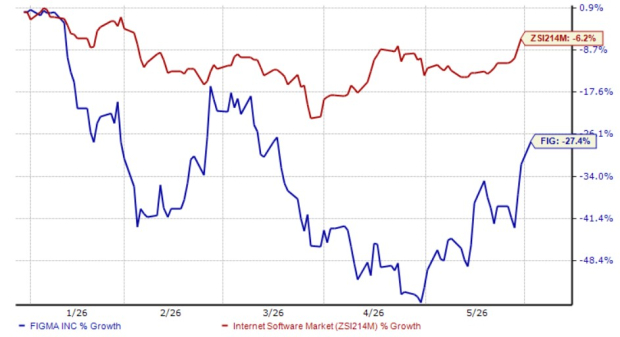

Figma (FIG) shares have declined by 27.4% year-to-date (YTD) as of now, while the Zacks Internet – Software industry has seen a decline of only 6.2%. Despite this underperformance, Figma’s stock is trading at a premium, with a forward 12-month Price/Sales ratio of 7.8X, significantly higher than the industry average of 4.06X.

Figma operates in a competitive design and product workflow market, facing challenges from major players like Adobe, Microsoft, and Atlassian. The company’s strong net dollar retention rate of 139% is primarily driven by seat expansion among large enterprises. However, slowing hiring activity and tighter enterprise technology budgets could pose risks, as growth is heavily reliant on customer adoption and software spending.

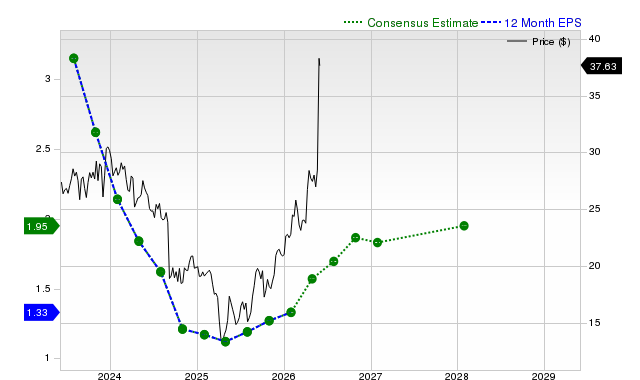

Figma’s non-GAAP gross margin for Q1 2026 was reported at 82%, a decline from previous highs. Earnings projections for 2026 stand at 23 cents per share, a 23% decrease year-over-year, with estimates remaining steady for the last 60 days. In the context of intense competition and rising operational costs, analysts advise caution regarding investment in Figma, labeling it a Zacks Rank #4 (Sell) stock.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.