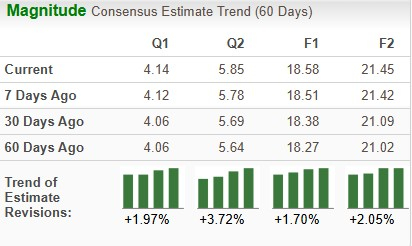

FedEx Corporation FDX is set to release its third-quarter fiscal 2026 (ended Feb. 28, 2026) results on March 19, after market close. The Zacks Consensus Estimate for the to-be-reported quarter’s earnings per share and revenues is pegged at $4.14 and $23.59 billion, respectively.

The consensus estimate for third-quarter fiscal 2026 earnings has been revised upward by 1.97% in the past 60 days. The mark has declined 8.2% from the year-ago actual. The Zacks Consensus Estimate for third-quarter fiscal 2026 revenues indicates a 6.5% upward movement from the year-ago actual.

Image Source: Zacks Investment Research

FDX has an impressive earnings surprise history, as reflected in the chart below.

Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

Given this backdrop, let’s examine the factors that might have influenced FDX’s fiscal third-quarter results.

We expect FDX’s bottom-line performance in the to-be-reported quarter to have been aided by cost-reduction benefits from the DRIVE program initiatives. These cost-reduction initiatives include reducing flight frequencies, parking aircraft and cutting staff. Cost-reduction efforts, particularly in line-haul expenses and productivity, are expected to have supported margins in the fiscal third quarter. Leveraging artificial intelligence to optimize routing, improve capacity planning and enhance digital capabilities are also likely to have aided bottom-line performance by lowering costs.

Focus on growing premium B2B and B2C volume, particularly in the healthcare sector, should have resulted in higher yields. Moreover, the rate increase, announced in January, on FedEx parcel and Freight LTL services is likely to have supported revenues.

We expect an update from management on FDX’s multi-year deal with Amazon AMZN, which was signed last year. Per the agreement, FDX is responsible for delivering select large packages for Amazon. The deal comes soon after FDX’s rival, United Parcel Service UPS, decided to lower its volumes with Amazon.

Q3 earnings Whispers for FDX

Our proven model predicts an earnings beat for FDX this time. A company with a Zacks Rank #1 (Strong Buy), 2 (Buy) or 3 (Hold), along with a positive earnings ESP, has a higher chance of beating estimates, which is exactly the case here.

earnings ESP: FedEx has an earnings ESP of +2.30% (the most accurate estimate of $4.23 is pegged at 9 cents above the Zacks Consensus Estimate). You can uncover the best stocks to buy or sell before they are reported with our earnings ESP Filter.

Zacks Rank: The company currently carries a Zacks Rank #3. You can see the complete list of today’s Zacks #1 Rank stocks here.

FDX Stock Outperforms Industry & UPS in Q3

Driven by the cost-reduction efforts, shares of FDX have increased in double-digits in the third quarter of fiscal 2026 (December-February), outperforming the Zacks Transportation-Air Freight and Cargo industry and rival United Parcel Service.

Q3 Price Comparison

Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

FDX trading Cheap

Based on forward 12-month Price/Sales (P/S), FDX’s shares are trading at a discount compared with the industry average as well as United Parcel Service. FDX currently has a Value Score of B.

FDX’s P/S F12M Vs. Industry & UPS

Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

Investment Thesis for FDX Stock

Tariff-related uncertainty and still-high inflation have been hurting consumer sentiment and growth expectations. FDX continues to struggle due to the normalization of volume and pricing trends in the post-COVID scenario.

The company’s efforts to reward its shareholders are likely to have supported the share price. In June 2025, FedEx raised its quarterly dividend by 5.1% to $1.45 per share (or $5.80 annually). FDX is also active on the buyback front.

End Note

It is worth noting that the company has the brand and the network to continue generating steady cash flows in the long run. This makes FDX a compelling long-term player in the transportation space. However, the near-term headwinds, including the tariff-induced uncertainties, are hard to ignore.

So, all in all, it is worth holding on to FDX Stock for now. Betting on the Stock ahead of its upcoming results does not seem like a good idea. It is better to wait for management’s commentary on volumes and cost-cutting efforts, apart from the fiscal 2026 guidance, to get more clarity on near-term prospects.

Zacks’ Research Chief Picks Stock Most Likely to “At Least Double”

Our experts have revealed their Top 5 recommendations with money-doubling potential – and Director of Research Sheraz Mian believes one is superior to the others. Of course, all our picks aren’t winners but this one could far surpass earlier recommendations like Hims & Hers Health, which shot up +209%.

see Our Top Stock to Double (Plus 4 Runners Up) >>

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Amazon.com, Inc. (AMZN) : Free Stock Analysis report

United Parcel Service, Inc. (UPS) : Free Stock Analysis report

FedEx Corporation (FDX) : Free Stock Analysis report

This article originally published on Zacks Investment Research (zacks.com).

Zacks Investment Research

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.