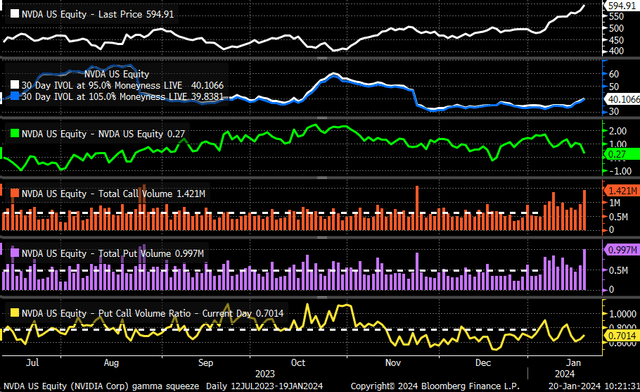

Nvidia also exhibits signs of a gamma squeeze, with higher call volume, the put-to-call ratio at the low end of the historical range, implied volatility rising and skewed to the calls side, and the stock price rocketing higher. A gamma squeeze is a self-reinforcing action where investors buy out-of-the-money call options, which results in market makers hedging the underlying by buying the shares, pushing the stock higher.

While this can be seen as a sign of bullishness, it can also be seen as a sign of excess because typically, once the call implied volatility gets too high, the process of the gamma squeeze burns out, and that results in the stock dropping significantly.

The problem here is that not only is Nvidia amid a gamma squeeze, but it also had a tremendous amount of call delta that expired on Friday. These call delta positions, for the most part, become self-reinforcing because as the stock price goes higher, more hedging needs to take place against these open call positions, which in itself pushes the value of the stock price higher, which in part helps to fuel the gamma squeeze even more.

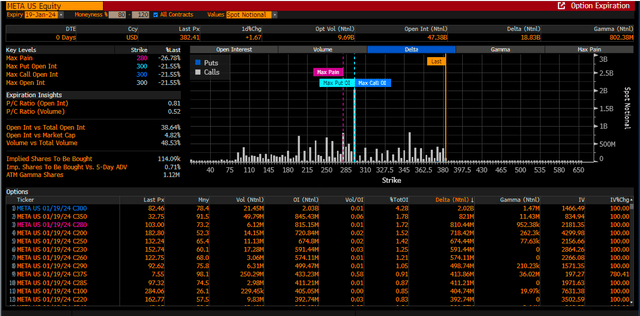

This same dynamic is also visible in Meta, with large amounts of in-the-money call options that expired on Friday, with the same reinforcing delta dynamic and flows that have helped to support the stocks and, more importantly, keep the stock grinding higher.

So the problem here is that if the S&P 500 has now become an overall representation of just three stocks and these stocks have been driven higher primarily by options activity and hedging flows, then it is no longer an accurate representation of the entire equity market and also becomes at risk of changes in these options flows, and more importantly vulnerable to a sharp decline if these flows disappear post option expiration starting next week.

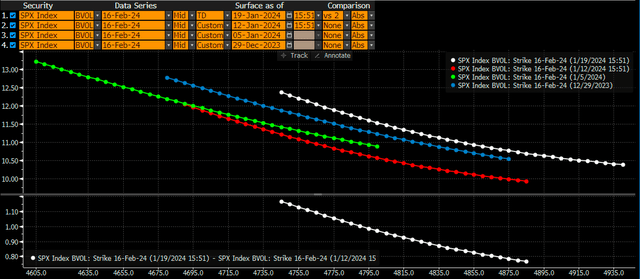

Rising Implied Volatility

Additionally, what is also clear is that fixed strike implied volatility for the S&P 500 is on the rise for the February 16 option expiration. So, while there is this appearance that implied volatility is falling, as noted by the decline in the VIX, implied volatility for lower strike prices for the February options expiration. This is a sign that on the S&P 500 index level, there is a demand to buy and own downside protection.

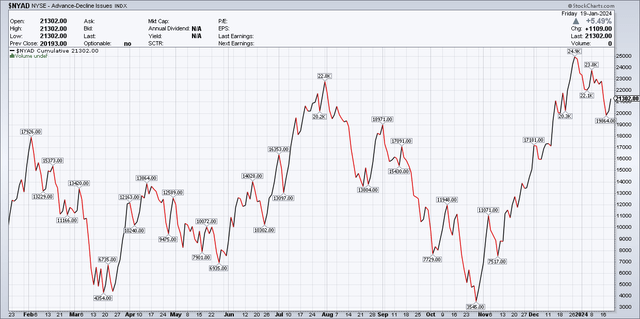

While it may seem on the headlines that all is well in the equity market and the stocks can only go higher from here, a breakdown of the actual structure and flows shows that the market is being driven higher by fewer stocks and the reason why the advance-decline on the NYSE is now below its July peak.

Could the S&P 500 continue to move higher? The S&P 500 itself is no longer a representation of 500 stocks at this point. So yes, that is a risk for S&P 500 index fund investors, but if the hedging flows from this week’s options expiration are now behind us and Nvidia’s gamma squeeze ends, then the window for a significant pullback is about as wide open as it is going to get.

Editor’s Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.